Tax Benefits of Super Contributions for 2025–26

Summary

Super contributions are tax-effective because before-tax contributions are generally taxed at 15% in super instead of your marginal rate, after-tax contributions shift growth into a 15% or 0% tax environment, and government incentives such as co-contributions, LISTO, spouse offsets, and downsizer rules improve the after-tax outcome when used correctly.

Table of Contents

- Introduction

- How Super Contributions Create Tax Benefits

- Tax Benefits of Concessional (Before-tax) Super Contributions

- Tax Benefits of Non-concessional (After-tax) Contributions

- Tax on Earnings Inside Super Versus Outside Super

- Government Tax Incentives Linked to Super Contributions

- Super Tax Benefits for Couples

- Downsizer Contributions and Their Tax Characteristics

- How Tax on Super Contributions Connects to Tax on Withdrawals

- Self-employed and Contractor Examples

- SMSFs, Ethical Funds, and the Tax Treatment of Contributions

- When the Tax Benefits of Super Contributions May Be Less Attractive

- Approach James Hayes for Tax-focused Super Contribution Advice

- FAQs

- Superannuation & SMSFs Knowledge Bundle

Introduction

For wealth builders in their 30s and 40s, and pre-retirees or retirees in their 50s and 60s, super contributions are primarily a tax tool rather than just a savings habit. The rules in 2025–26 determine how much you can shift from personal tax rates into super’s concessional tax environment.

This article focuses on the tax side of superannuation. The mechanics of caps and eligibility are covered in Super Contribution Rules 2025, while broader strategy sits in How to Grow Your Super Balance. General super structure is addressed in What is Superannuation and How Does It Work?.

James Hayes is a financial planner based in the Sutherland Shire, working with clients across greater Sydney on super, retirement, and SMSF strategies. He does not assist with Centrelink Jobseeker support, debt consolidation using super, or early-access schemes.

How Super Contributions Create Tax Benefits

Super is taxed at three points:

When contributions go in

On investment earnings inside the fund

When benefits are paid

The overall advantage arises because:

Many contributions are taxed at 15% in the fund instead of your marginal tax rate.

Earnings in accumulation are taxed at up to 15%, with capital gains often effectively 10% for long-term assets.

Earnings on retirement-phase pensions are generally tax-free up to the transfer balance cap, which is $2.0m from 1 July 2025.

The sections below break these benefits into contribution types and income ranges.

Tax Benefits of Concessional (Before-tax) Super Contributions

Concessional contributions include:

Employer Superannuation Guarantee (SG) contributions

Salary sacrifice contributions

Personal contributions claimed as a tax deduction

From 1 July 2024, the concessional cap is $30,000 per year and remains $30,000 in 2025–26. These contributions are taxed at 15% in the fund, provided they remain within the cap.

By comparison, resident income tax rates for 2025–26 range from 16%, 30%, 37%, and 45% across the brackets above the tax-free threshold, excluding Medicare. For most working Australians, the marginal tax rate on extra income is therefore higher than 15%.

Example 1: Mid-income Earner Using Salary Sacrifice

Assume:

Salary: $100,000 in 2025–26

SG at 12%: $12,000 (already concessional)

Additional salary sacrifice: $10,000

Ignoring Medicare and offsets, the marginal income tax rate on the top portion of a $100,000 salary is 30%. That $10,000 would otherwise be taxed at 30% outside super.

Instead:

The $10,000 salary sacrifice is taxed at 15% in the fund

Immediate tax saved is 15% of $10,000 = $1,500

After contributions tax, $8,500 remains invested inside super

You have sacrificed spending power today, but $1,500 that would have been paid as income tax now remains within the super system.

Read How to Grow Your Super Balance or request James to extend examples like this over multiple years, using conservative return assumptions.

Example 2: Higher-income Earner and Division 293 Tax

If income plus concessional contributions exceed $250,000 in a year, Division 293 imposes an extra 15% tax on some concessional contributions.

