Superannuation Death Benefits

Summary

Superannuation death benefits are payments your fund makes from your super when you die. They can go to eligible dependants or your estate, as lump sums or income streams. Tax depends on whether the recipient is a tax dependant, their age, and the tax-free and taxable components of your balance at death.

Table of Contents

- Introduction

- What Is a Superannuation Death Benefit?

- Who Can Receive a Superannuation Death Benefit?

- How and When Superannuation Death Benefits Must Be Paid

- Reversionary Pensions and Their Role in Superannuation Death Benefits

- Tax Components of Super and Why They Matter on Death

- Tax on Lump Sum Death Benefits

- Tax on Death Benefit Income Streams

- Common Practical Scenarios

- Super Nominations

- Strategies to Manage Super Death Benefit Tax

- How This Links to Inheritance and Estate Planning

- Working with a Planner in the Sutherland Shire and Sydney CBD

- FAQs

- Superannuation & SMSFs Knowledge Bundle

- Inheritance & Estate Planning Knowledge Bundle

Introduction

For many households in the Sutherland Shire and Sydney CBD, superannuation and, in some cases, SMSFs will be one of the largest assets eventually passing to beneficiaries. However, super does not automatically follow your will. It sits in a separate structure, with its own rules about who can receive it and how it is taxed.

This article explains, for the 2025–26 environment:

What a superannuation death benefit is

Who can receive it under super and tax law

How lump sums and pensions are taxed for different recipients

How nominations, reversionary pensions, and SMSFs interact with estate planning

It connects directly with:

James Hayes is an ASIC-licensed financial planner based in Caringbah, working with clients across the Sutherland Shire and Greater Sydney on super, SMSFs, and estate-linked retirement planning. He does not assist with Centrelink Jobseeker support, debt consolidation using super, or early-release schemes.

What Is a Superannuation Death Benefit?

When a member of a super fund dies, their fund must pay out their remaining superannuation as a superannuation death benefit.

Key features are consistent across large funds and SMSFs:

The benefit must be “cashed as soon as practicable” after death, generally within about 6–12 months, depending on the circumstances and any disputes.

It must be paid either to eligible dependants and/or to the legal personal representative (LPR), usually the executor of the estate.

It can be paid as a lump sum, an income stream, or a combination, subject to who the beneficiary is and the fund’s rules.

How this happens in practice depends on the fund deed, any valid nominations, any reversionary pensions, and interaction with your will.

Need help understanding who qualifies as a dependant under both sets of rules? Download the Super Beneficiary & Estate Checklist — it lays everything out in a simple way.

Who Can Receive a Superannuation Death Benefit?

There are two overlapping sets of rules:

Superannuation law (SIS regulations): Who the fund is allowed to pay

Tax law (ITAA 1997): Who counts as a “death benefits dependant” for tax purposes.

The definitions are similar but not identical.

Dependants Under Superannuation Law

Under superannuation law, a death benefit dependant includes:

A spouse or de facto spouse

A child of any age

A person in an interdependency relationship – a close personal relationship where two people live together and provide financial, domestic, and personal support

Funds can also pay to the legal personal representative (LPR), meaning the estate.

Recent commentary has highlighted that these definitions can leave some single people with limited direct beneficiary options, especially where they want to benefit siblings or friends who do not meet dependency tests. This creates a link between super nominations and broader estate planning.

Death Benefits Dependants Under Tax Law

Under taxation law, a death benefits dependant is defined in section 302-195 ITAA 1997 and includes:

Spouse or de facto spouse

Former spouse

A child under 18

A person who was financially dependent on the deceased

A person in an interdependency relationship with the deceased

In addition, certain beneficiaries of defence and police personnel who die in the line of duty are treated as death benefits dependants.

This definition determines whether a death benefit is taxed, and at what rate.

