How to Grow Your Super Balance

Summary

To grow your super balance, increase how much goes in, keep it invested for long periods, and make sure the structure is efficient. That usually means using concessional caps, adding extra savings when cashflow allows, choosing an appropriate investment mix, consolidating accounts, and reviewing your plan regularly at fixed intervals.

Table of Contents

- Introduction

- The Three Levers That Drive Your Super Balance

- Know the Current Superannuation Contribution Caps

- Superannuation Contribution Strategies While You Are Working

- Government and Spouse Support for Building Super Balances

- Superannuation Investment Strategy

- Structural Moves That Grow Your Super Balance

- Super Strategies by Life Stage

- Using SMSFs as Part of a Growth Strategy

- Behavioural Habits That Support Super Growth

- How James Hayes Works with Clients to Grow Super

- FAQs

- Superannuation & SMSFs Knowledge Bundle

Introduction

For many households in the Sutherland Shire and Sydney CBD, superannuation will fund a large portion of retirement income. The question is not simply “what is super?” – that is covered in What is Superannuation and How Does It Work? – but how to grow your balance in a structured way.

This guide focuses on practical growth strategies for two groups:

Wealth builders (35–50) who still have time for compounding to work.

Pre-retirees and retirees (55–65) who are preparing to draw income from super.

James Hayes is an ASIC-licensed financial planner based in Caringbah with 15+ years’ experience working with clients across the Sutherland Shire and Sydney CBD on super, investments, and retirement planning. He does not assist with Centrelink Jobseeker claims, debt consolidation schemes using super, or early-release arrangements that attempt to access super outside the law.

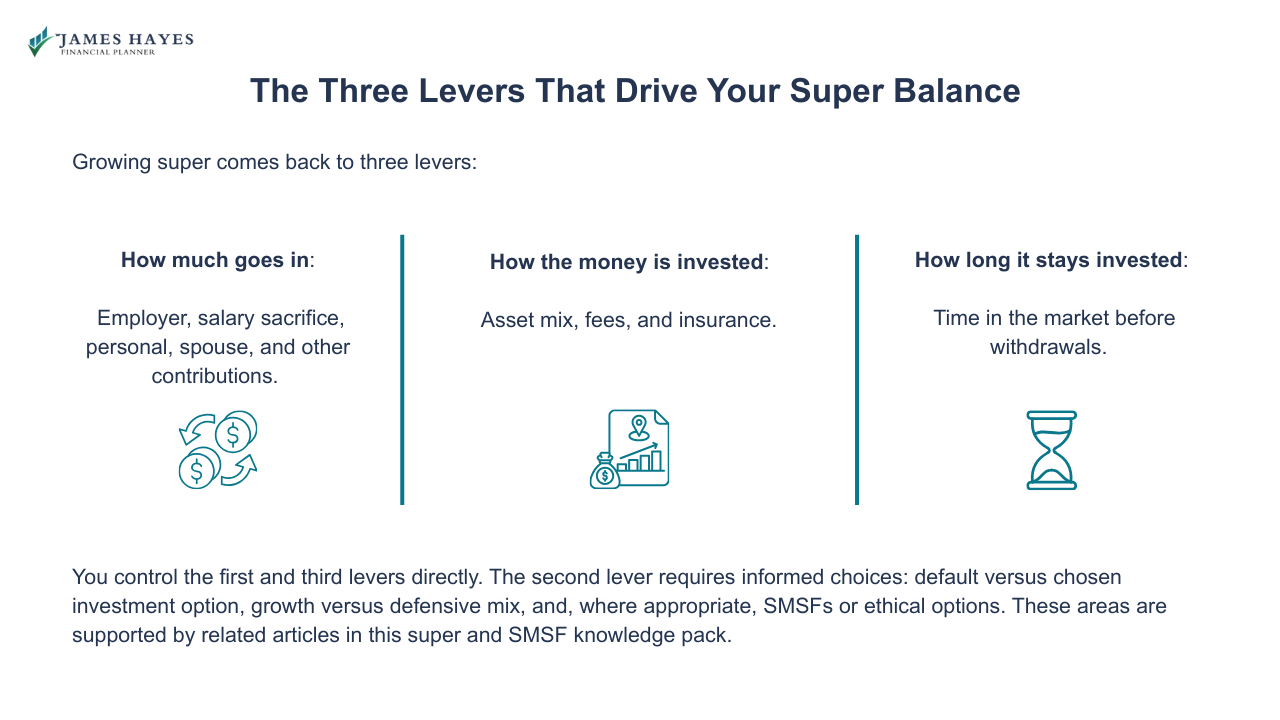

The Three Levers That Drive Your Super Balance

Growing super comes back to three levers:

