SMSF Investment Rules 2025–26

Summary

SMSF investment rules in 2025 require trustees to invest solely for retirement benefits, follow a documented investment strategy, keep all dealings at arm’s length, stay within strict related-party and in-house asset limits, meet borrowing rules for LRBAs, and avoid providing more than incidental personal benefits to members or relatives.

Table of Contents

- Introduction

- Core SMSF Investment Framework in 2025–26

- Sole Purpose Test and Personal Benefit

- SMSF Investment Strategy Requirements for 2025–26

- Related Parties, Related-Party Acquisitions, and In-House Assets

- Borrowing and Limited Recourse Borrowing Arrangements (LRBAs)

- Property Investment Rules for SMSFs in 2025

- Collectables, Personal-Use Assets, and Other Sensitive Assets

- Non-Arm’s Length Income (NALI) and Non-Arm’s Length Expenditure (NALE)

- Valuation, Diversification, and Liquidity Expectations

- Record-Keeping, Auditor Expectations, and Common Breaches

- SMSF Investment Examples for 35–50 and 55–65-Year-Olds

- How James Hayes Helps SMSF Trustees Stay Within the Rules

- FAQs

- Superannuation & SMSFs Knowledge Bundle

Introduction

For SMSF trustees and prospective trustees in the Sutherland Shire and Sydney CBD, investment rules are as important as returns. A self-managed super fund gives you control, but every decision is constrained by super law, tax law, and ATO expectations.

This article explains SMSF investment rules for 2025–26 (what trustees should know before investing), with an emphasis on:

Core legal tests – sole purpose, arm’s length, and residency

Investment strategy requirements

Related-party and in-house asset limits

Borrowing, property, collectables, and other higher-risk areas

Non-arm’s length income (NALI) and non-arm’s length expenditure (NALE)

Examples for 35–50 and 55–65 age groups

It builds on Self-Managed Super Funds (SMSFs) Explained and Setting Up an SMSF, then links into SMSF Compliance & Administration, How to Grow Your Super Balance, and Ethical & Sustainable Super Funds.

James Hayes is an ASIC-licensed financial planner based in Caringbah, advising clients across the Sutherland Shire and Sydney CBD on super, SMSFs, and retirement. He does not assist with Centrelink Jobseeker support, debt consolidation using super, or early-release schemes.

Want to check whether you’re ready for the responsibilities in SMSF investing? The SMSF Ready Assessment & Setup Roadmap helps you test your governance and risk awareness before you go further.

Core SMSF Investment Framework in 2025–26

Before looking at specific assets, it helps to understand the framework the ATO uses when reviewing SMSF investments.

At a high level, trustees must:

Maintain the fund for the sole purpose of providing retirement, or permitted death, benefits.

Have a documented investment strategy and invest in line with that strategy.

Ensure all investments are made and maintained on an arm’s length basis.

Comply with restrictions on acquiring assets from related parties.

Keep in-house assets (certain related-party investments) within the 5% limit.

Observe borrowing restrictions, including rules for limited recourse borrowing arrangements (LRBAs).

These rules apply regardless of whether you are investing in cash, ETFs, business real property, or a single property in an industrial estate.

The detailed trustee obligations and compliance processes are covered in SMSF Compliance & Administration.

Sole Purpose Test and Personal Benefit

The sole purpose test requires an SMSF to be maintained only to provide retirement benefits, or death benefits, to members or dependants.

The ATO treats an arrangement as a red flag if:

A member, or related party, obtains more than an incidental personal financial benefit from an investment, or

Fund assets are used directly or indirectly for personal use, private storage, or discounted access

Examples of breaches include:

Using SMSF property as a holiday home, even if market rent is paid

Storing collectables such as wine or art at a member’s private residence

Receiving rebates or rewards personally in return for directing SMSF investments to a particular provider

This test underpins everything else. If an arrangement is primarily designed to help you or a related party now, rather than provide retirement benefits, it is unlikely to satisfy the sole purpose test.

SMSF Investment Strategy Requirements for 2025–26

Every SMSF must have a written investment strategy that is tailored to the fund’s objectives and circumstances, and trustees must give effect to, and regularly review, that strategy.

