Super Contribution Rules 2025 & 2026

Summary

Super contribution rules for 2025–26 set how much you, your employer, and others can pay into super before extra tax applies. Key points are the $30,000 concessional cap, $120,000 non-concessional cap, age and work-test rules, total balance thresholds, and special options such as downsizer and government incentives available in 2025.

Table of Contents

- Introduction

- Overview of Contribution Types and Caps in 2024–25 and 2025–26

- Employer Contributions or Superannuation Guarantee (SG)

- Concessional (Before-tax) Super Contributions in 2025 and 2026

- Non-concessional (After-tax) Super Contributions

- Age, Work Status, and Who Can Contribute in 2025–26

- Special Contribution Types That Sit Alongside the Main Caps

- Contribution Rules for Self-employed People

- SMSFs and Contribution Rules

- Interaction with the Transfer Balance Cap from 1 July 2025

- Planning Around 30 June 2025 and 30 June 2026

- How James Hayes Can Help with Superannuation

- FAQs

- Superannuation & SMSFs Knowledge Bundle

Introduction

For wealth builders in their 30s and 40s, and pre-retirees or retirees in their 50s and 60s, super contribution rules determine how much you can add to your super at concessional tax rates each year.

This article explains the rules for:

The 2024–25 financial year (1 July 2024 to 30 June 2025)

The 2025–26 financial year (1 July 2025 to 30 June 2026), which we are currently in as of November 2025

It focuses on the rules, not the strategy. Strategy is handled in How to Grow Your Super Balance and Tax Benefits of Super Contributions, while What is Superannuation and How Does It Work? covers the underlying system.

James Hayes is an ASIC-licensed financial planner based in Caringbah who advises clients across the Sutherland Shire and Sydney CBD on super, retirement, and SMSFs. He does not assist with Centrelink Jobseeker support, debt consolidation using super, or schemes aimed at early super release outside the law.

