Self-Managed Super Funds (SMSFs) Explained

Summary

A self-managed super fund (SMSF) is a private super fund with up to six members who are also trustees, responsible for all investment and compliance decisions. SMSFs use the same tax and contribution rules as other super funds but involve higher responsibilities, specific costs, and suitability checks before they make sense.

Table of Contents

- Introduction

- What Is a Self-Managed Super Fund?

- How an SMSF Is Structured in Practice

- How SMSFs Are Regulated and Taxed

- SMSF Trustee Duties and Legal Responsibilities

- Investment Flexibility and Restrictions in SMSFs

- SMSF Costs and Time Commitment

- When an SMSF May Be Appropriate

- When an SMSF May Not Be Appropriate

- SMSFs Across Life Stages

- SMSFs, Estate Planning, and Death Benefits

- How SMSFs Compare with Industry and Retail Super Funds

- How James Hayes Works with SMSFs

- FAQs

- Superannuation & SMSFs Knowledge Bundle

Introduction

For many wealth builders in their 30s and 40s, and pre-retirees or retirees in their 50s and 60s, SMSFs are presented as a way to “take control” of super. In practice, they are a specialist structure with specific legal responsibilities, running costs, and regulatory oversight.

This article explains, in the 2025–26 environment:

What an SMSF is and how it is structured

How SMSFs are regulated and taxed

Trustee duties, risks, and penalties

SMSF costs and time commitment

When an SMSF can be appropriate, and when it usually is not

It connects with:

What is Superannuation and How Does It Work? (system fundamentals)

How to Grow Your Super Balance (contribution and investment strategy)

Super Contribution Rules 2025 and Tax Benefits of Super Contributions (tax and caps)

Accessing Your Super (Before & After Retirement) (pensions and withdrawals)

Superannuation Death Benefits and Wills, Executors & Probate (succession and inheritance)

SMSF Investment Rules 2025, SMSF Compliance & Administration, and Setting Up an SMSF (detailed implementation)

James Hayes is an ASIC-licensed financial planner based in Caringbah, advising wealth builders, pre-retirees, and retirees across the Sutherland Shire and Greater Sydney on super, retirement, and SMSFs. He does not assist with Centrelink Jobseeker support, debt consolidation using super, or early-access schemes.

What Is a Self-Managed Super Fund?

An SMSF is a trust created for the sole purpose of providing retirement benefits to its members, or to their dependants if a member dies before retirement.

Key structural points:

An SMSF can have no more than six members.

Every member must be either an individual trustee or a director of a corporate trustee.

The fund is regulated by the Australian Taxation Office (ATO), not APRA.

Managing an SMSF is a major commitment requiring time, knowledge, and skill. Trustees are personally responsible for complying with super and tax laws.

Contributions, benefit payments, tax rates, and conditions of release are broadly the same as for other complying super funds. The differences are governance, control, and accountability, not special tax concessions.

The separate post Setting Up an SMSF walks through the steps.

Unsure whether an SMSF fits your situation? Download the SMSF Ready Assessment & Setup Roadmap — it gives you a quick check on whether the structure is suitable for your needs.

