Tax Considerations for Beneficiaries in Australia

Summary

Australia does not levy inheritance tax, so beneficiaries are not taxed simply for receiving assets. Tax issues arise later in the form of income tax on rent, dividends, and interest after transfer, CGT when inherited assets are sold, and tax rules for superannuation death benefits and trust distributions.

Table of Contents

- Introduction

- Do Beneficiaries Pay Inheritance Tax in Australia?

- Estate Debts, Liabilities, and Administration Expenses

- Income Earned from Inherited Assets After Transfer

- Income Earned During Estate Administration

- Capital Gains Tax (CGT) and Inherited Assets

- Superannuation Death Benefits and Tax

- Trust Distributions and Beneficiary Tax Obligations

- Foreign Assets and Overseas Inheritances

- Recordkeeping and Reporting Requirements

- When to Seek Professional Advice

- Conclusion

- FAQs

- Inheritance & Estate Planning Knowledge Bundle

Introduction

Inheritances often involve property, listed investments, superannuation, and family trusts. The tax position depends on what you receive, how you receive it (estate vs non-estate), and when a later taxable event occurs (sale, income, distribution).

This article covers the main tax categories beneficiaries encounter in Australia and the specific legislative concepts that typically determine outcomes.

Do Beneficiaries Pay Inheritance Tax in Australia?

Australia does not have inheritance tax or estate tax in the way some countries do. Receiving cash or assets from a deceased estate is not a taxable event by itself.

Tax becomes relevant when:

the inherited asset produces assessable income after you become the owner, or

you sell, transfer, or otherwise dispose of a CGT asset you inherited.

Estate Debts, Liabilities, and Administration Expenses

Before beneficiaries receive estate assets, the executor (legal personal representative) pays estate liabilities and costs of administration. Beneficiaries generally do not pay estate debts from personal funds unless they have their own legal exposure (for example, as a borrower, guarantor, or joint debtor).

Typical estate outgoings include final tax liabilities, funeral costs, probate expenses, and professional fees. Some executor costs can also be relevant for CGT cost base calculations later.

Income Earned from Inherited Assets After Transfer

Once an asset is transferred to you, income it produces is generally assessed to you as the owner. For Australian residents, ordinary income derived from all sources is included in assessable income under Section 6-5 of the Income Tax Assessment Act 1997.

Rental Income on an Inherited Property

If you inherit a property and rent it out after it is transferred, rent is assessable income. You may also be entitled to deductions that meet the general deduction rules in Section 8-1 of the Income Tax Assessment Act 1997 (subject to the usual limits and substantiation). Keep records of the transfer date, tenancy start date, and deductible expenses.

Dividends on Inherited Shares and Managed Funds

Dividends received after the shares or units are transferred to you are assessable as ordinary income under Section 6-5 of the Income Tax Assessment Act 1997. Franking credits and dividend statements should be retained, as they affect the tax calculation.

Interest on Inherited Cash

Interest earned on inherited cash in a bank account or term deposit after it becomes yours is generally assessable under Section 6-5 of the Income Tax Assessment Act 1997. The cash itself is not taxed because it was inherited. The interest is taxed because it is income.

Income Earned During Estate Administration

Income generated while the estate is being administered is typically dealt with in the estate’s tax affairs, not the beneficiary’s, until beneficiaries become entitled to income or receive distributions. The ATO distinguishes the deceased person’s final return (up to date of death) from trust tax returns for the estate after death.

Where a beneficiary is presently entitled to trust income, different rules can apply (see trusts section below).

Capital Gains Tax (CGT) and Inherited Assets

CGT is the main long-term tax issue for beneficiaries who inherit property, shares, or other CGT assets.

As a starting point:

CGT does not usually arise merely because an asset passes on death, and

CGT is commonly triggered later when a disposal occurs (for example, a sale).

No CGT Event at the Time of Death?

Division 128 contains the specialist CGT rules for death. In general terms, capital gains or losses when a person dies are disregarded (subject to exceptions), which is why inheriting is not a taxable event at that point.

When you later sell an inherited CGT asset, the disposal is commonly a CGT event (for example, CGT event A1 under Section 104-10 of the Income Tax Assessment Act 1997).