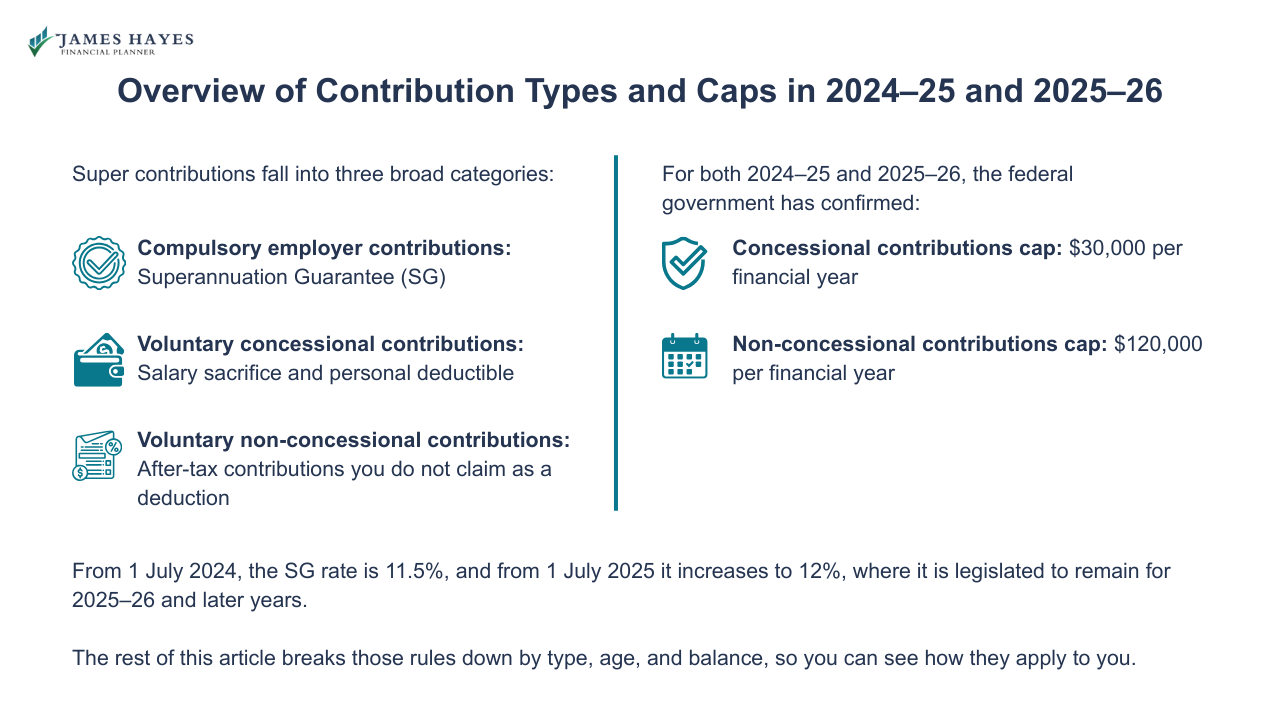

Overview of Contribution Types and Caps in 2024–25 and 2025–26

Super contributions fall into three broad categories:

Compulsory employer contributions: Superannuation Guarantee (SG)

Voluntary concessional contributions: Salary sacrifice and personal deductible

Voluntary non-concessional contributions: After-tax contributions you do not claim as a deduction

For both 2024–25 and 2025–26, the federal government has confirmed:

Concessional contributions cap: $30,000 per financial year

Non-concessional contributions cap: $120,000 per financial year

From 1 July 2024, the SG rate is 11.5%, and from 1 July 2025 it increases to 12%, where it is legislated to remain for 2025–26 and later years.

The rest of this article breaks those rules down by type, age, and balance, so you can see how they apply to you.

Planning ahead for 30 June? The Super Contributions & Tax Planner gives you a clean structure to check caps, calculate totals, test frameworks, and get organised early.