At a minimum, the strategy must consider:

Investment objectives for each member and the fund as a whole

Risk and likely return for different asset classes, suitable for each member’s profile

Diversification, including the risks of concentration in a single asset or asset class

Liquidity and cash-flow needs, including pension payments and expenses

The ability to pay benefits when members retire or die

Whether to hold insurance for one or more members

The ATO has made it clear that generic, one-page strategies are not enough. Strategies must be specific to the fund, show how target ranges were selected, and record how trustees have assessed the risks of any lack of diversification.

The article How to Grow Your Super Balance focuses on how asset allocation and contributions fit inside these rule-sets.

Related Parties, Related-Party Acquisitions, and In-House Assets

Investment rules are particularly strict when dealing with related parties. A related party of an SMSF includes:

Members

Standard employer sponsors

Certain relatives of members and entities controlled by members or their relatives

Acquiring Assets from Related Parties

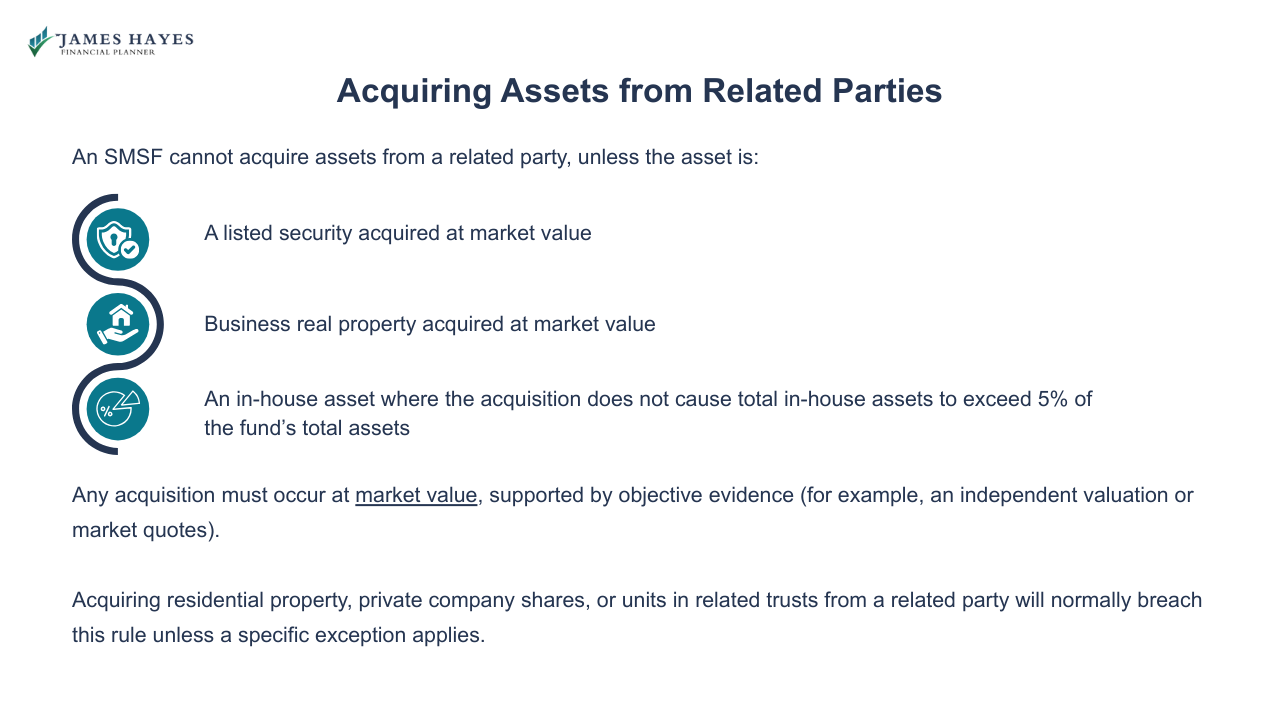

An SMSF cannot acquire assets from a related party, unless the asset is:

A listed security acquired at market value

Business real property acquired at market value

An in-house asset where the acquisition does not cause total in-house assets to exceed 5% of the fund’s total assets

Any acquisition must occur at market value, supported by objective evidence (for example, an independent valuation or market quotes).

