Rolling Over Super Funds

Summary

Rolling over super means transferring your existing balance from one fund to another without withdrawing it. It is not a contribution and usually has no tax on transfer, but it can affect fees, insurance, investment options, and timing of returns. The process is now mostly digital and must follow SuperStream rules.

Table of Contents

- Introduction

- What Is a Rollover of Super?

- Why Roll Over or Consolidate Super Accounts?

- How to Find and Review Existing Super Accounts

- Rolling Over Between APRA-regulated Funds

- SuperStream, Electronic Service Address (ESA), and Data Requirements

- Rolling Over to an SMSF

- Rolling Over from an SMSF to an APRA-Regulated Fund

- Tax Treatment of Rollovers

- Insurance Implications When Rolling Over Super

- Investment, Ethical, and ESG Considerations When Consolidating

- Common Risks and Issues When Rolling Over

- Rolling Over Super in the Context of Divorce and Relationship Splits

- How James Hayes Works with Clients on Rollover Decisions

- FAQs

- Superannuation & SMSFs Knowledge Bundle

Introduction

Most employed Australians accumulate multiple super accounts over time. For wealth builders in their 30s and 40s, and pre-retirees or retirees in their 50s and 60s, rolling over and consolidating super is often a practical way to reduce fees, simplify investments, and prepare for retirement or SMSF strategies.

This article explains:

What a rollover is and how it differs from a contribution or withdrawal

Reasons to roll over or consolidate super

How to roll over between APRA-regulated funds

How to roll over to, or from, a self-managed super fund (SMSF)

Insurance, investment, and estate-planning implications

It sits alongside:

What is Superannuation and How Does It Work? (core structure of the system)

How to Grow Your Super Balance (contribution and investment decisions)

Super Contribution Rules 2025 and Tax Benefits of Super Contributions (caps and tax on contributions)

Self-Managed Super Funds (SMSFs) Explained, Setting Up an SMSF, and SMSF Compliance & Administration (SMSF-specific practicalities)

Women & Super Gap Awareness and Super and Divorce / Relationship Splits (structural gaps and splitting issues)

James Hayes is an ASIC-licensed financial planner based in Caringbah, working with clients across the Sutherland Shire and Sydney CBD on super, retirement, and SMSF planning. He does not assist with Centrelink Jobseeker support, debt consolidation using super, or schemes aimed at early access.

What Is a Rollover of Super?

A rollover is a transfer of super benefits from one complying super fund to another, without paying the money to you personally. For tax and contribution-cap purposes, it is treated as a super benefit transfer, not a contribution or withdrawal, provided both funds are complying.

Under tax law, rollovers are covered by specific provisions; they are not counted toward concessional or non-concessional contributions, and the tax components (tax-free and taxable) must be preserved and reported to the receiving fund. The transfer is generally not taxed at the time of the rollover when moving between Australian regulated funds.

This is distinct from:

Contributions: New money entering the super system from you or an employer

Withdrawals: Money leaving the super system and paid to you or your estate

Those are examined in Super Contribution Rules 2025 and Accessing Your Super (Before & After Retirement).

Why Roll Over or Consolidate Super Accounts?

Rolling over super is primarily an efficiency and risk-management decision. It is not inherently beneficial or harmful; the detail matters.

Common reasons to consolidate include:

Reducing duplicate fees across multiple small accounts

Simplifying investment management and reporting

Aligning your super with specific investment or ethical preferences (see Ethical & Sustainable Super Funds)

Preparing to use an SMSF, where balances are held in a single structure

Improving oversight of insurance, estate nominations, and contribution strategy

Potential reasons not to consolidate particular accounts can include:

Valuable legacy insurance benefits that may not be replicable on the same terms

Unique defined benefit entitlements that should not be rolled over without specialist advice

Promotional fee discounts, or closed products with distinctive features

The How to Grow Your Super Balance article covers how rollover decisions fit into a broader strategy rather than being treated as a one-off admin task.

If you want a simple way to compare funds side by side before consolidating, the Super Fund Comparison & Rollover Workbook gives you tables for fees, investments, insurance, and performance so nothing gets missed.