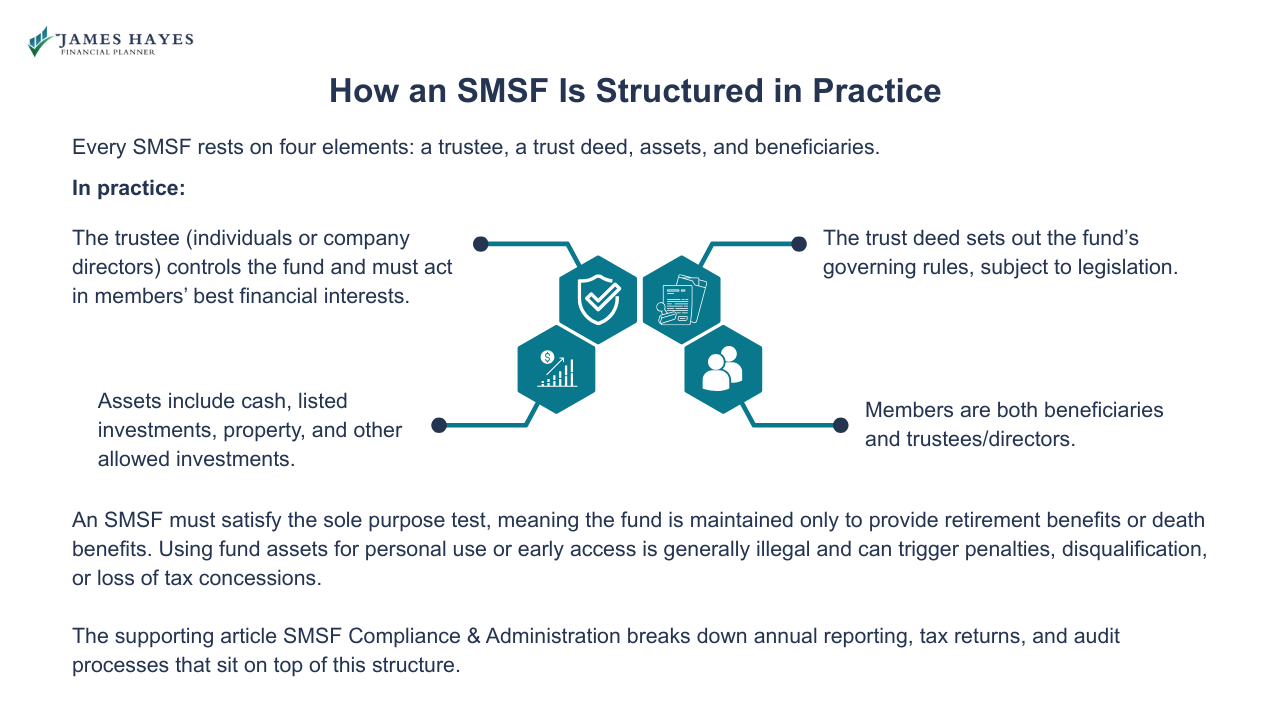

How an SMSF Is Structured in Practice

Every SMSF rests on four elements: a trustee, a trust deed, assets, and beneficiaries.

In practice:

The trustee (individuals or company directors) controls the fund and must act in members’ best financial interests.

The trust deed sets out the fund’s governing rules, subject to legislation.

Assets include cash, listed investments, property, and other allowed investments.

Members are both beneficiaries and trustees/directors.

An SMSF must satisfy the sole purpose test, meaning the fund is maintained only to provide retirement benefits or death benefits. Using fund assets for personal use or early access is generally illegal and can trigger penalties, disqualification, or loss of tax concessions.

The supporting article SMSF Compliance & Administration breaks down annual reporting, tax returns, and audit processes that sit on top of this structure.

How SMSFs Are Regulated and Taxed

SMSFs are governed primarily by the Superannuation Industry (Supervision) Act 1993, related regulations, and income tax law. The ATO:

Registers SMSFs and issues Australian business numbers and TFNs.

Monitors annual returns, contravention reports, and auditor compliance.

Can apply administrative penalties, direct rectification, disqualify trustees, or make a fund non-complying for serious breaches.

From a tax perspective, a complying SMSF is treated like other taxed super funds:

Up to 15% tax on most assessable income in accumulation phase, with effective 10% on long-term capital gains due to the one-third CGT discount.

0% tax on earnings from assets supporting retirement-phase income streams within the transfer balance cap (rising to $2.0 million on 1 July 2025).

Member contributions and withdrawals are taxed under the same contribution rules and access rules that apply to other funds.

The detail of contribution caps, Division 296 for large balances, and benefit taxation is covered carefully in Super Contribution Rules 2025, Tax Benefits of Super Contributions, and Accessing Your Super (Before & After Retirement).