How much goes in: Employer, salary sacrifice, personal, spouse, and other contributions.

How the money is invested: Asset mix, fees, and insurance.

How long it stays invested: Time in the market before withdrawals.

You control the first and third levers directly. The second lever requires informed choices: default versus chosen investment option, growth versus defensive mix, and, where appropriate, SMSFs or ethical options. These areas are supported by related articles in this super and SMSF knowledge pack.

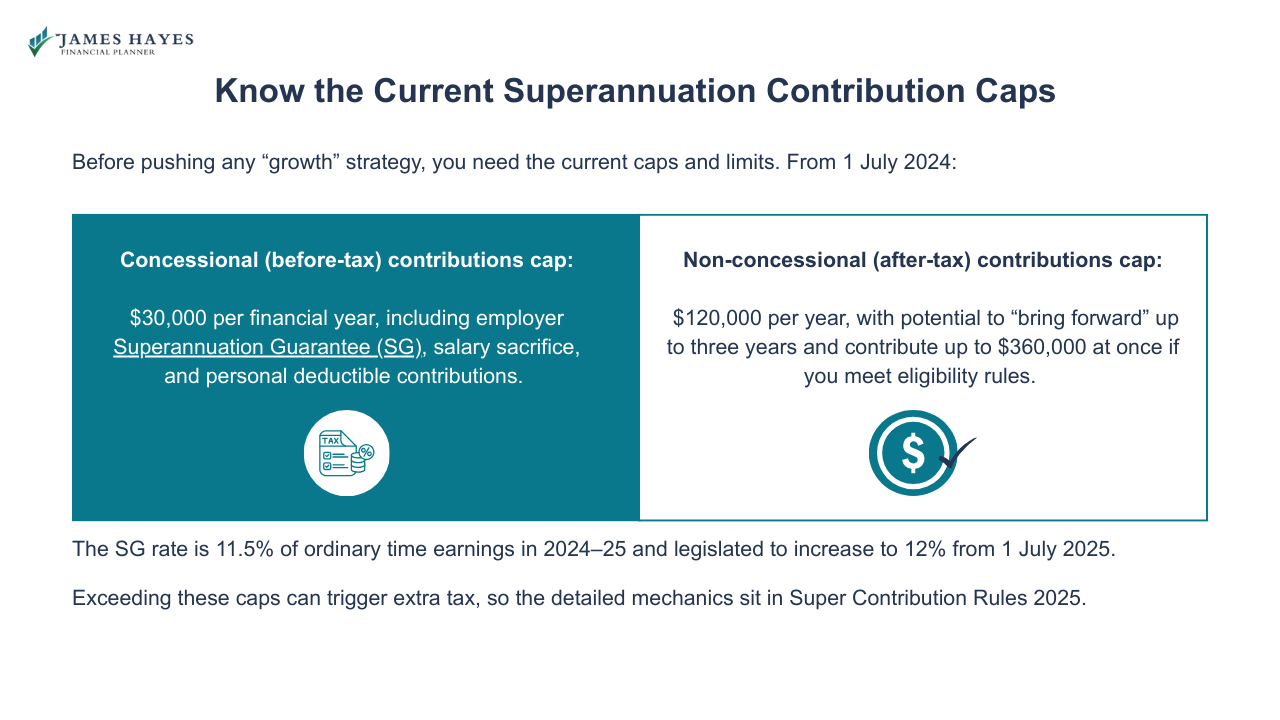

Know the Current Superannuation Contribution Caps

Before pushing any “growth” strategy, you need the current caps and limits. From 1 July 2024:

Concessional (before-tax) contributions cap: $30,000 per financial year, including employer Superannuation Guarantee (SG), salary sacrifice, and personal deductible contributions.