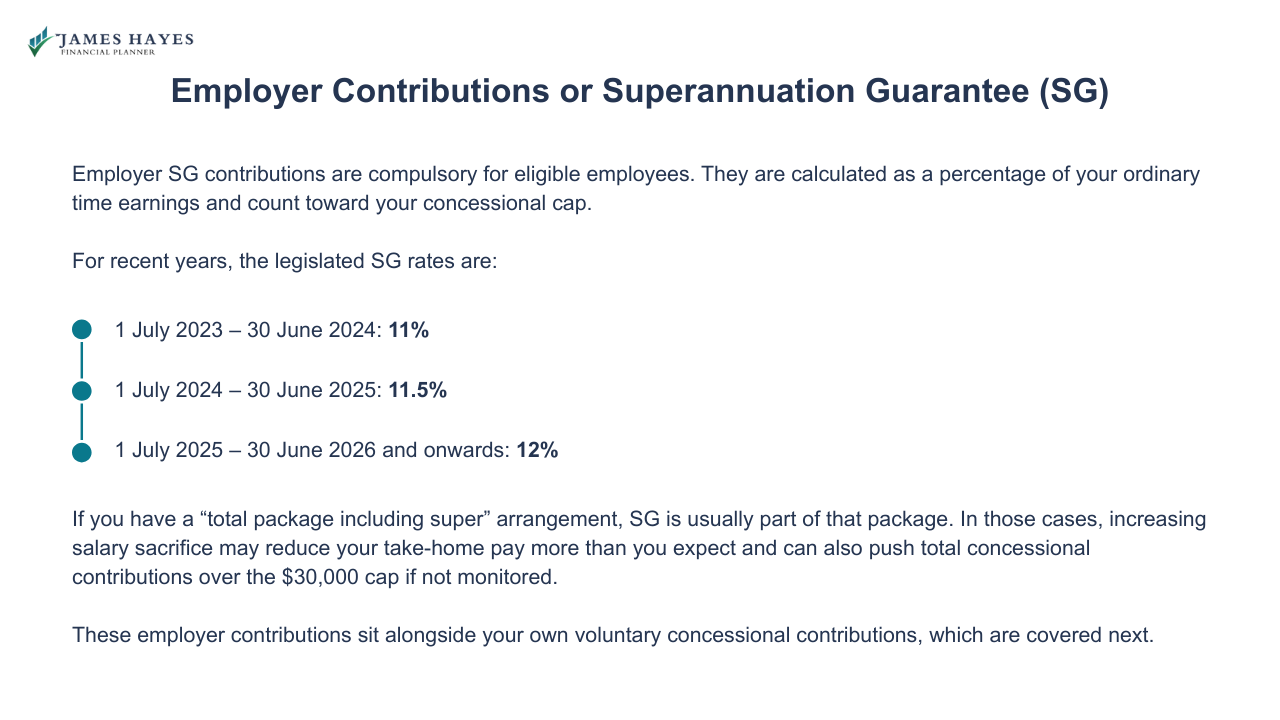

Employer Contributions or Superannuation Guarantee (SG)

Employer SG contributions are compulsory for eligible employees. They are calculated as a percentage of your ordinary time earnings and count toward your concessional cap.

For recent years, the legislated SG rates are:

1 July 2023 – 30 June 2024: 11%

1 July 2024 – 30 June 2025: 11.5%

1 July 2025 – 30 June 2026 and onwards: 12%

If you have a “total package including super” arrangement, SG is usually part of that package. In those cases, increasing salary sacrifice may reduce your take-home pay more than you expect and can also push total concessional contributions over the $30,000 cap if not monitored.

These employer contributions sit alongside your own voluntary concessional contributions, which are covered next.

Concessional (Before-tax) Super Contributions in 2025 and 2026

Concessional contributions are taxed at 15% inside your fund, rather than at your marginal income tax rate. They include:

Compulsory employer SG contributions

Reportable employer contributions (salary sacrifice)

Personal contributions you claim as an income-tax deduction

For 2024–25 and 2025–26, the general concessional cap is $30,000 per person, per financial year, across all funds.

If your income plus concessional contributions exceed $250,000 in a year, you may pay an additional 15% Division 293 tax on some or all concessional contributions, taking their tax rate to 30%.

The Tax Benefits of Super Contributions article uses worked examples to compare after-tax positions with and without concessional contributions for different income levels.