Acquiring residential property, private company shares, or units in related trusts from a related party will normally breach this rule unless a specific exception applies.

In-house Assets and the 5% Cap

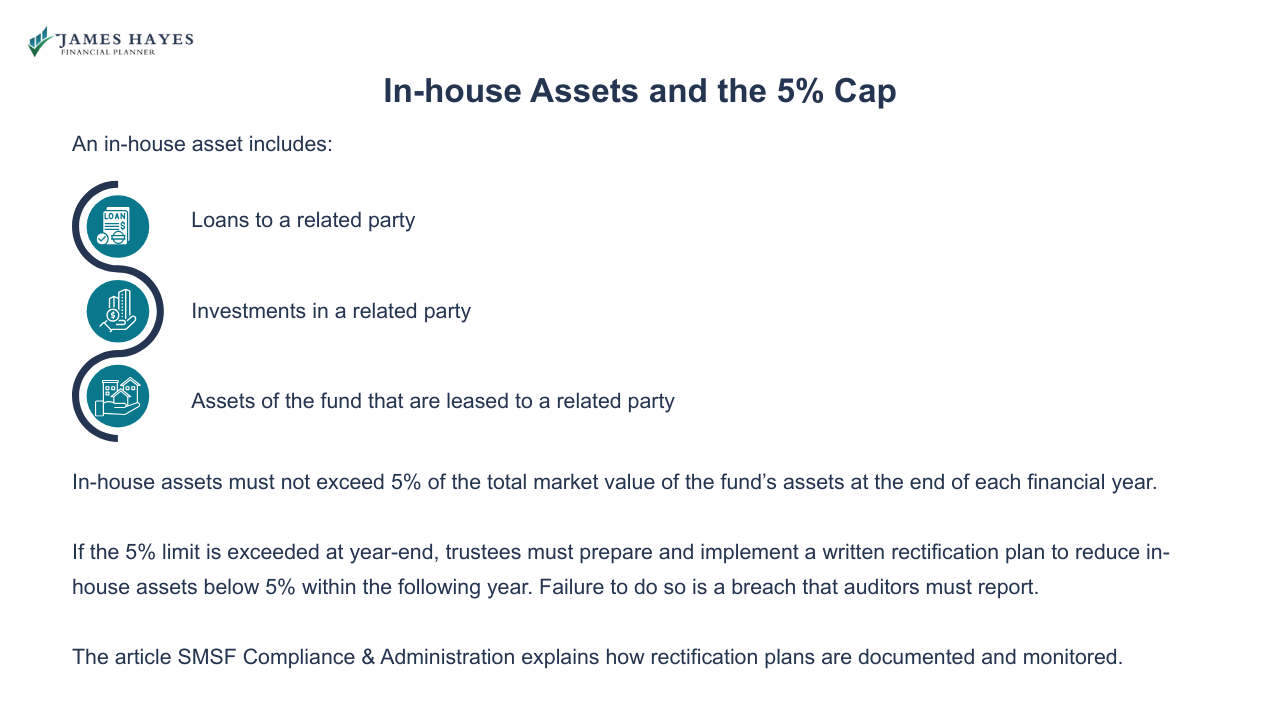

An in-house asset includes:

Loans to a related party

Investments in a related party

Assets of the fund that are leased to a related party

In-house assets must not exceed 5% of the total market value of the fund’s assets at the end of each financial year.

If the 5% limit is exceeded at year-end, trustees must prepare and implement a written rectification plan to reduce in-house assets below 5% within the following year. Failure to do so is a breach that auditors must report.

The article SMSF Compliance & Administration explains how rectification plans are documented and monitored.

Borrowing and Limited Recourse Borrowing Arrangements (LRBAs)

SMSFs are generally prohibited from borrowing, with limited exceptions. One key exception is a limited recourse borrowing arrangement (LRBA) used to acquire a permitted single acquirable asset, such as property or a parcel of listed shares.

Important LRBA rules include:

The asset must be held on separate trust (a bare trust) for the SMSF.

Recourse of the lender is limited to the asset in the LRBA, not to other fund assets.

The arrangement must be consistent with the fund’s investment strategy and risk profile.

Additional borrowings or redraws cannot be used for improvements that change the character of the original asset.