Why the Distinction Matters

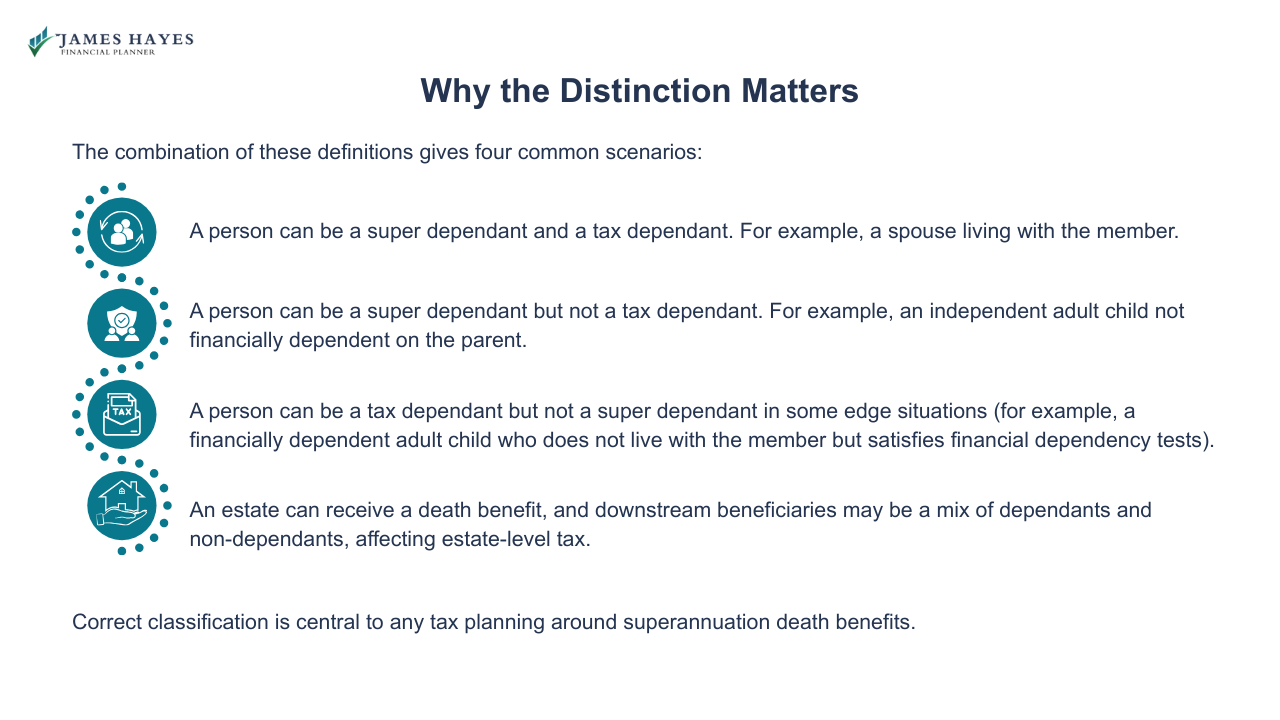

The combination of these definitions gives four common scenarios:

A person can be a super dependant and a tax dependant. For example, a spouse living with the member.

A person can be a super dependant but not a tax dependant. For example, an independent adult child not financially dependent on the parent.

A person can be a tax dependant but not a super dependant in some edge situations (for example, a financially dependent adult child who does not live with the member but satisfies financial dependency tests).

An estate can receive a death benefit, and downstream beneficiaries may be a mix of dependants and non-dependants, affecting estate-level tax.

Correct classification is central to any tax planning around superannuation death benefits.

If you want help mapping who qualifies as a dependant under both sets of rules, download the Super Beneficiary & Estate Checklist. This guide makes it easy.

How and When Superannuation Death Benefits Must Be Paid

Superannuation law requires that a member’s benefit be “cashed” as soon as practicable after death.

In practice, trustees must:

Identify potential beneficiaries (including the LPR).

Review any binding or non-binding nominations and the deed.

Determine who is entitled, then pay as lump sums and/or pensions consistent with the law and the fund rules.

The ATO previously suggested six months as a guide, but that explicit timeframe has been removed. For well-managed funds, 6–12 months is a common range, allowing for documentation, tax calculations, and disputes where they arise.

Lump Sums Versus Income Streams

Death benefits can be paid either as lump sums or as death benefit income streams, subject to eligibility.