How to Find and Review Existing Super Accounts

Before rolling over anything, you need a confirmed list of accounts and their features.

Most people can:

Use myGov linked to the ATO to view current super accounts, ATO-held super, and lost super (this uses ATO records and SuperStream identifiers).

Request current balances, unit prices, and insurance details from each fund.

Obtain the latest product disclosure statement (PDS) and insurance guide for each fund to compare fees, investments, and options.

The What is Superannuation and How Does It Work? post explains how myGov and ATO data interact with funds, rollovers, and contributions.

At this stage, it is important to note:

Current insurance cover types, sums insured, and premium structures

Binding or non-binding death benefit nominations or reversionary pensions

Any defined benefit components, which usually require specialist analysis before changes

These non-balance features often drive whether a rollover is advisable.

Before you roll anything over, it helps to see all your accounts and their features in one place. The Super Fund Comparison & Rollover Workbook lets you list each fund, capture insurance, and review nominations clearly.

Rolling Over Between APRA-regulated Funds

For most people without SMSFs, rollovers happen between APRA-regulated funds such as retail, industry, or corporate funds.

The process usually involves:

Choosing the Receiving Fund

You identify which fund will be your primary (or only) fund going forward, taking into account investment menus, fees, insurance, and service. See Ethical & Sustainable Super Funds and How to Grow Your Super Balance for selection frameworks.

Initiating the Rollover

In many cases you can request the rollover via the receiving fund’s online portal, or via myGov using ATO online services. These systems use SuperStream, which requires accurate fund identifiers and bank details.

Providing Required Details

Processing by the Transferring Fund

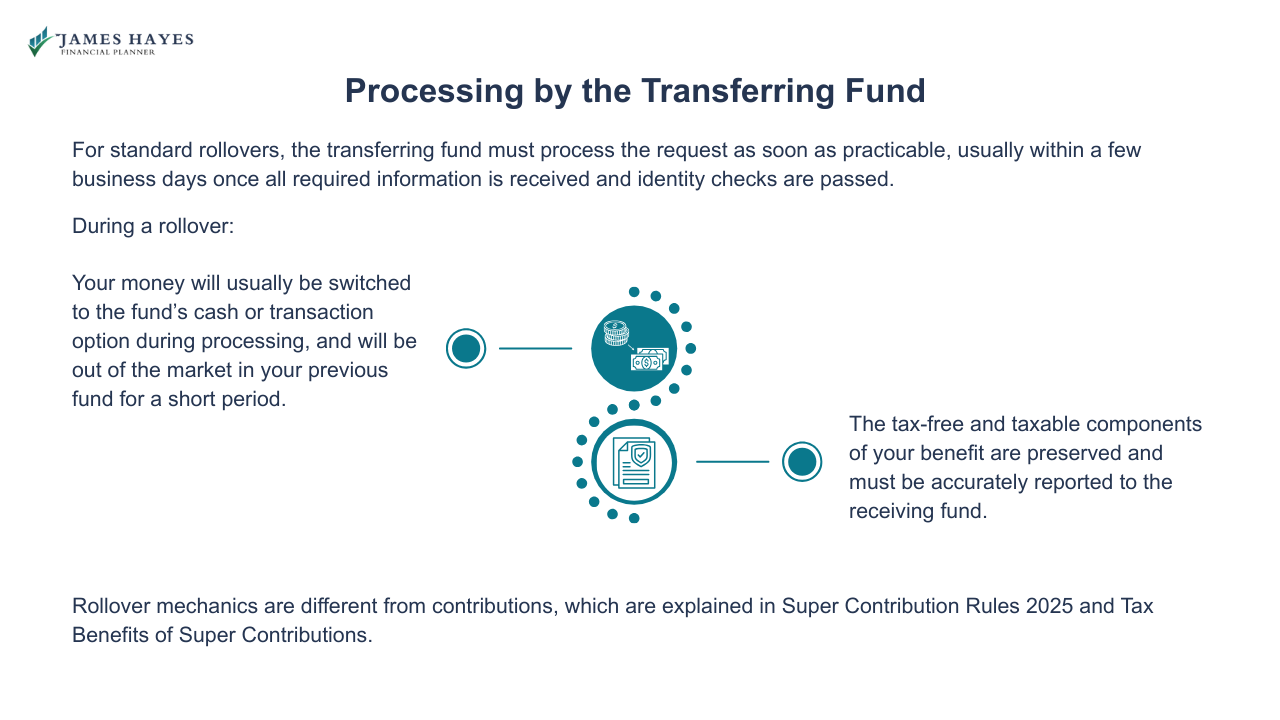

For standard rollovers, the transferring fund must process the request as soon as practicable, usually within a few business days once all required information is received and identity checks are passed.