For a person with:

Taxable income: $210,000

Employer and salary-sacrifice contributions: $40,000 (assume $30,000 within cap, $10,000 carried forward from prior unused caps)

Their Division 293 income is $250,000. The concessional contributions inside the cap are taxed:

15% standard contributions tax

Plus 15% Division 293 tax

So, some contributions are taxed at 30% overall. This is still lower than the 37% marginal tax rate applying to income between $135,001 and $190,000, and much lower than the 45% rate above $190,000 (ignoring Medicare).

The tax benefit narrows at higher incomes but does not disappear entirely.

If you want an easy way to map your SG, salary sacrifice, and personal deductible contributions for FY26, download the Super Contributions & Tax Planner. It helps you total everything across funds, so you stay under the cap and plan with real numbers.

Tax Benefits of Non-concessional (After-tax) Contributions

Non-concessional contributions are made from money on which you have already paid income tax. They:

Do not provide an income-tax deduction

Are not taxed on entry to the fund

Are limited by a $120,000 annual cap from 1 July 2024, which is unchanged for 2025–26, with bring-forward options for eligible members

Non-concessional contributions are essentially a trade-off: you forego liquidity and some flexibility in exchange for moving future earnings into super’s concessional tax environment.

Example 3: Comparing Investing Inside and Outside Super

Assume:

You are 55

You have $200,000 in after-tax savings

Your marginal tax rate is 30% (excluding Medicare)

You plan to invest for 10 years

If you invest outside super and earn a 5% annual return (2% income, 3% capital gains):

Income (2% of $200,000 = $4,000) is taxed at 30% each year.

Capital gains tax applies when you sell. With a 50% CGT discount, the effective rate is 15% on gains.

Inside super:

The $200,000 is contributed as a non-concessional contribution (subject to eligibility and caps).

Earnings in accumulation are taxed at up to 15%, with a one-third CGT discount on long-term capital gains, giving an effective 10% on those gains.

Once converted to a retirement-phase pension within the transfer balance cap, future earnings can become tax-free.

Over 10 years, the tax difference on earnings compounds. James will be glad to model this for you with step-by-step projections.

Planning a larger after-tax contribution or thinking about using the bring-forward rule? Figure out contribution amounts with the free Super Contributions & Tax Planner.

Tax on Earnings Inside Super Versus Outside Super

Tax benefits of contributions do not stop at entry. The ongoing tax rate on earnings is critical.

In a typical complying taxed fund:

Accumulation phase: Investment earnings (interest, rent, non-discounted capital gains) are taxed at up to 15%. Long-term capital gains on assets held for at least 12 months receive a one-third discount, making the effective CGT rate 10%.

Retirement phase: Earnings supporting a retirement-phase income stream are tax-free within your personal transfer balance cap (now $2.0m from 1 July 2025).

By contrast, investment income outside super is taxed at your marginal rate (16%, 30%, 37%, or 45% above the tax-free threshold, excluding Medicare).

For higher-income earners, this difference in ongoing earnings tax is often more significant over time than the initial tax deduction.

There is a separate Division 296 regime applying an extra 15% tax on earnings relating to super balances above $3m. This reduces the marginal tax advantage on very large balances. The Accessing Your Super (Before & After Retirement) article considers this for high-balance retirees.

Free eBook: 2025-26 Super Contributions and Tax Planner (Instant Download)

〰️

Free eBook: 2025-26 Super Contributions and Tax Planner (Instant Download) 〰️

Government Tax Incentives Linked to Super Contributions

In addition to concessional tax rates, the government provides direct incentives for low and middle-income earners.