High-level rules are:

Any beneficiary can generally receive a lump sum, either directly or through the estate.

Only a death benefits dependant (tax definition) can receive, or continue to receive, a death benefit income stream. Non-dependants cannot start a new death benefit pension.

Children can receive an income stream only if they are under 18, or under 25 and financially dependent, or have a permanent disability. Otherwise, any child pension must convert to a tax-free lump sum by age 25.

In addition, there is a lifetime transfer balance cap (TBC) – $2.0 million from 1 July 2025 – which limits how much can sit in tax-free retirement-phase pensions, including death benefit income streams.

The TBC interaction is explained in more detail in Accessing Your Super (Before & After Retirement).

If you want to be clear on who your fund is likely to pay — and why — the Super Beneficiary & Estate Checklist helps you document your funds, nominations, and intended beneficiaries before you speak with an adviser.

Reversionary Pensions and Their Role in Superannuation Death Benefits

If you already receive an account-based pension, you may be able to nominate a reversionary beneficiary so the income stream continues automatically to them on your death.

Key features of reversionary pensions include:

The pension does not stop on death. It “reverts” to the nominated beneficiary if they are eligible.

The proportioning of tax-free and taxable components remains the same. It flows through to the beneficiary.

The value of the pension counts toward the beneficiary’s transfer balance cap, with special timing rules for reporting.

A reversionary nomination can provide clarity and reduce delays for a spouse or eligible child.

Free eBook: Super Beneficiary and Estate Checklist (Instant Download)

〰️

Free eBook: Super Beneficiary and Estate Checklist (Instant Download) 〰️

Tax Components of Super and Why They Matter on Death

Every super account is divided into:

Tax-free component: Largely non-concessional contributions and some pre-July 2007 elements.

Taxable component, which can be further split into:

Taxed element: Contributions and earnings where the fund has paid tax.

Untaxed element: Usually from untaxed schemes (including some public sector funds), or certain insurance-related allocations.

The proportion of tax-free and taxable components is fixed for each interest and determines how much of any payment can be taxed.

On death, the recipient of the benefit (and whether they are a death benefits dependant) determines whether the taxable components are taxed and at what rate.

Tax on Lump Sum Death Benefits

Tax on lump sum death benefits is usually applied once, to the recipient, based on their status and the components.

Lump Sum to a Death Benefits Dependant

If a lump sum death benefit from either a taxed or untaxed fund is paid to a death benefits dependant (tax definition), the entire lump sum is tax-free, including both taxed and untaxed elements.

This typically applies to spouses, financial dependants, and qualifying children.

Lump Sum to a Non-dependant

If a lump sum is paid to a non-dependant (for tax purposes), such as an independent adult child:

The tax-free component is tax-free.

The taxable taxed element is taxed at a maximum rate of 15% plus Medicare (17% effective).

The taxable untaxed element is taxed at a maximum rate of 30% plus Medicare (32% effective), subject to the untaxed plan cap.

An adult child receiving a large benefit from an untaxed public sector scheme can therefore face significant tax on the untaxed element.

Lump Sum Paid to the Estate

If the death benefit is paid to the trustee of a deceased estate:

If all ultimate beneficiaries are death benefits dependants, the estate pays no tax on the lump sum.

If any ultimate beneficiaries are non-dependants, the estate pays tax on the taxable components at the same effective rates that would have applied had the amounts been paid directly to non-dependants.

Recent private rulings confirm that paying a benefit initially to a spouse’s estate will not preserve tax-free treatment if the end beneficiaries are non-dependants.

This is one reason superannuation death benefits are tightly integrated with estate planning in the Inheritance & Estate Planning Knowledge Pack.

Tax on Death Benefit Income Streams

A death benefit income stream can usually be paid only to a death benefits dependant.

The tax treatment depends on:

Whether the recipient is under 60 or age 60+

Whether the deceased was under 60 or 60+ when they died

Whether the fund is a taxed or untaxed scheme

For taxed funds:

If both deceased and beneficiary are under 60, the taxable component of pension payments is taxed at the beneficiary’s marginal rate, with no automatic offset.