During a rollover:

Your money will usually be switched to the fund’s cash or transaction option during processing, and will be out of the market in your previous fund for a short period.

The tax-free and taxable components of your benefit are preserved and must be accurately reported to the receiving fund.

Rollover mechanics are different from contributions, which are explained in Super Contribution Rules 2025 and Tax Benefits of Super Contributions.

Need help organising the admin details—like fund identifiers, insurance checks, and what to confirm before requesting the rollover? The Super Fund Comparison & Rollover Workbook includes a practical checklist you can work through.

SuperStream, Electronic Service Address (ESA), and Data Requirements

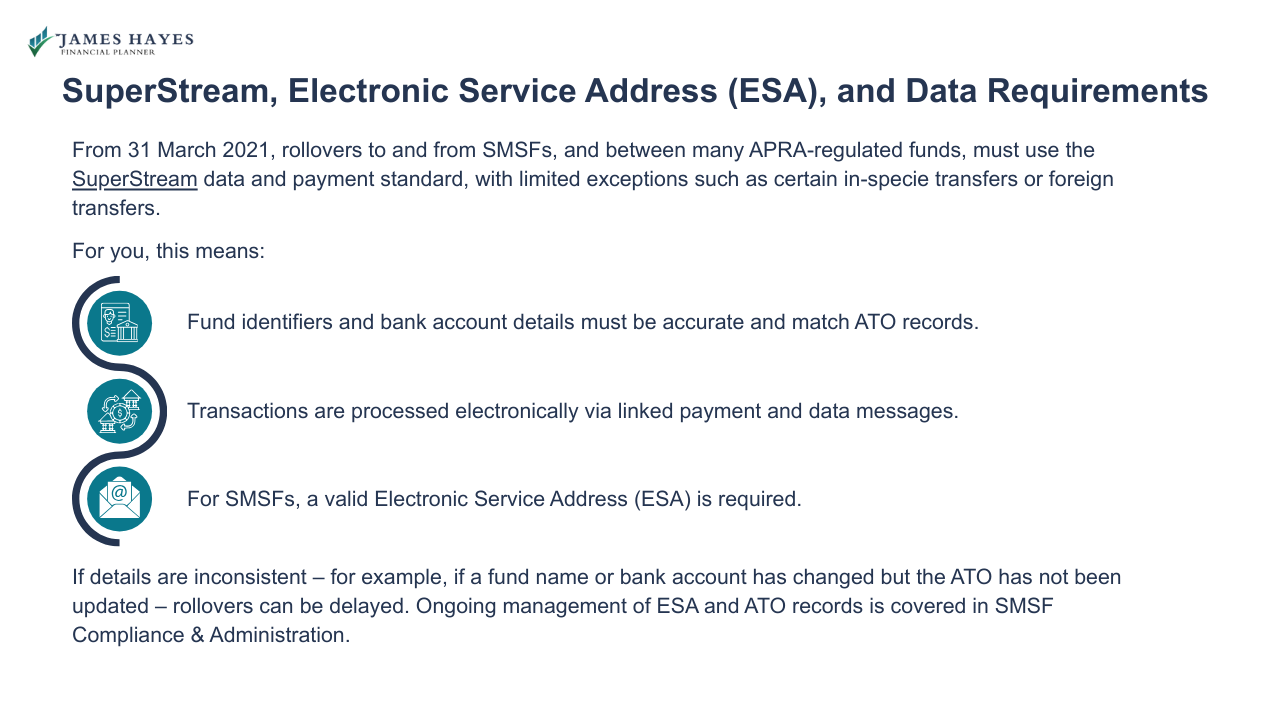

From 31 March 2021, rollovers to and from SMSFs, and between many APRA-regulated funds, must use the SuperStream data and payment standard, with limited exceptions such as certain in-specie transfers or foreign transfers.