Non-concessional (after-tax) contributions cap: $120,000 per year, with potential to “bring forward” up to three years and contribute up to $360,000 at once if you meet eligibility rules.

The SG rate is 11.5% of ordinary time earnings in 2024–25 and legislated to increase to 12% from 1 July 2025.

Exceeding these caps can trigger extra tax, so the detailed mechanics sit in Super Contribution Rules 2025.

Superannuation Contribution Strategies While You Are Working

Most growth comes from a steady flow of contributions over many years. This section focuses on workers and business owners who are still accumulating.

Use Concessional Contributions Efficiently

For many 35–65 year olds, concessional contributions are the core growth tool because they are usually taxed at 15% inside super rather than at marginal rates, which can be 30% or higher from 1 July 2024.

Two standard approaches are:

Salary sacrifice: Asking your employer to direct part of your pre-tax salary to super, within your $30,000 concessional cap.

Personal deductible contributions: Making a lump-sum contribution from your bank account, then lodging a notice of intent to claim a deduction.

For example, a 45-year-old earning $140,000 in 2024–25 could:

Receive around $16,100 in SG at 11.5%.

Salary-sacrifice an extra $10,000, staying inside the $30,000 cap.

Have $26,100 going into super at a 15% contributions tax rate, instead of paying their marginal income tax rate on that $10,000.

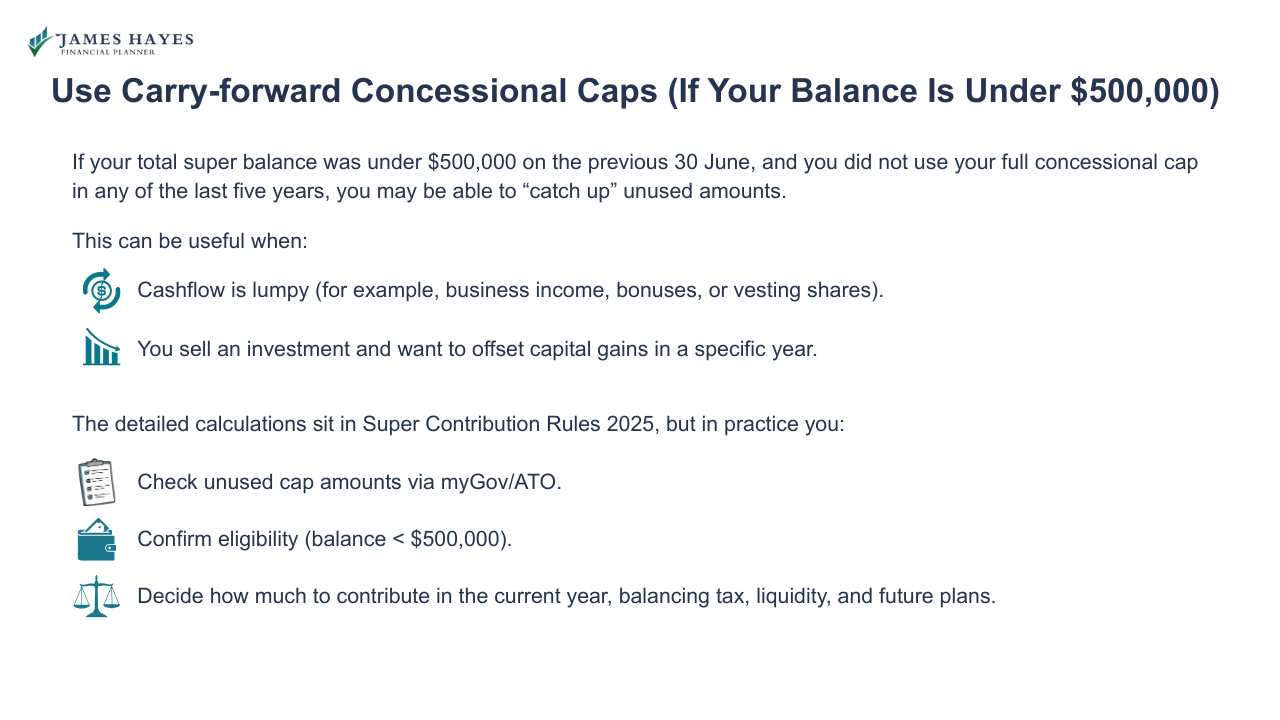

Use Carry-forward Concessional Caps (If Your Balance Is Under $500,000)

If your total super balance was under $500,000 on the previous 30 June, and you did not use your full concessional cap in any of the last five years, you may be able to “catch up” unused amounts.