If either the deceased or the beneficiary is 60 or over, the taxable component is generally tax-free in the beneficiary’s hands.

For untaxed funds, the taxable component of death benefit pensions may be assessable with a 10% tax offset, even for dependants, and may be subject to defined benefit income caps.

Death-benefit pensions also count towards the recipient’s transfer balance cap, which can require restructuring of their existing retirement-phase interests.

Common Practical Scenarios

Illustrative scenarios help show how these rules apply in practice. These are simplified and assume taxed funds.

Scenario 1: Spouse Receives a Lump Sum

Member dies at age 68, with a super balance of $800,000: 20% tax-free, 80% taxable (taxed element).

Spouse aged 66 receives a lump sum directly from the fund.

Because the spouse is a death benefits dependant, the entire $800,000 lump sum is tax-free, regardless of components.

Scenario 2: Adult Child Receives a Lump Sum

Same starting balance: $800,000, with 20% tax-free and 80% taxable (taxed element).

Independent adult child (age 40, not financially dependent) receives the lump sum directly.

Tax outcomes:

$160,000 tax-free component – tax-free

$640,000 taxable taxed element – taxed at 15% plus Medicare, with a tax offset ensuring the effective rate does not exceed this cap.

Scenario 3 – Spouse Pension Then Adult Children

Member dies with an account-based pension of $1.4m and an accumulation account of $300,000, all in a taxed fund.

Spouse (age 62) is nominated as a reversionary beneficiary, and later leaves remaining funds to independent adult children via the estate.

On death:

The pension reverts to the spouse and continues as a death benefit income stream. Payments to the spouse are generally tax-free.

When the spouse later dies, any residual balance becomes a death benefit to adult children, taxed per Scenario 2.

This illustrates how tax-free treatment on initial payment to a dependant does not eliminate tax for later non-dependant beneficiaries.

Super Nominations

Your super fund does not automatically follow your will. In most retail and industry funds, trustees consider:

The trust deed and rules

Any binding death benefit nomination (BDBN)

Any non-binding nomination

Any reversionary pension nomination

The pattern of contributions and other evidence of intent

Binding Death Benefit Nominations (BDBNs)

A valid BDBN:

Directs the trustee to pay benefits to the nominated person(s), if they are eligible dependants or the LPR.

Must meet formal requirements (correct form, signatures, witnesses, and sometimes time limits such as three-year lapsing rules).

Can reduce the risk of disputes and complaints.

Recent court and complaints-authority decisions show that, without a valid BDBN, trustees can exercise discretion in ways that may surprise adult children, especially in blended families.

Non-binding Nominations

A non-binding nomination expresses a preference but does not bind the trustee. It may be used where it is difficult to nominate a strict dependant (for example, for some single people), but it does not guarantee the outcome.

Non-binding nominations should be aligned with your will and broader estate plan, but additional documentation may be needed to reduce the risk of disputes.

SMSF–specific Issues

In SMSFs, the fund deed and trustee control are critical. Trustees must ensure:

BDBNs are drafted to comply with the deed and SIS law.

Reversionary pensions are documented in pension terms, not just in fund minutes.

Corporate trustee and shareholding structures support the intended succession control.

Those topics sit in Self-Managed Super Funds (SMSFs) Explained, Setting Up an SMSF, and SMSF Compliance & Administration.

If you’re unsure whether your nomination still does what you think it does, use the Super Beneficiary & Estate Checklist. It helps you review every fund, every nomination, and spot anything that needs updating.

Strategies to Manage Super Death Benefit Tax

Managing future death benefit tax is part of a broader retirement and estate plan. Common techniques include:

Re-contribution strategies: Withdrawing taxable super and recontributing as non-concessional contributions to increase the tax-free component.

Structuring pensions: Using account-based pensions and, where appropriate, reversionary nominations within transfer balance cap limits.

Insurance planning: Considering whether life insurance should be held inside or outside super.

Charitable or inter vivos gifts: Moving assets outside the super system during lifetime.