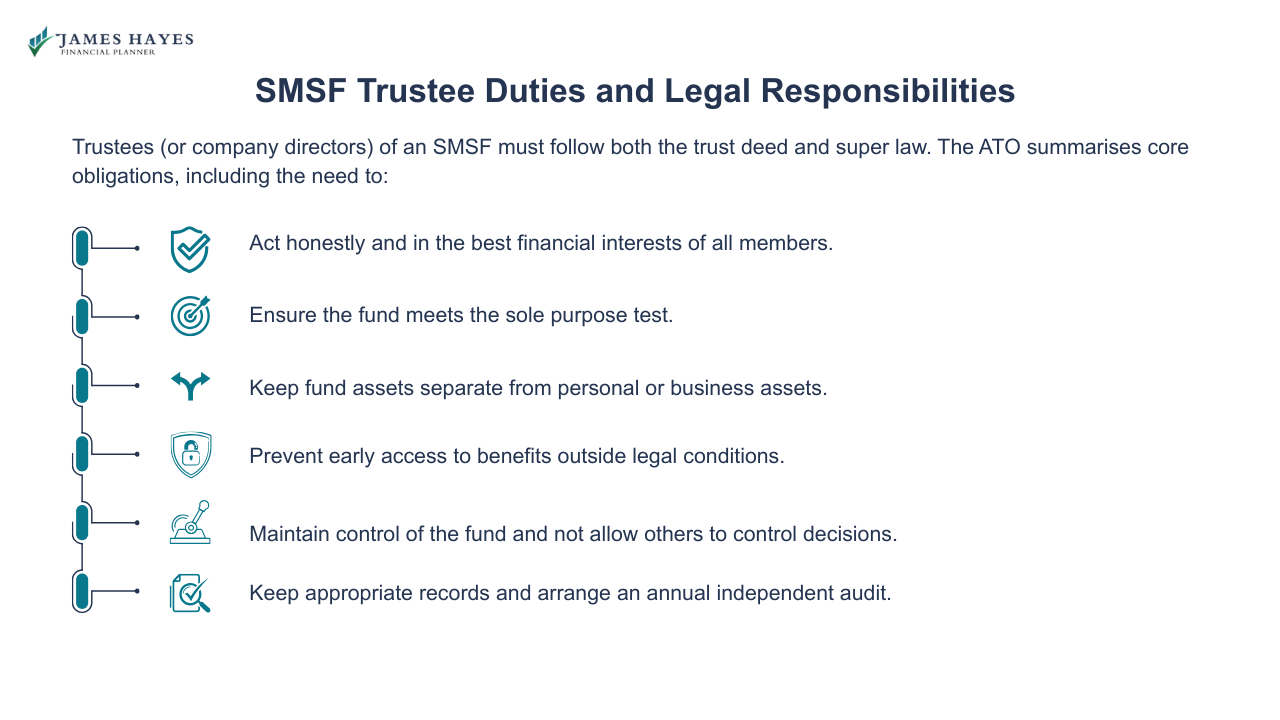

SMSF Trustee Duties and Legal Responsibilities

Trustees (or company directors) of an SMSF must follow both the trust deed and super law. The ATO summarises core obligations, including the need to:

Act honestly and in the best financial interests of all members.

Ensure the fund meets the sole purpose test.

Keep fund assets separate from personal or business assets.

Prevent early access to benefits outside legal conditions.

Maintain control of the fund and not allow others to control decisions.

Keep appropriate records and arrange an annual independent audit.