Where the lender is a related party, the terms must be consistent with arm’s length conditions (interest rate, security, loan-to-value ratio, and term). ATO Practical Compliance Guidelines 2016/5 set out safe harbour terms often used for related-party LRBAs, including indicative interest rates (for example, 9.35% for real property in 2024–25).

Poorly structured LRBAs can result in non-arm’s length income (NALI), where income from the asset is taxed at 45%, so cross-checking with SMSF Compliance & Administration and specialist advice is essential.

If you're trying to work out whether you have the governance habits needed for arrangements like LRBAs, the SMSF Ready Assessment & Setup Roadmap provides a simple way to test that readiness.

Property Investment Rules for SMSFs in 2025

Property remains a common SMSF asset class, particularly for business owners in the Shire and CBD. The core rules are stricter than general property investment rules.

For both residential and commercial property, the investment must:

Satisfy the sole purpose test

Be expressly allowed by the trust deed and consistent with the investment strategy

Be acquired and maintained on arm’s length terms, including purchase price and rent

For residential property, additional restrictions apply:

It cannot be acquired from a related party, except in limited grandfathered circumstances.

It must not be rented to a related party, even at market rent.

It must not provide current-day accommodation or holiday use for members or relatives.

For business real property (for example, an office or warehouse used wholly and exclusively in a business), the SMSF may be able to:

Acquire the property from a related party at market value

Lease the property to a related-party business at market rent under commercial terms

The definition of business real property, and mixed-use property issues (such as farms with dwellings), are detailed topics covered further in Self-Managed Super Funds (SMSFs) Explained and Super for the Self-Employed.

Moneysmart and ATO guidance both stress the need to understand property rules, costs, and risks before using an SMSF to buy property.

Free eBook: SMSF Ready Assessment and Setup Roadmap (Instant Download)