For you, this means:

Fund identifiers and bank account details must be accurate and match ATO records.

Transactions are processed electronically via linked payment and data messages.

For SMSFs, a valid Electronic Service Address (ESA) is required.

If details are inconsistent – for example, if a fund name or bank account has changed but the ATO has not been updated – rollovers can be delayed. Ongoing management of ESA and ATO records is covered in SMSF Compliance & Administration.

Free eBook: Super Fund Comparison & Rollover Workbook

〰️

Free eBook: Super Fund Comparison & Rollover Workbook 〰️

Rolling Over to an SMSF

For clients moving from an APRA-regulated fund into an SMSF, the rollover is a key step after the SMSF has been properly established and registered.

In sequence, you would normally:

Set Up and Register the SMSF

This includes executing the trust deed, appointing trustees or corporate trustee directors, obtaining an ABN/TFN, opening a bank account, documenting an investment strategy, and obtaining an ESA. These steps are explained in Setting Up an SMSF.

Confirm SuperStream Readiness

The SMSF must have:

A valid ESA from a messaging provider

A recorded ABN and bank account with the ATO

Accurate member details in ATO records

Request the Rollover

You submit a rollover request from the APRA-regulated fund to the SMSF, typically through the transferring fund’s portal or forms, providing the SMSF’s ABN, ESA, and bank account details.

Monitor Completion and Allocate Contributions

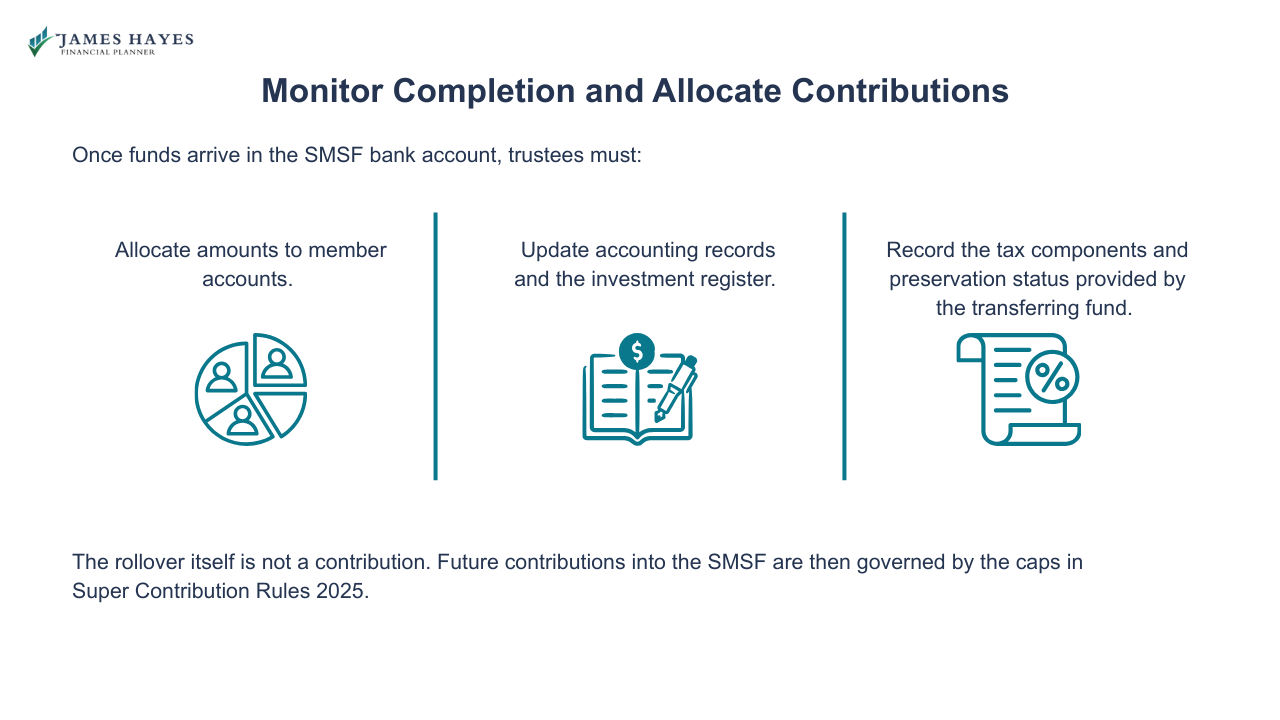

Once funds arrive in the SMSF bank account, trustees must:

Allocate amounts to member accounts.