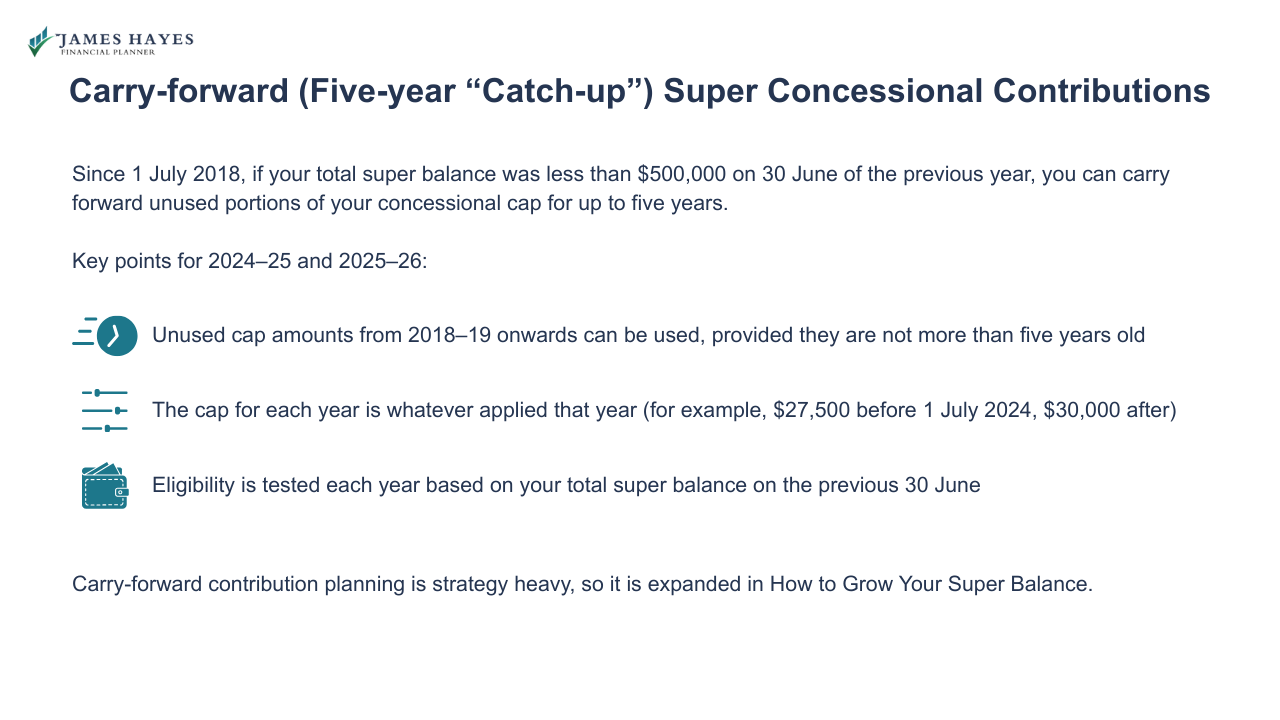

Carry-forward (Five-year “Catch-up”) Super Concessional Contributions

Since 1 July 2018, if your total super balance was less than $500,000 on 30 June of the previous year, you can carry forward unused portions of your concessional cap for up to five years.

Key points for 2024–25 and 2025–26:

Unused cap amounts from 2018–19 onwards can be used, provided they are not more than five years old

The cap for each year is whatever applied that year (for example, $27,500 before 1 July 2024, $30,000 after)

Eligibility is tested each year based on your total super balance on the previous 30 June

Carry-forward contribution planning is strategy heavy, so it is expanded in How to Grow Your Super Balance.