Cost Base, Acquisition Timing, and Date-of-Death Values

The beneficiary or estate may inherit or reset the cost base depending on the asset type and circumstances. ATO guidance explains how to work out the cost base of inherited assets, and notes that certain costs of the legal personal representative can form part of the cost base.

Main Residence Exemption and the Two-Year Timeframe

If the inherited dwelling was the deceased’s main residence, exemptions may apply. One of the key legislative reference points is Section 118-195 of the Income Tax Assessment Act 1997, which is often discussed in practice as including a two-year sale timeframe in certain scenarios.

Because eligibility depends on facts (use of the property, who lived there, and timing), the executor’s file should include valuation and occupancy information.

CGT Discount Where Conditions Are Met

If you dispose of an inherited asset and the relevant holding period and eligibility rules are satisfied, the CGT discount rules in Subdivision 115-A may reduce a capital gain for individuals (subject to conditions).

Free eBook: Beneficiaries Tax Records Checklist

〰️

Free eBook: Beneficiaries Tax Records Checklist 〰️

Superannuation Death Benefits and Tax

Superannuation death benefits can be taxed very differently to estate assets because super sits outside the estate and is paid under fund rules and trustee decisions.

ATO guidance summarises the operational position for funds paying death benefits, including that lump sums paid to dependants are tax-free, and where beneficiaries are not dependants, the taxable component can be taxed at different rates depending on taxed and untaxed elements.

Death Benefits Dependant Definition

The definition is Section 302-195 of the Income Tax Assessment Act 1997, which sets out who is a death benefits dependant, including a spouse or former spouse, a child under 18, an interdependent person, or another dependant.

Tax for Non-Dependants Receiving a Lump Sum

If a person is not a death benefits dependant and receives a superannuation lump sum because of death, Section 302-145 of the Income Tax Assessment Act 1997 provides that the taxable component is assessable income, with different treatment for taxed and untaxed elements.

The ATO’s super death benefit guidance notes tax rates of 15% for the taxed element and 30% for the untaxed element in scenarios where not all beneficiaries are dependants.

When Is the Benefit Paid to the Estate?

If a super death benefit is paid to the legal personal representative (estate), taxation can depend on the status of the ultimate beneficiaries. The ATO guidance addresses the “paid to the estate” scenarios and the dependant versus non-dependant outcome.

Trust Distributions and Beneficiary Tax Obligations

Trust structures are common in Sydney family wealth planning, particularly where wills create testamentary trusts. The tax position hinges on whether you are presently entitled to income and how the trustee resolves distribution by year-end.

Division 6 of the Income Tax Assessment Act 1936 sets the trust assessment framework. Section 97 includes the rule that where a beneficiary is presently entitled (and not under legal disability), their assessable income includes their share of the trust’s net income.

Present Entitlement Drives Timing

ATO material on trust calculations highlights that the beneficiary’s share of net income is worked out by reference to their present entitlement proportions. In practice, this can create timing mismatches between entitlement, cash receipts, and personal tax bills.

Income Characteristics

A distribution can retain tax characteristics (for example, capital gains or franked distributions) depending on how the trust accounts for and distributes income. Beneficiaries should obtain the trust’s annual tax statement and distribution resolution for their records.

Foreign Assets and Overseas Inheritances

Overseas inheritances are tax-neutral on receipt, but Australian residents are assessed on worldwide ordinary income under Section 6-5 of the Income Tax Assessment Act 1997, which is why foreign rent and foreign dividends can become assessable once you own the asset.

Where foreign tax has been paid, Division 770 provides the foreign income tax offset framework and its limit rules. Overseas probate and local taxes may also apply in the asset’s jurisdiction, separate to Australian rules.