This can be useful when:

Cashflow is lumpy (for example, business income, bonuses, or vesting shares).

You sell an investment and want to offset capital gains in a specific year.

The detailed calculations sit in Super Contribution Rules 2025, but in practice you must:

Consider Non-concessional and Bring-forward Contributions

Non-concessional contributions use after-tax money. They do not give you an immediate tax deduction, but they move money into the lower tax environment of super, which is especially relevant if you expect high future investment income outside super.

Key rules as at 2024–25:

Standard cap: $120,000 per financial year.

Bring-forward rule: up to $360,000 at once by “using” up to three years of caps, if you are under 75 at 1 July of the year you trigger the rule.

Your available limit depends on your total super balance at the previous 30 June and reduces once you are above specific thresholds.

Bring-forward contributions often feature in:

Pre-retirement top-ups from savings or inheritances

Couples moving non-super money into super in a planned way

Strategies combined with downsizer contributions (explained later)

For the technical table of thresholds and bring-forward combinations, see Super Contribution Rules 2025 rather than repeating it here.

Want a simple way to check your caps, map your contributions, and avoid surprises at tax time? Download the 2026 Super Contributions & Tax Planner. It helps you line up SG, salary sacrifice, personal contributions, and bring-forward rules without guesswork.

Government and Spouse Support for Building Super Balances

For some households, especially in the 35–50 range or where one partner has lower income, government incentives and spouse strategies can accelerate growth without very high contributions.