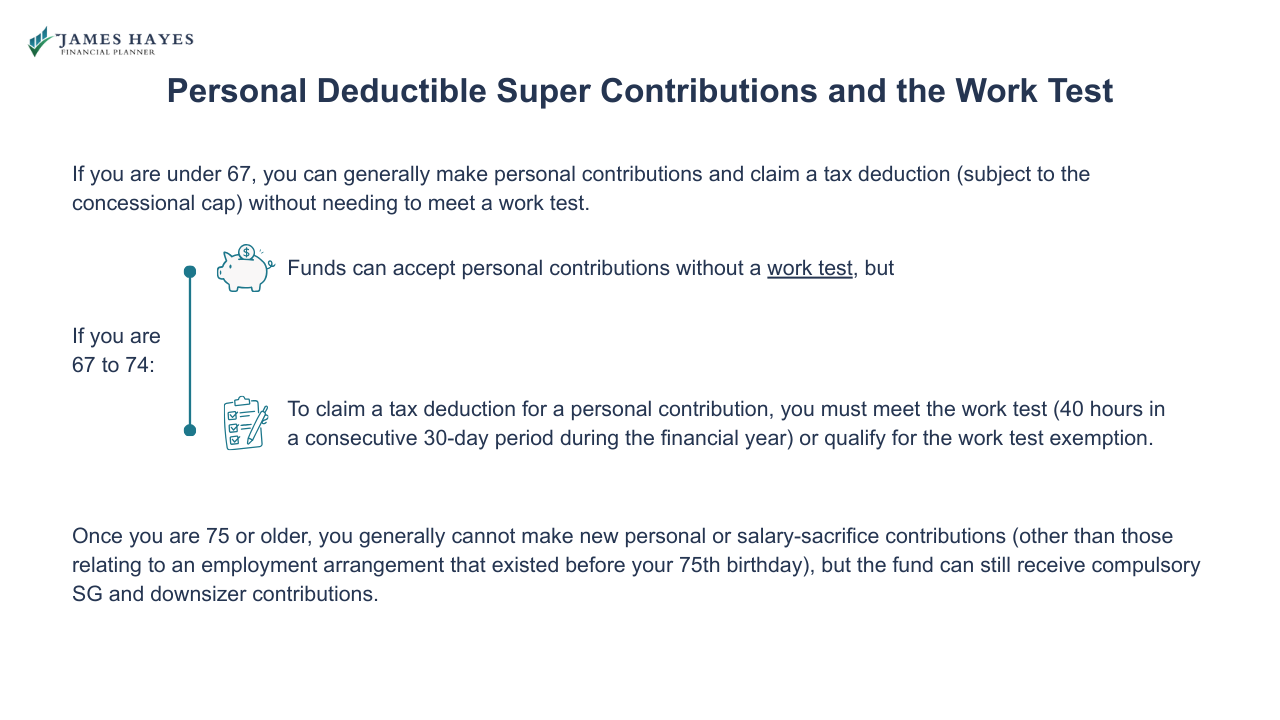

Personal Deductible Super Contributions and the Work Test

If you are under 67, you can generally make personal contributions and claim a tax deduction (subject to the concessional cap) without needing to meet a work test.

If you are 67 to 74:

Funds can accept personal contributions without a work test, but

To claim a tax deduction for a personal contribution, you must meet the work test (40 hours in a consecutive 30-day period during the financial year) or qualify for the work test exemption.

Once you are 75 or older, you generally cannot make new personal or salary-sacrifice contributions (other than those relating to an employment arrangement that existed before your 75th birthday), but the fund can still receive compulsory SG and downsizer contributions.

Want help checking how much concessional cap you still have left? The Super Contributions & Tax Planner gives you a clean worksheet to map SG, salary sacrifice, and personal deductible contributions for FY26.

Non-concessional (After-tax) Super Contributions

Non-concessional contributions come from money that has already been taxed. They are not taxed on the way into super but are subject to annual caps and balance-based limits.

For both 2024–25 and 2025–26:

The Standard non-concessional cap is $120,000 per year.

If your total super balance on 30 June of the previous year is at or above the general transfer balance cap (TBC), your non-concessional cap is nil for that year.

The relevant general transfer balance caps are:

2023–24 and 2024–25: $1.9 million

2025–26: $2.0 million

If your total super balance is at or above the TBC on 30 June, you cannot make further non-concessional contributions the following year.

Bring-forward Super Rule

If you are under 75 at any time during the financial year and otherwise eligible, you may trigger the bring-forward rule by contributing more than the standard $120,000 cap.

For 2024–25 and 2025–26 the maximum bring-forward is:

Up to $360,000 (three years of $120,000), subject to your total super balance.

Up to $240,000 (two-year bring-forward) where your total super balance is within a middle range.

Standard $120,000 only, or nil, once your total super balance approaches the TBC.

Indicative 2024–25 thresholds (based on a 30 June 2024 total super balance) are:

< $1.66m – up to $360,000

$1.66m to < $1.78m – up to $240,000

$1.78m to < $1.9m – up to $120,000

≥ $1.9m – non-concessional cap is nil

For 2025–26 (based on a 30 June 2025 balance), the thresholds shift because the TBC and total super balance test increase to $2.0m. For example, if your total super balance is $1.88m or more but under $2.0m, you can contribute up to the standard $120,000, but you cannot trigger a bring-forward.

The precise threshold bands are numeric and change over time, so the ATO non-concessional cap guidance should always be checked at the time of advice.

Want a simple way to map out your concessional and non-concessional limits for 2025–26? Download the Super Contributions & Tax Planner to work out what you can contribute, how it affects tax, and where you have room before 30 June.

Free eBook: 2025-26 Super Contributions and Tax Planner (Instant Download)

〰️

Free eBook: 2025-26 Super Contributions and Tax Planner (Instant Download) 〰️

Age, Work Status, and Who Can Contribute in 2025–26

The law distinguishes between whether a fund can accept a contribution and whether you can claim a tax deduction.

For 2025–26:

Under 67: Funds can accept all standard contribution types (subject to caps). You can claim deductions for personal concessional contributions if you lodge a valid notice of intent.

67 to 74: Funds can still accept concessional and non-concessional contributions. However, you must meet the work test or work test exemption to claim a deduction for personal concessional contributions.

75 or older: Funds can receive compulsory employer SG and downsizer contributions. Other voluntary contributions are heavily restricted.

The detailed mechanics of the work test and exemption are procedural rather than strategic, so this post keeps them high level. Implementation is usually handled in the context of a specific retirement or tax plan.