These strategies involve interaction with contribution caps, transfer balance caps, Age Pension tests, and capital gains tax on other assets. Theese concerns are addressed across Tax Benefits of Super Contributions, How to Grow Your Super Balance.

Working with a Planner in the Sutherland Shire and Sydney CBD

Questions that often arise for households in the Shire and Sydney CBD include:

How will my super be divided between my spouse, children, and other beneficiaries?

Will any beneficiaries pay tax of 15%, 30%, or more on my super?

Should I use binding nominations, reversionary pensions, my will, or a combination?

How do my SMSF deed, corporate trustee, and estate plan fit together?

James Hayes advises on super, SMSFs, and retirement strategies, and works alongside clients’ legal advisers on wills, enduring documents, and disputes.

He does not provide legal services, Jobseeker advice, or debt consolidation via super, but can coordinate with solicitors and tax agents to align superannuation death benefits with the wider inheritance plan. Book a free 15-minute call with him.

FAQs

-

No. Superannuation is held in a trust, and the trustee decides how to pay death benefits in line with the fund deed, super law, and any valid nominations. A binding nomination to eligible dependants or your legal personal representative can align super with your will, but they operate through separate legal mechanisms.

-

For tax on super death benefits, a death benefits dependant includes your spouse or de facto spouse, former spouse, children under 18, someone financially dependent on you, or someone in an interdependency relationship. Adult children who are independent usually are not tax dependants, so taxable components they receive can be taxed at capped rates.

-

If your spouse receives a superannuation death benefit as a lump sum from either a taxed or untaxed fund, the entire amount is tax-free for them. If they receive an income stream from a taxed fund and they or you were 60 or over at death, pension payments are generally tax-free, subject to defined-benefit rules.

-

Independent adult children are usually non-dependants for tax purposes. The tax-free component of any lump sum is not taxed, but the taxable taxed element can be taxed at up to 15% plus Medicare, and any untaxed element at up to 30% plus Medicare, with offsets ensuring rates do not exceed those maximums.

-

It depends. Direct payment can reduce challenge risk and may simplify administration. Paying to the estate can assist with equalisation or testamentary trust structures. However, if non-dependants benefit, tax on the taxable component will generally apply whether the payment is made directly or via the estate, subject to specific calculations.

-

Only dependants under super law or your legal personal representative can receive super death benefits from the fund. Siblings or friends who are not dependants usually cannot be nominated directly as binding beneficiaries. Instead, the benefit can be directed to your estate and then distributed to them under your will, with tax considered.

-

If you have a reversionary pension and the beneficiary is eligible, the pension may continue to them as a death benefit income stream, subject to their transfer balance cap. If there is no valid reversionary nomination, the pension stops on death and the remaining balance becomes a death benefit, which trustees must cash to eligible recipients.

-

You should review nominations whenever your circumstances change, including marriage, separation, divorce, new children, deaths, or significant balance changes, and at least every few years if nominations are lapsing. Reviews should consider super and estate law definitions of dependants, your transfer balance cap position, the form of pensions, and your broader estate planning objectives.

Superannuation & SMSFs Knowledge Bundle

- What is Superannuation and How Does It Work?

- How to Grow Your Super Balance

- Super Contribution Rules 2025

- Tax Benefits of Super Contributions

- Accessing Your Super (Before & After Retirement)

- Self-Managed Super Funds (SMSFs) Explained

- Setting Up an SMSF

- SMSF Investment Rules 2025

- SMSF Compliance & Administration

- Rolling Over Super Funds

- Ethical & Sustainable Super Funds

- Super for the Self-Employed

- Super and Divorce / Relationship Splits

- Women & Super Gap Awareness

Inheritance & Estate Planning Knowledge Bundle

- Inheritance & Estate Planning Explained

- Understanding Inheritance Tax in Australia

- Superannuation Death Benefits

- Tax Implications for Beneficiaries

- Wills, Executors & Probate

- Gifting vs Inheriting

- Blended Families & Estate Disputes

- Deceased Estates & Capital Gains

- Financial Planning After Inheritance

- Ethical Will & Legacy Planning

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.