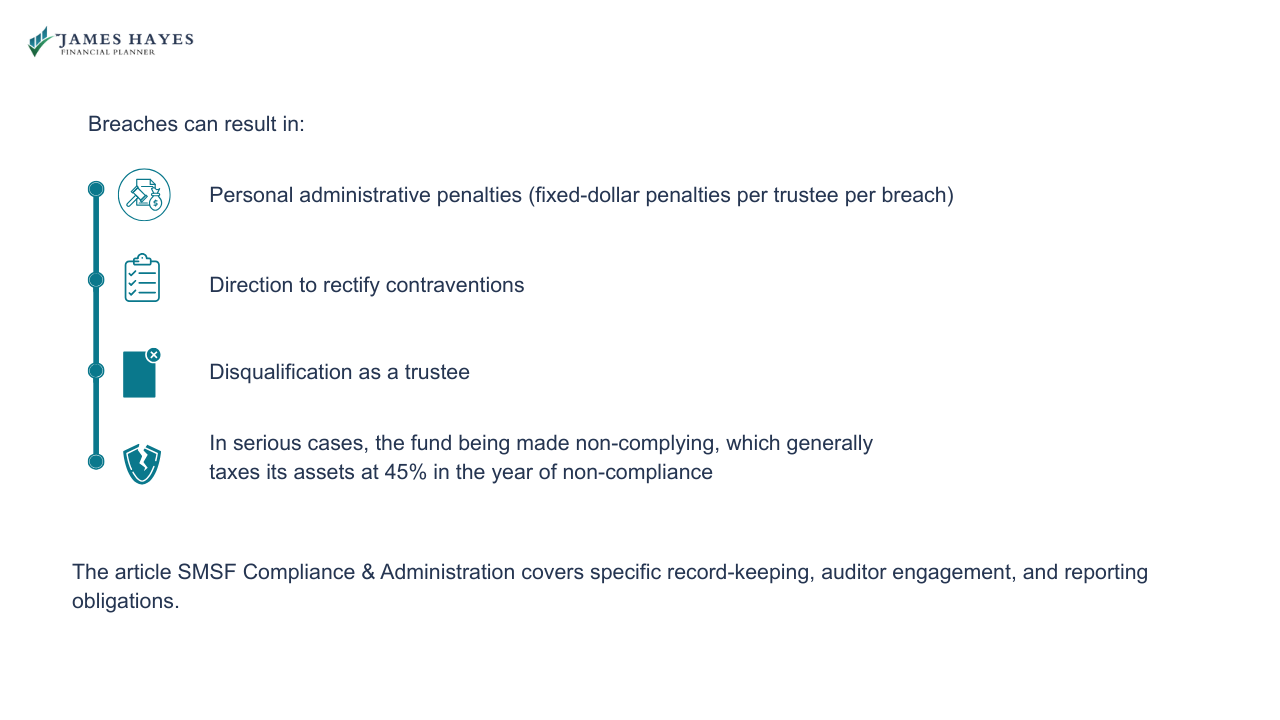

Breaches can result in:

Personal administrative penalties (fixed-dollar penalties per trustee per breach)

Direction to rectify contraventions

Disqualification as a trustee

In serious cases, the fund being made non-complying, which generally taxes its assets at 45% in the year of non-compliance

The article SMSF Compliance & Administration covers specific record-keeping, auditor engagement, and reporting obligations.

Investment Flexibility and Restrictions in SMSFs

One reason SMSFs attract interest is investment flexibility. Subject to law and the trust deed, an SMSF can invest in:

Cash and term deposits

Listed shares, exchange-traded funds, and managed funds

Some forms of fixed interest

Direct property, including certain business real property

Other assets that meet the investment strategy and legal tests

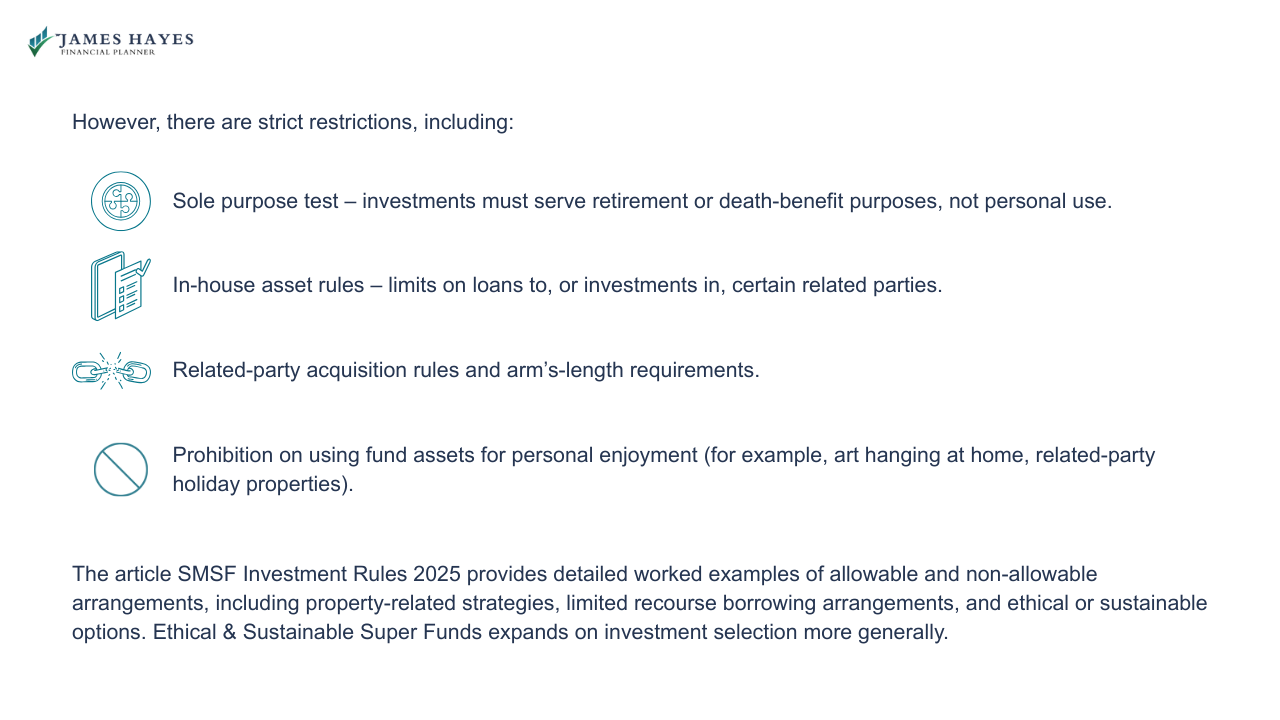

However, there are strict restrictions, including:

Sole purpose test – investments must serve retirement or death-benefit purposes, not personal use.

In-house asset rules – limits on loans to, or investments in, certain related parties.

Related-party acquisition rules and arm’s-length requirements.

Prohibition on using fund assets for personal enjoyment (for example, art hanging at home, related-party holiday properties).

The article SMSF Investment Rules 2025 provides detailed worked examples of allowable and non-allowable arrangements, including property-related strategies, limited recourse borrowing arrangements, and ethical or sustainable options. Ethical & Sustainable Super Funds expands on investment selection more generally.

Free eBook: SMSF Ready Assessment and Setup Roadmap (Instant Download)

〰️

Free eBook: SMSF Ready Assessment and Setup Roadmap (Instant Download) 〰️

SMSF Costs and Time Commitment

Even with professional support, SMSFs involve fixed and variable costs that must be weighed against balance size and benefits.

Recent data and analysis indicate that:

The ATO’s March 2025 quarter data suggests a median administration and operating expense around $4,628, and a median total expense (including investment-related costs) around $9,297 per fund, based on returns to March 2025.

Trustees spend more than eight hours per month on average managing an SMSF, or over 100 hours a year, across investment research, record-keeping, and compliance tasks.

Typical ongoing cost categories include:

Accounting and tax agent fees for annual financial statements and SMSF annual returns

Annual independent audit fees

ATO supervisory levy

Investment platform, brokerage, and, often, advice fees

Because many SMSF costs are flat-dollar amounts, they consume a larger percentage of smaller balances. ASIC has historically warned that funds with balances below around $500,000 often have lower net returns after fees and tax than comparable retail or industry funds, although guidance now focuses more generally on cost-effectiveness rather than strict thresholds.

The article Setting Up an SMSF covers typical establishment costs and fee structures in more detail.

When an SMSF May Be Appropriate

Regulators do not prescribe strict eligibility thresholds, but both ASIC and the ATO emphasise that SMSFs are not suitable for everyone.

In practice, SMSFs tend to be more suitable when several of the following apply:

Balance size is sufficient that fixed costs are reasonable as a percentage of assets (for example, a combined balance approaching or exceeding mid-six figures).

Members are willing and able to spend time on investment decisions, record-keeping, and regulatory updates.