Special Contribution Types That Sit Alongside the Main Caps

Some contribution types either do not count toward the standard caps or interact with them in particular ways. These can be especially relevant for pre-retirees and retirees in the 55–75 range.

Downsizer Contributions (55 and Over)

If you are 55 or older, and you or your spouse sell an eligible main residence held for at least ten years, you may be able to make a downsizer contribution of up to $300,000 per person (up to $600,000 per couple) directly into super.

Key points:

Downsizer contributions do not count toward concessional or non-concessional caps.

They can be made regardless of your total super balance, and there is no upper age limit.

They still count towards later total super balance calculations and the transfer balance cap.

Downsizer contributions are explained in more detail in How to Grow Your Super Balance, and their estate-planning impact is covered in Superannuation Death Benefits.

Government Co-contribution

If you are a lower or middle-income earner and make personal non-concessional contributions, you may be eligible for a government co-contribution of up to $500 in 2024–25 and 2025–26.

For 2024–25 the maximum $500 applies if:

Your income is $45,400 or less, and

You make an eligible personal contribution of at least $1,000

The co-contribution tapers to zero once income reaches $60,400. Thresholds for 2025–26 are expected to be indexed. The ATO publishes the confirmed figures each year.

Low-income Super Tax Offset (LISTO)

LISTO is designed so low-income earners do not pay more tax on concessional contributions than on their wages. It provides a refund of 15% of concessional contributions, capped at $500, for individuals with incomes up to $37,000 (with legislated increases from 1 July 2027 not yet in force).

The detailed income definitions and eligibility tests sit within Tax Benefits of Super Contributions.

Check whether you qualify for LISTO or the government co-contribution, with the Super Contributions & Tax Planner. It helps you line up your income and contribution pattern so you can compare it with the latest thresholds.

Spouse Contributions and Contribution Splitting

Two mechanisms exist to rebalance super between spouses:

Spouse contributions: One partner contributes to the other’s super using after-tax money. The contributing spouse may receive a tax offset of up to $540, subject to income tests.

Contribution splitting: One spouse asks the fund to allocate up to 85% of the previous year’s concessional contributions to the other spouse’s account, within legislated limits.

These rules are relevant to Women & Super Gap Awareness and Super and Divorce / Relationship Splits, which focus on uneven balances and separation.

Contribution Rules for Self-employed People

If you are self-employed or a contractor without SG from an employer, contribution rules are the same, but the responsibility to act is yours.

Typically, you:

Make personal concessional contributions and claim a deduction, subject to the $30,000 cap and work-test rules if you are 67–74.

Use non-concessional contributions or downsizer contributions when disposing of assets or receiving windfalls.

Decide how to balance contributions against business cashflow and non-super investments.

Because missed contribution years are hard to recover, this topic is expanded in Super for the Self-Employed, which looks at cashflow patterns in more detail.

SMSFs and Contribution Rules

Self-managed super funds (SMSFs) are regulated under the same contribution caps and age rules as large public offer funds. The differences lie in:

How contributions are recorded and allocated to member accounts.

The risk of non-arm’s-length income (NALI) if contributions are structured improperly.

The added focus on audit evidence and documentation.

Trustees must ensure contributions are:

Within caps

Made for a member who is eligible by age and work-test status

Supported by bank records, contribution statements, and notices of intent, where relevant

These implementation issues are handled in the SMSF content cluster:

This contributions article focuses on the rules themselves, rather than their SMSF-specific administration.

Interaction with the Transfer Balance Cap from 1 July 2025

From 1 July 2025, the general transfer balance cap increases from $1.9m to $2.0m.

This change affects contribution rules in two ways:

The total super balance test for non-concessional contributions and bring-forward eligibility increases to $2.0m, which means some individuals who were previously locked out may regain capacity to contribute after 30 June 2025.

Planning the timing of contributions relative to starting a retirement-phase pension becomes more intricate, especially for people near the cap.

The detailed impact on retirement income streams is covered in Accessing Your Super (Before & After Retirement), while tax-efficient death-benefit strategies are explored in Superannuation Death Benefits.