〰️

Free eBook: SMSF Ready Assessment and Setup Roadmap (Instant Download) 〰️

Collectables, Personal-Use Assets, and Other Sensitive Assets

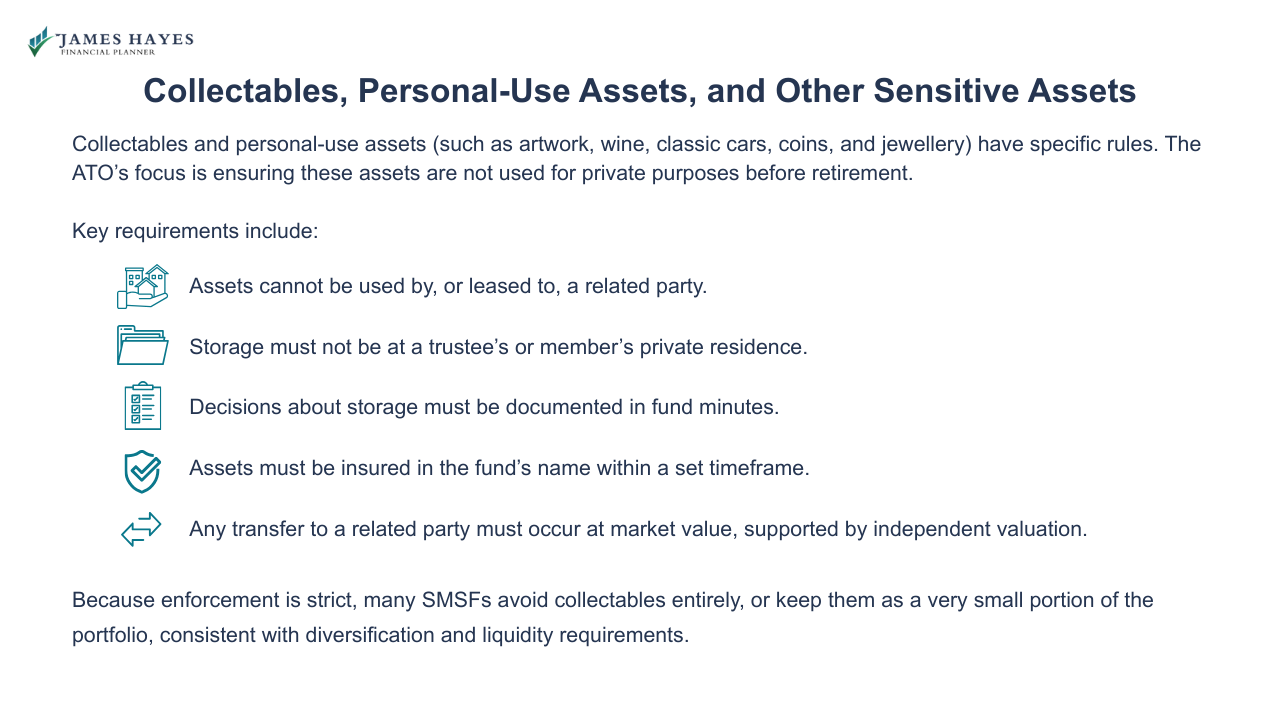

Collectables and personal-use assets (such as artwork, wine, classic cars, coins, and jewellery) have specific rules. The ATO’s focus is ensuring these assets are not used for private purposes before retirement.

Key requirements include:

Assets cannot be used by, or leased to, a related party.

Storage must not be at a trustee’s or member’s private residence.

Decisions about storage must be documented in fund minutes.

Assets must be insured in the fund’s name within a set timeframe.

Any transfer to a related party must occur at market value, supported by independent valuation.

Because enforcement is strict, many SMSFs avoid collectables entirely, or keep them as a very small portion of the portfolio, consistent with diversification and liquidity requirements.

Non-Arm’s Length Income (NALI) and Non-Arm’s Length Expenditure (NALE)

NALI rules apply where an SMSF receives income that is higher than expected, or pays less than commercial rates for expenses, due to non-arm’s length dealings.

Examples include:

Acquiring an asset at less than market value from a related party

Paying below-market interest on a related-party LRBA

Receiving services from a related party on terms that affect the fund’s expenses or structure

If NALI applies, all income from the relevant arrangement, including capital gains, can be taxed at 45%, instead of concessional rates.

From 1 July 2023, Treasury and ATO guidance has also focused on NALE, where general fund expenses are not charged on arm’s length terms, though some transitional concessions apply. This area is technical and often requires specialist input.

Tax Benefits of Super Contributions and SMSF Compliance & Administration cover the tax mechanisms in more depth.

Valuation, Diversification, and Liquidity Expectations

The ATO expects SMSFs to value assets at market value each year, using appropriate evidence such as independent valuations, comparable sales, or observable market data.

Trustees must also:

Demonstrate they have considered diversification, especially where large portions of the fund are in a single property or asset.

Show they have assessed liquidity, including the ability to pay minimum pensions and tax liabilities.

Provide documentation where the fund deliberately maintains concentrated positions, explaining why that approach remains consistent with members’ retirement objectives.

This documentation sits inside the investment strategy and trustee minutes, both of which auditors and the ATO scrutinise.

Record-Keeping, Auditor Expectations, and Common Breaches

Investment rules cannot be separated from record-keeping. Approved SMSF auditors must review both the financial statements and compliance each year, including:

Evidence of asset ownership in the fund’s name

Supporting valuations

Documentation of related-party transactions, leases, and loans

Investment strategy and review minutes

Common breaches reported to the ATO include:

Loans to members or relatives

Breaches of the 5% in-house asset limit

Acquisitions from related parties outside the allowed categories

Early-release schemes disguised as investments

SMSF Compliance & Administration explains the consequences of breaches, rectification plans, and ATO penalty powers. Self-Managed Super Funds (SMSFs) Explained sets out trustee duties more broadly.

SMSF Investment Examples for 35–50 and 55–65-Year-Olds

Rules can seem abstract. The examples below show how they apply in common situations. These are simplified and assume complying taxed funds.

Example 1: 45-Year-Old Business Owner Buying Premises

A 45-year-old in the Shire runs a small engineering firm and wants their SMSF to buy a factory that the business will lease.

Key rule points:

If the property qualifies as business real property used wholly and exclusively in the business, the SMSF may acquire it from a related party at market value.

The business must pay market rent under a written lease.

The investment must align with the investment strategy, and the fund must manage diversification and liquidity metrics.

Further property details are covered in Super for the Self-Employed and SMSF Investment Rules 2025 is the anchor article for that cluster.