Super Co-contribution

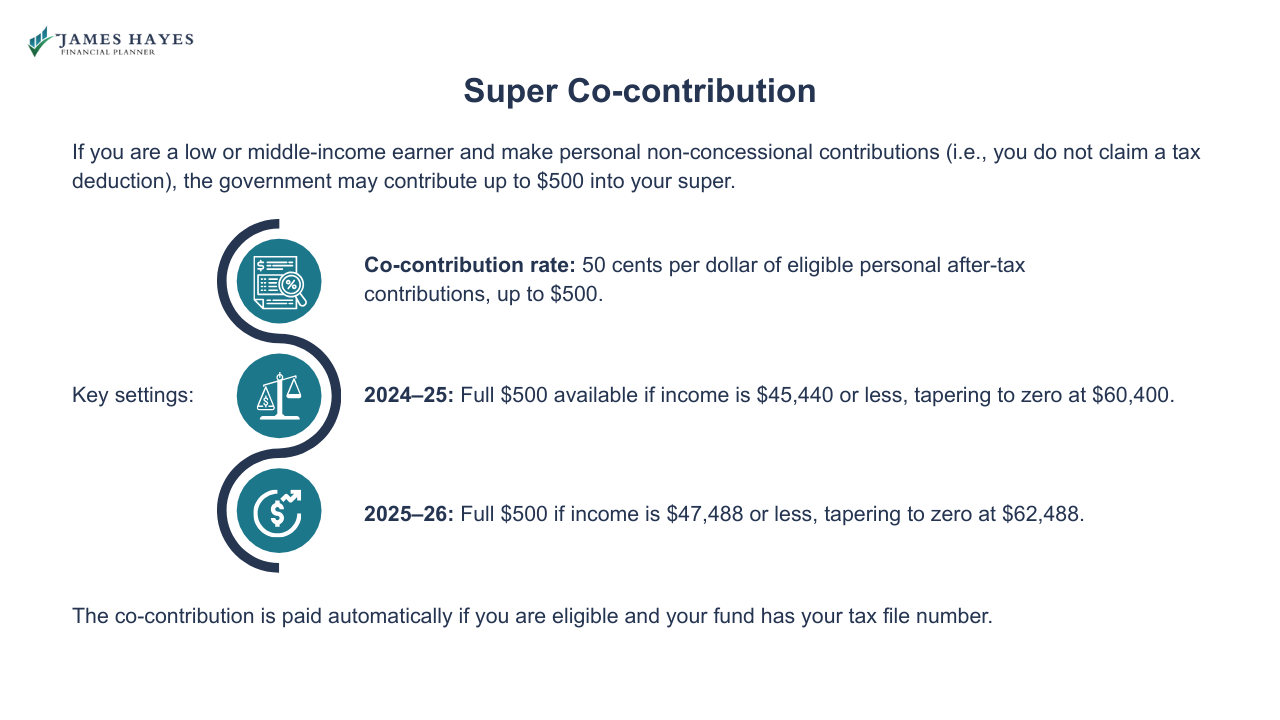

If you are a low or middle-income earner and make personal non-concessional contributions (i.e., you do not claim a tax deduction), the government may contribute up to $500 into your super.

Key settings:

Co-contribution rate: 50 cents per dollar of eligible personal after-tax contributions, up to $500.

2024–25: Full $500 available if income is $45,440 or less, tapering to zero at $60,400.

2025–26: Full $500 if income is $47,488 or less, tapering to zero at $62,488.

The co-contribution is paid automatically if you are eligible and your fund has your tax file number.

Low Income Super Tax Offset (LISTO)

LISTO is designed so low-income earners do not pay more tax on concessional contributions than on wages. If your adjusted taxable income is $37,000 or less, LISTO refunds 15% of your concessional contributions, up to $500 per year, into your super fund.

LISTO is applied automatically by the ATO and credited directly to your account. Proposed changes from 1 July 2027 would increase the income threshold to $45,000 and the maximum payment to $810, but these do not affect 2025–26 settings.

These government incentives are central to Super for the Self-Employed and Women & Super Gap Awareness, where small contributions and offsets have a measurable effect on retirement outcomes.

If you’re unsure whether you qualify for the co-contribution or LISTO this year, the Super Contributions & Tax Planner helps you organise your income and contribution details so you can quickly compare them with the current thresholds.

Super Tax Benefits for Couples

Couple strategies are often framed as balance-equalisation or estate planning issues, but they also have tax implications.

Spouse Contribution Tax Offset

If your spouse has a low income, making after-tax contributions into their super may generate a tax offset of up to $540 for you.

Broadly:

Maximum offset requires a $3,000 contribution and spouse income under $37,000, with a partial offset up to $40,000.

Your spouse must be under 75, have room under their non-concessional cap, and have a total super balance under the transfer balance cap on the prior 30 June.

This offset directly reduces your tax payable, which can improve the combined after-tax position.

Contribution Splitting

Contribution splitting allows you to request that up to 85% of the previous year’s concessional contributions (such as SG and salary sacrifice) be transferred to your spouse’s super account, subject to fund and legislative rules.