If you want the key FY26 contribution settings in one place – caps, main thresholds, and how they line up with your income – use the 2026 Super Contributions & Tax Planner. It gives you a clean worksheet to sketch your numbers before meeting with James.

Planning Around 30 June 2025 and 30 June 2026

Because caps, balance tests, and transfer balance caps are measured at specific dates (usually 30 June), practical planning for 2025 and 2026 often involves:

Checking your total super balance on 30 June each year through myGov/ATO.

Confirming total concessional contributions year-to-date across all funds.

Modelling whether to trigger bring-forward or carry-forward provisions in 2024–25 or 2025–26.

Coordinating contributions with asset sales, inheritances, or home downsizing.

The strategic side of this timing work is handled in How to Grow Your Super Balance and Tax Benefits of Super Contributions, which provide numerical examples.

How James Hayes Can Help with Superannuation

James provides advice on:

Super contributions and caps

Fund selection, investment options, and SMSFs

Retirement income planning and transitions to pension phase

Integration of super with Age Pension advice, inheritance planning, and other assets.

He does not provide advice on:

Centrelink Jobseeker claims

Debt consolidation schemes using super

Early release arrangements outside the standard conditions of release

If you need contribution rules applied to your own circumstances, you can book a free 15-minute call with him.

FAQs

-

For 2025–26, the concessional cap is $30,000, covering employer SG, salary sacrifice, and personal deductible contributions. The non-concessional cap is $120,000, provided your total super balance on 30 June 2025 is below $2.0 million. At or above $2.0 million, your non-concessional cap is nil for that year under ATO rules.

-

If you are under 75 and eligible, contributing more than $120,000 in non-concessional contributions in 2025–26 can automatically trigger a bring-forward period. You may access up to $360,000, depending on your total super balance on 30 June 2025. Once triggered, your bring-forward limit is fixed for three financial years.

-

From 1 July 2025, the work test mainly matters for claiming deductions on personal concessional contributions. If you are aged 67 to 74 and want to claim a deduction, you must meet the work test or exemption. Funds can still accept many contributions without the test, subject to age restrictions.

-

Exceeding a concessional cap usually means excess contributions are effectively a 15% tax offset for contributions already taxed in the fund, plus interest. Exceeding a non-concessional cap can trigger penalty tax or forced withdrawal of the excess and associated earnings, calculated under ATO rules.

-

Downsizer contributions sit outside the usual non-concessional caps, so they do not use up those limits. However, they still increase your total super balance and will count when assessing future non-concessional eligibility and transfer balance cap capacity. You must be at least 55 and meet all ATO downsizer criteria.

-

If you are self-employed, you can still make concessional and non-concessional contributions, subject to the same caps and age rules as employees. Concessional contributions are usually personal deductible contributions you claim at tax time. You are responsible for timing, documentation, and cashflow, because no employer pays SG on your behalf.

-

No. SMSF members are subject to the same concessional and non-concessional caps, age limits, work-test rules, and downsizer provisions as members of public offer funds. The differences lie in administration, audit, and non-arm’s-length income rules, which place more responsibility on SMSF trustees to track and document contributions accurately.

-

Advice tends to be valuable when you have combined super and investments above roughly $150,000–$200,000, are within 10–15 years of retirement, or are considering large non-concessional, downsizer, or catch-up concessional contributions. It is also important after major events, such as separation, inheritance, business sale, or planned home downsizing.

Superannuation & SMSFs Knowledge Bundle

- What is Superannuation and How Does It Work?

- How to Grow Your Super Balance

- Tax Benefits of Super Contributions

- Accessing Your Super (Before & After Retirement)

- Superannuation Death Benefits

- Self-Managed Super Funds (SMSFs) Explained

- Setting Up an SMSF

- SMSF Investment Rules 2025

- SMSF Compliance & Administration

- Rolling Over Super Funds

- Ethical & Sustainable Super Funds

- Super for the Self-Employed

- Super and Divorce / Relationship Splits

- Women & Super Gap Awareness

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.