Recordkeeping and Reporting Requirements

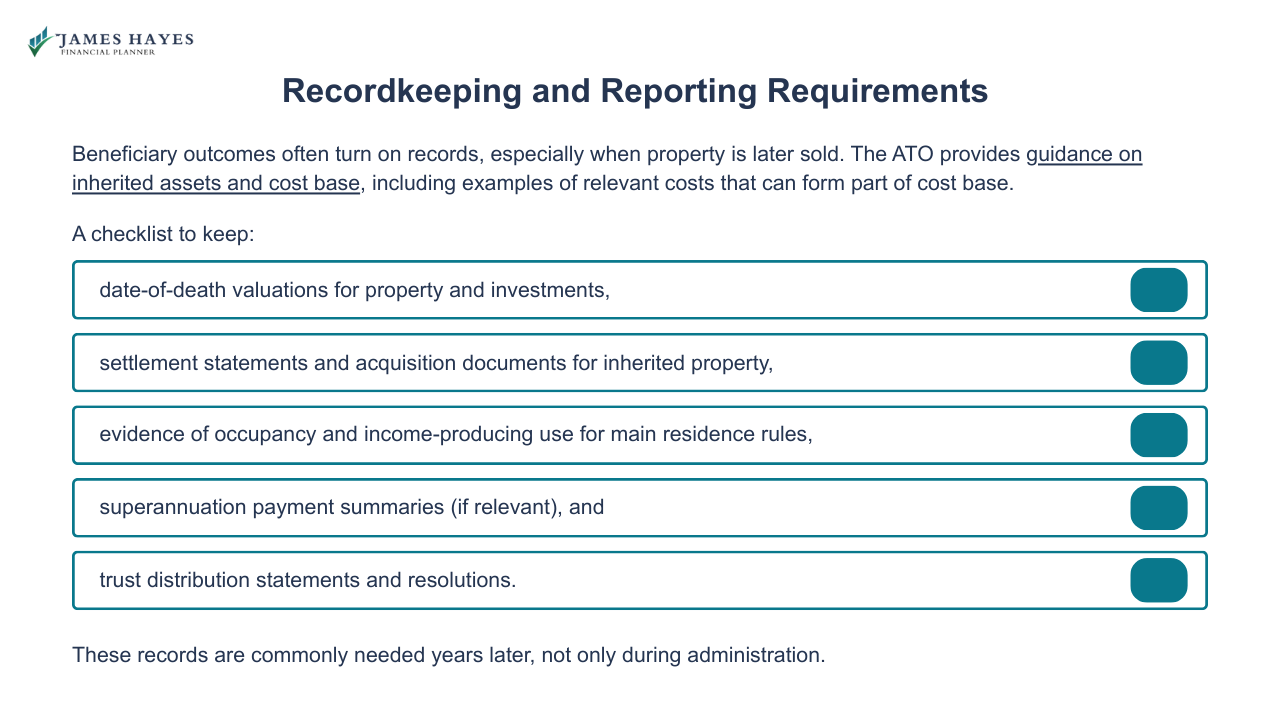

Beneficiary outcomes often turn on records, especially when property is later sold. The ATO provides guidance on inherited assets and cost base, including examples of relevant costs that can form part of cost base.

A checklist to keep:

date-of-death valuations for property and investments,

settlement statements and acquisition documents for inherited property,

evidence of occupancy and income-producing use for main residence rules,

superannuation payment summaries (if relevant), and

trust distribution statements and resolutions.

These records are commonly needed years later, not only during administration.