There is a specific investment objective not easily achieved in standard funds (for example, owning business real property used by a family business, more tailored asset allocation, or integrated family estate planning).

There is a need for greater control over succession, pension design, or specific insurance and estate strategies, often in conjunction with Superannuation Death Benefits.

For 35–50 year olds, SMSFs can be relevant for business owners, higher-balance professionals, or families wanting coordinated investment and estate strategies. For 55–65 year olds, SMSFs are often evaluated as part of a transition-to-retirement or retirement-phase restructure, covered in Accessing Your Super (Before & After Retirement).

Not sure whether an SMSF is right for you? Take a quick test with the SMSF Ready Assessment & Setup Roadmap — a kit designed to help you understand whether you’re realistically SMSF-ready.

When an SMSF May Not Be Appropriate

Recent ASIC reviews and ATO warnings have highlighted material risks where SMSFs are established without clear suitability.

An SMSF is often not appropriate where:

Combined member balances are modest and the percentage impact of fixed costs is high.

Members have limited time or interest in investment and compliance tasks.

Financial literacy is low, or members are uncomfortable interpreting legal and tax rules.

Objectives are relatively simple (for example, broad market exposure, limited estate complexity), which can be achieved efficiently in well-run APRA-regulated funds.

The main driver is a proposal to access super early, buy high-risk or related-party investments, or consolidate debts.

The ATO has specifically warned against illegal SMSF schemes that promote early access to super for personal expenses, property deposits, or debt repayment. James does not assist with setting up SMSFs for debt consolidation or early-release purposes, consistent with this guidance.

The article Super for the Self-Employed looks at situations where SMSFs may or may not suit business owners and contractors compared with strong industry funds.

If any of the above red flags sound familiar, download the SMSF Ready Assessment & Setup Roadmap — it highlights the gaps that usually need fixing before an SMSF even makes sense to consider.

SMSFs Across Life Stages

SMSF suitability is not only about balance size. Life stage matters.

For 35–50 year olds, SMSFs are most often considered when:

There is a growing super balance alongside business or property plans, such as owning premises through super.

Couples want deliberate control over investment style, ethical tilts, or concentrated strategies not available in pooled funds.

There is early thinking about estate planning, blended families, or intergenerational wealth (see Women & Super Gap Awareness).

For 55–65 year olds, the questions usually shift to:

Coordinating account-based pensions, transition-to-retirement income streams, and lump sums.

Managing sequence-of-returns risk and cashflow in retirement, discussed in How to Grow Your Super Balance.

Structuring death-benefit nominations, reversionary pensions, and SMSF succession with the help of Superannuation Death Benefits and estate planning content.

In both age groups, the core question remains whether an SMSF adds net value once costs, time, and risk are fully accounted for.

SMSFs, Estate Planning, and Death Benefits

Because members are also trustees, SMSFs play a central role in estate planning and inheritance.

Important features include:

Trustees control how binding death-benefit nominations, reversionary pensions, and the deed interact when a member dies.

SMSFs can provide flexible income-stream or lump-sum options for spouses and dependants, subject to super and tax law.

Control of the trustee company or individual trustee roles after death or incapacity is critical, particularly in blended families.

The tax-treatment of superannuation death benefits is the same whether the fund is an SMSF or a large fund. The supporting article Superannuation Death Benefits explains:

Who is treated as a tax dependant

How adult children are taxed on taxable components

How recontribution and pension strategies can manage future death-benefit tax

How SMSFs Compare with Industry and Retail Super Funds

The ATO provides comparison guidance between SMSFs and other funds. At a high level:

Responsibility: SMSF members are directly responsible for everything. In industry and retail funds, a professional trustee group is responsible.

Control: SMSFs can tailor investment strategy, insurance, and estate features more precisely, within the law.

Costs: SMSFs have largely flat-dollar administration, audit, and advice fees. Industry funds often use percentage-based fees.

Regulation: SMSFs are regulated by the ATO. APRA regulates most large funds.

Complaints and compensation: SMSFs have limited access to statutory compensation schemes compared with APRA-regulated funds.