Example 2: 60-Year-Old Couple with a Property-Heavy SMSF

A couple in their early 60s have an SMSF with 80% of assets in a single commercial property and 20% in cash and fixed interest.

Rule implications:

The investment strategy must explicitly discuss concentration risk, diversification, and liquidity.

Trustees must be able to show how they will meet pension payments and expenses if the property is vacant or needs repairs.

Valuations and lease terms must support arm’s length dealings.

The sustainability of this structure in retirement is explored further in Accessing Your Super (Before & After Retirement) and How to Grow Your Super Balance.

SMSF readiness varies by age. Use the SMSF Ready Assessment & Setup Roadmap to assess whether the trustee workload fits your circumstances.

How James Hayes Helps SMSF Trustees Stay Within the Rules

ASIC and the ATO continue to highlight poor-quality SMSF advice where investment risk, costs, and compliance duties are not adequately explained.

Within that regulatory environment, James works with SMSF trustees in the Sutherland Shire and Sydney CBD to:

Align investment strategies with the legal framework explained here.

Integrate contribution decisions (see Super Contribution Rules 2025 and Tax Benefits of Super Contributions) with investment selection.

Assess property, business, and ethical investment proposals against sole purpose, related-party, in-house asset, and NALI rules.

Coordinate investment structures with retirement income planning and death-benefit strategies from Accessing Your Super (Before & After Retirement) and Superannuation Death Benefits.

He does not promote SMSFs for early access, debt consolidation, or high-risk arrangements that sit at odds with ATO guidance. Book a complimentary 15-minute call with him.

FAQs

-

The core rule is the sole purpose test. Every investment and arrangement must be for the sole purpose of providing retirement or permitted death benefits, not current-day personal benefit. This test sits above related-party, in-house asset, borrowing, and NALI rules, and is the starting point for any SMSF investment proposal.

-

Generally, no. An SMSF cannot acquire residential property from a related party, and it cannot lease residential property to a related party, even at market rent. The property must satisfy the sole purpose test and must not provide current-day accommodation or holiday use for members, relatives, or related entities.

-

In-house assets include loans to related parties, investments in related entities, and assets leased to related parties. At each year-end, they must not exceed 5% of the SMSF’s total asset value. If they do, trustees must prepare and implement a written plan to reduce them below 5% during the following year.

-

Possibly, but only within strict limits. A loan to your company is usually an in-house asset and counts towards the 5% cap. The loan must be on arm’s length terms with proper documentation. Any breach of the in-house asset limit or arm’s length rules can trigger compliance issues and potential NALI.

-

Borrowing must occur via a limited recourse borrowing arrangement, with the property held in a separate holding trust. The loan must be limited in recourse to that asset, consistent with the investment strategy, and on arm’s length terms. Related-party loans must meet ATO safe harbour conditions or be benchmarked carefully.

-

You must consider diversification in your investment strategy and document your reasoning. The ATO does not force specific allocations, but concentrated positions, such as a single property or large parcel of unlisted shares, require clear documentation of risks and mitigants. Auditors and the ATO expect evidence that diversification has been assessed.

-

At least annually, and whenever there is a significant change in fund or member circumstances, such as starting a pension, large contributions, major asset purchases, or membership changes. Reviews should produce dated minutes, confirm whether the strategy remains appropriate, and record any changes in target ranges, diversification, liquidity, or insurance positions.

-

If income is treated as non-arm’s length, the ATO can tax all income and capital gains from the relevant arrangement at 45%, rather than concessional super rates. This can occur where assets are acquired cheaply, related-party loans are mis-priced, or services are structured in ways that distort true commercial terms.

Superannuation & SMSFs Knowledge Bundle

- What is Superannuation and How Does It Work?

- How to Grow Your Super Balance

- Super Contribution Rules 2025

- Tax Benefits of Super Contributions

- Accessing Your Super (Before & After Retirement)

- Superannuation Death Benefits

- Self-Managed Super Funds (SMSFs) Explained

- Setting Up an SMSF

- SMSF Compliance & Administration

- Rolling Over Super Funds

- Ethical & Sustainable Super Funds

- Super for the Self-Employed

- Super and Divorce / Relationship Splits

- Women & Super Gap Awareness

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.