When to Seek Professional Advice

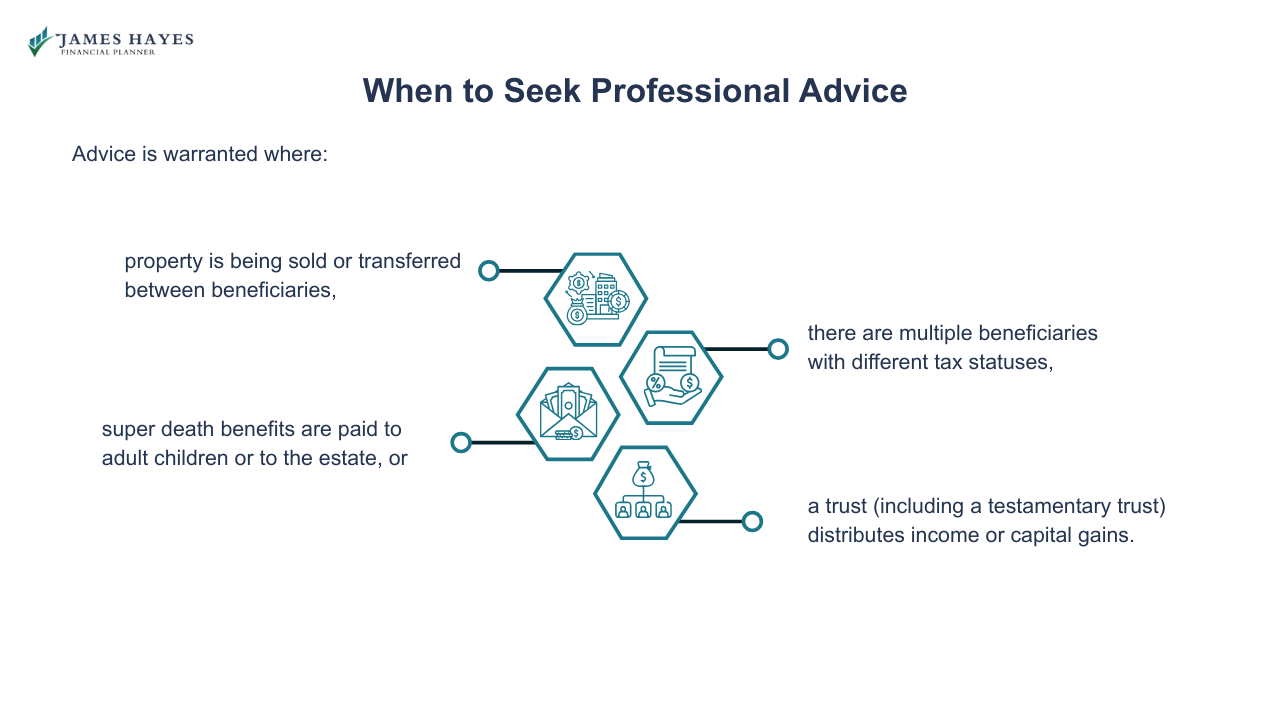

Advice is warranted where:

property is being sold or transferred between beneficiaries,

there are multiple beneficiaries with different tax statuses,

super death benefits are paid to adult children or to the estate, or

a trust (including a testamentary trust) distributes income or capital gains.

For wills, probate, and disputes, a solicitor is the lead adviser. For beneficiary cash flow, investment structure, and retirement strategy after funds are received, a financial planner can coordinate the plan with your tax agent.

Conclusion

Beneficiaries are not taxed on inheritances simply because they receive assets, but tax consequences arise later through income, CGT events, superannuation death benefits, and trust entitlements. Legislative detail and documentation determine outcomes, particularly for property and super.

If you expect to receive an inheritance and want a plan for investing proceeds, managing risk, and aligning the outcome with your retirement timeline, James Hayes can help with financial planning after funds are received. Book your free 15-minute call with him.

FAQs

-

Inherited cash is generally not assessable income merely because it was inherited. Tax reporting relates to interest earned after you hold the cash, income from assets you inherit, and capital gains if you later sell inherited CGT assets. Keep records for later calculations.

-

CGT is not triggered merely because you inherit a CGT asset from a deceased estate. It arises later when you dispose of the asset, such as a sale, which can trigger CGT event A1. The cost base rules for inherited assets then determine the gain.

-

The date-of-death valuation (where relevant), evidence of whether the dwelling was the deceased’s main residence, documents showing any income-producing use, and details of estate legal costs that may form part of cost base. These are required to calculate exemptions and any eventual capital gain.

-

The tax outcome depends on whether the recipient is a “death benefits dependant” under Section 302-195 of the Income Tax Assessment Act 1997. ATO guidance notes lump sums to dependants are tax-free, while payments where beneficiaries are not dependants can attract tax on the taxable component, with different rates for taxed and untaxed elements.

-

Trust income is often assessed to beneficiaries who are “presently entitled” under Division 6 of the Income Tax Assessment Act 1936, including Section 97. This can apply even if cash is received later. Beneficiaries should obtain the trust tax statement and distribution resolution, because the timing and character of distributed income affect the personal tax return.

-

Overseas inheritances are not taxed on receipt, but income from foreign assets can be assessable to Australian residents under SectionSection 6-5 of the Income Tax Assessment Act 1997. If foreign tax is paid, Division 770 provides foreign income tax offset rules and limits. Overseas probate and local taxes may also apply where the asset is located.

Inheritance & Estate Planning Knowledge Bundle

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.