The article Rolling Over Super Funds deals with the mechanics and consequences of moving from APRA-regulated funds to SMSFs or vice versa.

Trying to compare SMSFs with your current fund? The SMSF Ready Assessment & Setup Roadmap walks you through a setup sequence so you can compare that commitment with staying in your current fund.

How James Hayes Works with SMSFs

Regulators have highlighted concerns where SMSFs were recommended without proper analysis of costs, risks, or suitability. ASIC’s 2025 Review of SMSF Establishment Advice found that 62% of advice files failed to demonstrate compliance with the best-interests duty, with 27% raising serious client-detriment concerns.

Against that backdrop, James works with clients in the Sutherland Shire and Sydney CBD to:

Assess whether an SMSF is appropriate compared with existing industry or retail funds.

Model SMSF outcomes alongside other strategies (see How to Grow Your Super Balance).

Integrate contributions, pensions, and investment decisions (see Super Contribution Rules 2025 and Tax Benefits of Super Contributions)

Coordinate SMSF structures with estate planning (see Superannuation Death Benefits)

He does not promote SMSFs as a default solution, nor as a vehicle for early access, debt consolidation, or high-risk schemes. If an SMSF does not appear cost-effective and suitable, he will usually recommend alternative structures.

If you want tailored advice on whether an SMSF is appropriate, you can request a 15-minute introductory call with James Hayes.

FAQs

-

An SMSF is a private super fund with up to six members who are also trustees or company directors. They control all investment and compliance decisions and are personally responsible for meeting super and tax laws. Industry and retail funds are run by professional trustees, with members as customers rather than controllers.

-

There is no legislated minimum balance. However, ATO data shows median annual SMSF expenses in the thousands of dollars, and ASIC has previously warned that funds under roughly $500,000 often have lower net returns after fees and tax than large funds. Cost-effectiveness, not a single dollar figure, should drive the decision.

-

The Australian Taxation Office regulates SMSFs and approved SMSF auditors. It monitors annual returns, contravention reports, and registration data, and can impose administrative penalties, direct rectification, disqualify trustees, or make a fund non-complying in serious cases. APRA regulates most large industry, retail, and corporate super funds, not SMSFs.

-

No. SMSFs must meet the same conditions of release as other funds. Using an SMSF to access super for personal expenses, debt repayment, or property purchases before a legal condition of release is met is generally illegal. The ATO actively warns against such schemes and can apply significant penalties.

-

Not in principle. A complying SMSF is taxed under the same rules as other taxed super funds: up to 15% on most accumulation earnings, effective 10% on eligible capital gains, and 0% on earnings supporting retirement-phase income streams within the transfer balance cap. Advantages or disadvantages arise from investment, cost, and governance decisions.

-

You must run the fund for the sole purpose of providing retirement or death benefits, act in members’ best financial interests, keep assets separate, prevent early access, follow contribution and investment rules, maintain required records, and arrange annual audits and returns. All trustees share responsibility, even if one person does more work.

-

Often, yes, if the property qualifies as business real property and the acquisition, lease, and any borrowing arrangements meet SMSF investment rules, in-house asset limits, and arm’s-length requirements. The detail is technical and covered in “SMSF Investment Rules 2025”. Legal, tax, and lending advice is usually required before proceeding.

-

SMSFs sit alongside, not inside, your estate. On death, remaining benefits are paid as superannuation death benefits to dependants or your legal personal representative, under the fund deed and any nominations. Binding nominations, reversionary pensions, trustee control, and tax on death benefits must align with your wills and broader estate planning.

Superannuation & SMSFs Knowledge Bundle

- What is Superannuation and How Does It Work?

- How to Grow Your Super Balance

- Super Contribution Rules 2025

- Tax Benefits of Super Contributions

- Accessing Your Super (Before & After Retirement)

- Superannuation Death Benefits

- Setting Up an SMSF

- SMSF Investment Rules 2025

- SMSF Compliance & Administration

- Rolling Over Super Funds

- Ethical & Sustainable Super Funds

- Super for the Self-Employed

- Super and Divorce / Relationship Splits

- Women & Super Gap Awareness

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.