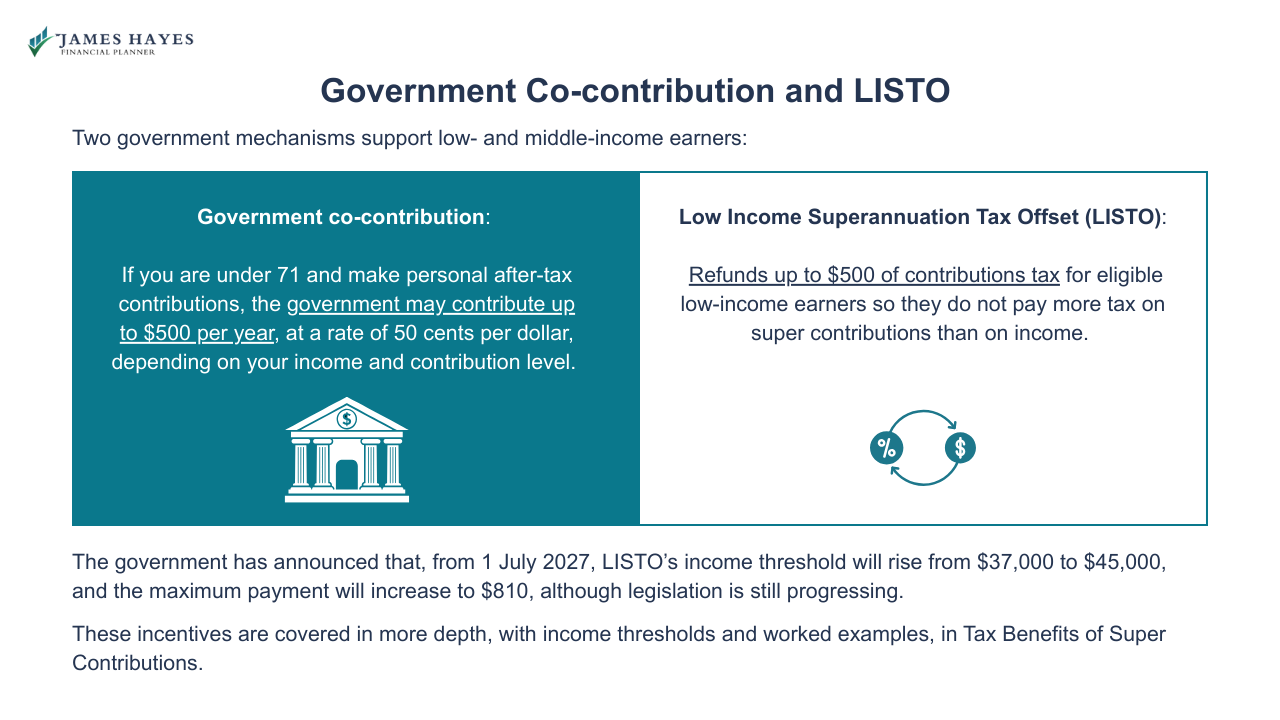

Government Co-contribution and LISTO

Two government mechanisms support low- and middle-income earners:

Government co-contribution: If you are under 71 and make personal after-tax contributions, the government may contribute up to $500 per year, at a rate of 50 cents per dollar, depending on your income and contribution level.

Low Income Superannuation Tax Offset (LISTO): Refunds up to $500 of contributions tax for eligible low-income earners so they do not pay more tax on super contributions than on income.

The government has announced that, from 1 July 2027, LISTO’s income threshold will rise from $37,000 to $45,000, and the maximum payment will increase to $810, although legislation is still progressing.

These incentives are covered in more depth, with income thresholds and worked examples, in Tax Benefits of Super Contributions.

Spouse Contributions and Contribution Splitting

Couples can use super rules to balance retirement savings, which is relevant for:

One partner who has taken time out for caring responsibilities

Households planning for potential Age Pension entitlements

Managing transfer balance caps in later retirement

Two common approaches are:

Spouse contributions: One partner pays a non-concessional contribution into the other’s account and may receive a tax offset, subject to income thresholds.

Contribution splitting: You ask your fund to allocate up to 85% of your concessional contributions for a year into your spouse’s account (usually the following year), within prescribed limits.

These techniques are particularly important in the Women & Super Gap Awareness article, which addresses the persistent gap in women’s super balances, and in Super and Divorce / Relationship Splits, which examines how super is treated on separation.

Free eBook: How to Grow Your Super Balance

〰️

Free eBook: How to Grow Your Super Balance 〰️

Superannuation Investment Strategy

Contribution strategies only create potential. Investment decisions determine whether that potential becomes actual growth.

Most Australians are in MySuper default options unless they deliberately choose another option. MySuper options must be diversified, but growth and risk levels still vary across funds.

Choosing an Appropriate Risk Level

A simple way to think about investment risk is by timeframe:

If you are 35–50, you generally have 15–30 years until retirement. A higher allocation to growth assets (Australian and global shares, property, and infrastructure) is often appropriate, assuming you can tolerate fluctuations.

If you are 55–65, you still need growth, because retirement may last 25 years or longer, but sequence-of-returns risk matters more. Many pre-retirees tilt to slightly more balanced or “growth plus defence” portfolios.

Lifecycle or “age-based” options gradually shift from growth to defensive assets as you approach retirement. Each fund implements this differently, so asset mix, fees, and glide-path need to be checked individually.

Ethical and sustainable options apply additional filters to the investment universe. They are discussed in Ethical & Sustainable Super Funds, which assesses screening methods, greenwashing risks, and how these options compare with standard growth or balanced choices.

Managing Fees, Insurance, and Leakage

Fees and insurance premiums can erode returns, especially if you have multiple funds.

Key checks include:

Investment and administration fees: Small percentage differences compound materially over 20–30 years.

Insurance inside super: Life, TPD, and income protection cover should match your needs; unnecessary or duplicated policies reduce growth.

Adviser service fees: Ongoing advice fees should align with the level of service and review you actually receive.

The article Rolling Over Super Funds looks more closely at consolidation, insurance retention, and avoiding unintended loss of cover when closing older funds.

Thinking about your contribution strategy? Take a look at the 2026 Super Contributions & Tax Planner to quantify what’s possible this year — including caps, catch-up rules, and tax effects.