Record the tax components and preservation status provided by the transferring fund.

Update accounting records and the investment register.

The rollover itself is not a contribution. Future contributions into the SMSF are then governed by the caps in Super Contribution Rules 2025.

Rolling Over from an SMSF to an APRA-Regulated Fund

Some trustees decide to wind up an SMSF or to move member balances back to an APRA-regulated fund, often due to time constraints, cost, or succession-planning issues. The mechanics are similar but run in the opposite direction.

The process typically requires:

Ensuring financial statements and asset valuations are up to date.

Selling or transferring SMSF investments so that benefits can be rolled over as cash or in permitted forms.

Using SuperStream to initiate the rollover to the receiving fund, with correct member and SMSF details.

Making sure all member balances are reduced to zero, then completing the SMSF wind-up tasks (final audit, final annual return, notifying the ATO, closing bank accounts).

The wind-up process is handled in detail in SMSF Compliance & Administration. This article focuses on the rollover itself rather than total fund closure.

Tax Treatment of Rollovers

From a tax-planning perspective, the key points are:

A rollover between complying funds is not treated as a concessional or non-concessional contribution and does not use contribution caps.

The tax-free and taxable components of your super interest must be preserved and reported to the receiving fund. Those components affect the tax on future withdrawals or death benefits.

The rollover does not reset the underlying tax components or your transfer balance cap position, although starting a new pension in the receiving fund can create a reportable event.

The earnings in each fund will be subject to normal tax rules (15% in accumulation, 0% on retirement-phase pensions within the transfer balance cap). Tax on withdrawals and death benefits are dealt with in Accessing Your Super (Before & After Retirement) and Superannuation Death Benefits.

Insurance Implications When Rolling Over Super

Insurance is one of the main areas where rollovers can have unintended consequences.

Most APRA-regulated funds provide:

When rolling over and closing an account, you usually cancel the associated insurance. Once cancelled, reinstating cover on the same terms may not be possible, especially if health has changed.

Best practice before rollover includes:

Checking existing sums insured, waiting periods, and definitions

Confirming whether cover in the new fund will start automatically, or require underwriting

Considering whether to keep a small balance in the old fund purely to preserve valuable cover (subject to fee, balance, and administration implications)

These insurance issues intersect with the retirement and estate goals discussed in How to Grow Your Super Balance and Superannuation Death Benefits.

Investment, Ethical, and ESG Considerations When Consolidating

Rolling over can change your investment menu and ESG characteristics. Many now use rollovers to align their super with:

Specific risk profiles and asset allocations

Targeted exposure to Australian and global equities, fixed interest, infrastructure, or property

Ethical or sustainable investment preferences, as outlined in Ethical & Sustainable Super Funds

Before consolidating, you should compare:

Default MySuper options versus tailored investment choices

Fee structures, including performance fees

Historical risk and return characteristics, noting that past performance is not a guarantee but can illustrate volatility

These comparisons are addressed, at portfolio level, in How to Grow Your Super Balance.

Common Risks and Practical When Rolling Over

Rollovers are procedural, but they still carry practical risks.

Common issues include:

Short periods out of the market, where funds are in cash during processing, which can be material if markets move sharply.

Incorrect fund or member details, causing delays or rejection.

Employer contributions continuing to go to the old fund if payroll details are not updated.

Rolling out of defined benefit or legacy products without modelling impacts.

Losing insurance unintentionally.

These risks are manageable with planning and documentation, but they need to be understood as part of a deliberate strategy rather than assumed to be minor details.