The tax benefit is indirect:

It can help manage transfer balance cap headroom for each spouse.

It can shift more of the household’s super into the older spouse’s name, or the younger spouse’s name, depending on retirement timing and Age Pension planning.

It can reduce future death benefits tax outcomes for non-dependent beneficiaries, which is explored further in Superannuation Death Benefits.

Contribution splitting does not create an extra tax deduction but affects how the tax advantages of contributions are shared over time.

If you’re trying to balance super between partners, download the Super Contributions & Tax Planner. It helps you with spouse contributions and partners’ caps.

Downsizer Contributions and Their Tax Characteristics

A downsizer contribution lets eligible older Australians contribute up to $300,000 each (up to $600,000 per couple) from the sale of an eligible main residence to super.

Key tax features:

Minimum age of 55 at the time of contribution.

Home must have been owned for at least 10 years and have been your main residence for at least part of that time.

Contribution must be made within 90 days of receiving sale proceeds.

Downsizer contributions do not count toward concessional or non-concessional caps.

Contributions are not tax-deductible, but move the funds into the super environment, where earnings are taxed at up to 15% in accumulation, or 0% in pension within the transfer balance cap.

Downsizer contributions can substantially increase the amount ultimately receiving tax-free earnings in retirement. Their impact on Age Pension tests and estate planning is addressed in Accessing Your Super (Before & After Retirement) and Superannuation Death Benefits.

How Tax on Super Contributions Connects to Tax on Withdrawals

The tax benefit of contributions should be evaluated together with how withdrawals will be taxed.

Broad principles:

Earnings on retirement-phase income streams are tax-free within the transfer balance cap; lump sums and pensions to members aged 60 or over from taxed funds are generally tax-free in their hands, subject to specific components and caps.

Withdrawals before 60, withdrawals from untaxed funds, and certain death benefits to non-dependants can be taxed at varying rates, including 15%, 30%, or higher, depending on the component and cap thresholds.

The supporting article Accessing Your Super (Before & After Retirement) covers tax on lump sums versus income streams, while Superannuation Death Benefits focuses on tax outcomes for adult children and other non-dependants.

Self-employed and Contractor Examples

If you are self-employed or a contractor, the tax mechanics are the same, but you must initiate contributions yourself.

Consider a 45-year-old sole trader with:

Taxable business income: $120,000

Marginal income tax rate on top dollars: 30% (ignoring Medicare)

Room under the concessional cap

A $20,000 personal concessional contribution:

Is taxed at 15% in the fund, costing $3,000 in contributions tax

Reduces taxable income to $100,000, saving $6,000 of income tax at 30%

Net tax saving is $3,000 for that year, plus future tax-advantaged earnings inside super

However, the contribution reduces immediate business cashflow and is preserved until access conditions are met. Those trade-offs are covered extensively in Super for the Self-Employed.

Want a clean way to link your taxable income and contributions? The Super Contributions & Tax Planner helps you draft a plan that fits irregular income without breaching caps.

SMSFs, Ethical Funds, and the Tax Treatment of Contributions

From a tax perspective, SMSFs and large public offer funds operate under the same legislation:

Concessional contributions are taxed at 15%, subject to Division 293 for high-income earners.

Non-concessional contributions are untaxed on entry, subject to the non-concessional cap and total super balance.

Earnings in accumulation are taxed at up to 15%, and pension-phase earnings within the transfer balance cap are tax-free.

What changes in an SMSF is:

The trustees’ responsibility to ensure contribution caps and eligibility rules are followed.

The risk of non-arm’s-length income (NALI) if contributions or related-party transactions are structured improperly.

Tax rules for SMSFs and related investment issues are handled in:

Similarly, ethical and sustainable super funds do not change the tax rates on contributions or earnings. They change how the money is invested. The tax outcomes still follow the general rules described here, and investment choice is addressed in Ethical & Sustainable Super Funds.

When the Tax Benefits of Super Contributions May Be Less Attractive

Super remains tax-effective, but there are situations where additional contributions are less compelling:

You expect to need funds before meeting a condition of release, and locking money into super would create short-term liquidity issues.