Structural Moves That Grow Your Super Balance

In addition to regular contributions and investment choices, several structural moves can add scale to your super.

Consolidate Scattered Accounts

Job changes often create multiple small balances. Consolidating into a single, well-chosen fund can:

Reduce duplicate fees and insurance

Make it easier to manage investment choices

Simplify retirement planning and estate nominations

Before rolling over, review:

Insurance cover that might be lost

Defined benefit or legacy features

Exit and entry fees, if any

These issues are covered step-by-step in Rolling Over Super Funds.

Use Downsizer Contributions (55+)

If you are 55 or older and sell your home (meeting main residence and other eligibility criteria), you may be able to contribute up to $300,000 per person to super as a downsizer contribution, regardless of your work status or standard contribution caps. For couples, this can mean up to $600,000 combined.

Downsizer contributions:

Do not count towards non-concessional caps.

Still count towards your total super balance and transfer balance cap calculations in later years.

This tool is usually reviewed alongside estate planning and cashflow needs. It also links to Superannuation Death Benefits, because large late-stage contributions affect death benefit tax outcomes.

Super Strategies by Life Stage

The principles are consistent, but the emphasis changes with age and circumstances.

Focus Areas If You Are 35–50

At this stage, time is your main asset. A 40-year-old who adds an extra $5,000 per year to super for 20 years at a 6% net return finishes with roughly $184,000 more than if they only received employer contributions.

Practical focus points:

Target a contribution rate (SG plus salary sacrifice and personal deductible) that gets close to your concessional cap, where cashflow allows.

Choose an investment option with an appropriate growth allocation and review every 2–3 years.

Consolidate multiple funds to ensure insurance needs are covered.

Build a habit of annual reviews, aligned to the 30 June year-end.

If you are self-employed, there is no compulsory SG on your own drawings. The dedicated article Super for the Self-Employed covers contribution options, deductions, and cashflow planning for business owners and contractors.

Focus Areas If You Are 55–65

For pre-retirees and those at early retirement ages, the main questions are:

How much income do you want, after tax, in retirement?

How much of that will come from super versus non-super assets and, where relevant, the Age Pension?

What balance do you need at retirement to support that income?

Growth strategies often involve:

Maximising concessional contributions (including carry-forward) as you reduce non-deductible debt.

Planning non-concessional or bring-forward contributions from savings, investment sales, or inheritance.

Considering downsizer contributions if scaling down the family home.

Structuring investments for the shift into account-based pensions and, where appropriate, transition-to-retirement income streams (covered in Accessing Your Super Before & After Retirement).

For couples, this stage also links closely with Super and Divorce / Relationship Splits, Women & Super Gap Awareness, and Superannuation Death Benefits, because decisions now affect both living standards and estate outcomes.

Heading toward retirement? Stay ahead with your super balance strategy. Download the 2026 Super Contributions & Tax Planner and figure out a contribution plan that actually fits your income, tax bracket, and year-end deadlines.

Using SMSFs as Part of a Growth Strategy

A self-managed super fund (SMSF) is essentially a private super fund where members are also trustees. SMSFs can allow:

Direct ownership of certain assets, such as business real property.

More bespoke investment strategies, including term deposits, managed portfolios, and some alternative assets.

However:

Trustees carry legal responsibility for compliance with super and tax law.

Set-up, audit, and running costs must be proportionate to fund size.

Investment strategies must still satisfy diversification and sole purpose requirements.

For many households, an SMSF becomes efficient only once balances are large enough, governance discipline is strong, and there is a clear reason to move away from high-quality public offer funds.

SMSF topics are handled across four dedicated articles:

Self-Managed Super Funds (SMSFs) Explained (structure, suitability, and trade-offs)

Setting Up an SMSF (steps, roles, and documentation)

SMSF Investment Rules 2025 (what is allowed and what is prohibited)

SMSF Compliance & Administration (ongoing obligations and penalties)

This supporting article simply flags SMSFs as one of several growth pathways, rather than the default option.

Behavioural Habits That Support Super Growth

Technical rules matter, but consistent behaviour is what builds balances over decades.