To reduce the risk of delays or missed details, the Super Fund Comparison & Rollover Workbook includes a rollover checklist covering data accuracy, insurance, employer updates, and what to confirm after the transfer.

Rolling Over Super in the Context of Divorce and Relationship Splits

Rollovers interact with family-law splits and post-separation planning.

In a relationship breakdown:

A superannuation agreement or court order can require part of one party’s super to be split and transferred to the other spouse’s super account.

The receiving spouse may then choose to roll over that entitlement into a preferred fund or SMSF, subject to fund rules and costs.

The rules around splitting, flagging, and implementing orders are examined in Super and Divorce / Relationship Splits, which should be considered before any rollover that might affect negotiations or court proceedings.

How James Hayes Works with Clients on Rollover Decisions

Rolling over super is often presented as a simple consolidation exercise. In practice, it intersects with contribution strategies, SMSFs, insurance, and long-term retirement goals.

James typically:

Reviews each existing super account for fees, investments, insurance, and tax components.

Assesses whether consolidation supports the strategies in How to Grow Your Super Balance, Super Contribution Rules 2025, and Tax Benefits of Super Contributions.

Evaluates whether moving to, or from, an SMSF is appropriate. (see Self-Managed Super Funds (SMSFs) Explained and Setting Up an SMSF).

Coordinates timing with retirement planning and estate objectives (see Accessing Your Super (Before & After Retirement and Superannuation Death Benefits).

He does not use rollovers as a way to withdraw super early, consolidate personal debts, or circumvent contribution rules.

FAQs

-

No. A rollover between complying super funds is treated as a transfer of existing benefits, not a contribution. It does not use concessional or non-concessional contribution caps. The tax-free and taxable components are preserved and reported to the receiving fund, which then use those components for future tax calculations on withdrawals or death benefits.

-

Generally not, if both funds are Australian complying funds. The rollover itself is not taxed, and it does not trigger capital gains tax for you personally. The tax-free and taxable components of your benefit are preserved and move to the new fund, where they influence later withdrawal and death-benefit tax outcomes.

-

You usually choose the new fund first, then request a rollover via the new fund’s forms or through myGov. You provide your TFN, fund identifiers, and member details. The transferring fund processes the rollover using SuperStream once all details are correct, and the amount is paid to your new fund account.

-

You should review each fund’s fees, investment options, and performance characteristics, along with insurance cover, death-benefit nominations, and any defined benefit or legacy features. Insurance is especially important, because rolling over and closing an account usually cancels cover. You should also confirm whether employer contributions will be redirected correctly post-rollover.

-

After the SMSF is set up and registered, with an ABN, TFN, bank account, and Electronic Service Address, you request a rollover from your existing fund to the SMSF. The transferring fund uses SuperStream to send the money and data. Trustees then allocate amounts to member accounts and update records accordingly.

-

Yes, provided the receiving fund accepts the rollover. Trustees must ensure accounts are valued, investments are sold or transferred appropriately, and SuperStream is used where required. The rollover must be properly documented in the SMSF’s accounts. If the SMSF is being wound up, final audits and returns must also be completed.

-

Yes, potentially. If you close an account, associated life, TPD, or income protection cover is usually cancelled. New cover in another fund may involve waiting periods, different definitions, or underwriting. Before rolling over, you should compare insurance terms and consider whether to keep some cover in an existing fund, subject to fees.

-

You should review your super structure when you change jobs, accumulate new accounts, change investment preferences, start or stop an SMSF, experience health changes, or approach retirement. For many people, reviewing super funds and potential rollovers forms part of an annual or biennial review linked to the broader retirement and estate plan.

Superannuation & SMSFs Knowledge Bundle

- What is Superannuation and How Does It Work?

- How to Grow Your Super Balance

- Super Contribution Rules 2025

- Tax Benefits of Super Contributions

- Accessing Your Super (Before & After Retirement)

- Superannuation Death Benefits

- Self-Managed Super Funds (SMSFs) Explained

- Setting Up an SMSF

- SMSF Investment Rules 2025

- SMSF Compliance & Administration

- Ethical & Sustainable Super Funds

- Super for the Self-Employed

- Super and Divorce / Relationship Splits

- Women & Super Gap Awareness

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.