Your income is low enough that marginal tax is already 0% or 16%, in which case the gain from 15% contributions tax can be small or negative without LISTO.

Your combined income and concessional contributions regularly exceed $250,000, reducing benefits via Division 293 tax.

Your super balance is heading towards or above $3m, where the new Division 296 earnings tax erodes some of the concessional advantage.

These scenarios rely heavily on forward planning and are best handled with integrated modelling across super, non-super investments, and retirement spending, rather than in isolation.

If you’re weighing up SMSFs or ethical options, the Super Contributions & Tax Planner can help you keep caps, thresholds, and scenarios in one place so you can see what’s actually worth doing this year.

Approach James Hayes for Tax-focused Super Contribution Advice

James Hayes works with clients in the Sutherland Shire and Sydney CBD on:

Structuring concessional and non-concessional contributions.

Using salary sacrifice, personal deductible contributions, and carry-forward or bring-forward rules within caps.

Assessing government incentives such as LISTO and the co-contribution in the context of household cashflow.

Coordinating contributions with SMSFs, existing investments, and eventual retirement-phase income streams.

He does not assist with Centrelink Jobseeker support, debt consolidation using super, or early-access schemes outside standard conditions of release. If you want these tax rules applied to your own circumstances, you can request a complimentary 15-minute introductory call with him.

FAQs

-

The tax saving equals your marginal income tax rate minus 15%, applied to the contribution amount, ignoring Medicare and offsets. For example, if your marginal rate is 30%, each $10,000 of concessional contributions typically saves about $1,500 of income tax in that year, subject to Division 293 and contribution caps.

-

Non-concessional contributions do not create an income tax deduction, but they move investment earnings into an environment where tax is capped at 15% in accumulation, and can be 0% in retirement phase within the transfer balance cap. They are usually most effective for people with long horizons, surplus capital, and high marginal tax rates.

-

Both count as concessional contributions, are taxed at 15% in the fund, and reduce taxable income. Salary sacrifice is arranged through your employer’s payroll, while personal deductible contributions are made from after-tax income, then claimed via a notice of intent. The tax outcome is similar if total concessional contributions stay within the $30,000 cap.

-

If eligible, contributing $1,000 of after-tax money can result in a $500 government co-contribution, effectively giving a 50% immediate uplift. There is no income-tax deduction, but the combined $1,500 then earns investment returns at super tax rates. Eligibility depends on total income, non-concessional contribution status, and age-related conditions.

-

The Low Income Super Tax Offset (LISTO) refunds up to $500 of contributions tax for eligible low-income earners. If your adjusted taxable income is $37,000 or less, LISTO can refund 15% of concessional contributions into your super, neutralising the 15% contributions tax and making concessional contributions broadly tax-neutral relative to wage taxation.

-

Yes. One common approach is to realise capital gains personally, then make concessional or non-concessional contributions so future growth occurs in the super environment, where earnings tax is lower. There is no direct offset between a specific capital gain and a specific contribution, but the strategy can reduce long-term effective tax on invested capital.

-

Often, yes. Division 293 adds 15% to the 15% contributions tax on some concessional contributions, bringing the total to 30%. For people in the 37% or 45% tax brackets, paying 30% on contributions is still lower than paying 37% or 45% on the same income outside super, although the margin is smaller.

-

Contributions can provide an upfront deduction and move funds into a lower-tax environment. When you later draw a retirement-phase pension after 60 from a taxed fund, payments are generally tax-free in your hands, and earnings are tax-free within the transfer balance cap. Planning should consider both the contribution-year tax saving and the retirement withdrawal tax position.

Superannuation & SMSFs Knowledge Bundle

- What is Superannuation and How Does It Work?

- How to Grow Your Super Balance

- Super Contribution Rules 2025

- Accessing Your Super (Before & After Retirement)

- Superannuation Death Benefits

- Self-Managed Super Funds (SMSFs) Explained

- Setting Up an SMSF

- SMSF Investment Rules 2025

- SMSF Compliance & Administration

- Rolling Over Super Funds

- Ethical & Sustainable Super Funds

- Super for the Self-Employed

- Super and Divorce / Relationship Splits

- Women & Super Gap Awareness

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.