Useful habits include:

Annual contribution check: Confirm total concessional and non-concessional contributions against caps before 30 June.

Investment and fee review: Confirm your option, fee levels, and performance relative to similar funds.

Life event triggers: Reassess super when changing jobs, buying or selling property, receiving an inheritance, or separating.

Documentation: Keep records of notices of intent, spouse contribution claims, and downsizer elections.

Many of these reviews overlap with planning to access your super, which is the focus of Accessing Your Super (Before & After Retirement).

Make things simpler — download the free 2026 Super Contributions & Tax Planner. It helps you track caps, plan salary sacrifice, and time contributions before the deadline, so you can stay on track each year.

How James Hayes Works with Clients to Grow Super

James Hayes is an ASIC-licensed financial planner, based in Caringbah, serving clients across the Sutherland Shire and Sydney CBD. His work on super focuses on:

Quantifying your required retirement income and target super balance.

Designing contribution plans that make efficient use of concessional, non-concessional, and catch-up rules.

Selecting or reviewing super funds and investment options, including ethical choices where appropriate.

Coordinating super with non-super investments, home ownership, and estate planning.

He is not aligned with banks or large institutions, and he does not assist with Centrelink Jobseeker claims, debt consolidation using super, or schemes that aim to release super before lawful conditions of release.

If you want tailored modelling rather than general strategies, you can book a free 15-minute call with him.

FAQs

-

There is no universal figure, but many households aim to move gradually toward using most of the $30,000 concessional cap, where cashflow allows. The appropriate rate depends on your age, existing super, debt, and planned retirement age. A financial planner can model the contribution level required to meet your income target.

-

For tax purposes, they are usually equivalent. Both count toward the same concessional cap and are taxed at 15% inside super, with possible additional tax for very high incomes. Salary sacrifice is automated via payroll, whereas personal deductible contributions are often used for one-off lump sums or end-of-year top-ups.

-

Non-concessional contributions are usually considered when you have surplus after-tax savings, expect higher long-term investment returns than bank deposits, and have already used concessional caps or prefer to keep taxable income lower. They can also be relevant after an inheritance, business sale, or when coordinating with downsizer contributions in later years.

-

Most people do not need frequent changes. A practical approach is to review your option annually and after significant life events, such as job changes, major debt changes, or approaching retirement within five to ten years. Changes should align with your risk tolerance, timeframe, and overall investment strategy, not short-term market movements.

-

Consolidation usually reduces duplicated fees and insurance, which supports growth, but it can be harmful if you lose valuable insurance, defined benefits, or low-fee legacy arrangements. Before consolidating, compare investment options, insurance, and costs for each fund, and confirm there are no penalties that outweigh the benefits of having a single account.

-

Downsizer contributions allow eligible people aged 55 or over to move up to $300,000 each from home sale proceeds into super, outside normal contribution caps. This increases the portion of wealth invested in the super environment, where earnings are taxed at concessional rates, and later may support tax-free retirement-phase pensions.

-

An SMSF is not automatically better or worse. It offers wider investment choice and control but comes with trustee responsibilities, higher fixed costs, and strict compliance obligations. For some households with sufficient balance, skills, and need for specific assets, SMSFs work well. Others achieve strong outcomes using high-quality public offer funds.

-

Advice is generally useful when you are earning higher income, have $150,000–$200,000 or more in super and investments, or are within 10–15 years of retirement. It is also relevant after major events, such as separation, business sale, inheritance, or relocation, when contribution, investment, and withdrawal decisions become more complex and interlinked.

Superannuation & SMSFs Knowledge Bundle

- What is Superannuation and How Does It Work?

- Super Contribution Rules 2025

- Tax Benefits of Super Contributions

- Accessing Your Super (Before & After Retirement)

- Superannuation Death Benefits

- Self-Managed Super Funds (SMSFs) Explained

- Setting Up an SMSF

- SMSF Investment Rules 2025

- SMSF Compliance & Administration

- Rolling Over Super Funds

- Ethical & Sustainable Super Funds

- Super for the Self-Employed

- Super and Divorce / Relationship Splits

- Women & Super Gap Awareness

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.