Overview of Inheritance and Estate Planning in Australia

Summary

Inheritance and estate planning in Australia is about controlling who receives your assets, how they receive them, and what tax or legal steps apply after death. Key issues include wills and intestacy rules, superannuation death benefits, probate, capital gains tax on inherited assets, and dispute risk under state succession laws (NSW rules often apply locally).

Table of Contents

- Introduction

- What Counts as an Estate in Australia?

- How Does Inheritance Work in Australia?

- Estate Planning Documents and Decisions

- Superannuation and Estate Planning

- Tax Considerations for Beneficiaries

- Disputes, Family Provision Claims, and Blended Families

- Gifting vs Inheriting

- What to Do After Receiving an Inheritance

- Ethical Wills and Legacy Planning

- When to Revisit Your Estate Plan

- How James Hayes Can Help

- FAQs

- Inheritance & Estate Planning Knowledge Bundle

Introduction

For Sydney wealth builders (35–50) and pre-retirees or retirees (55–65), estate planning intersects with property, superannuation, family structures, and tax records. Australia has no inheritance tax in the traditional sense, but beneficiaries can face tax outcomes depending on the asset type.

This guide is general information, not legal or tax advice. For wills, probate, and estate disputes, a solicitor is usually the lead adviser. A financial planner supports the financial structure, beneficiary outcomes, and post-inheritance strategy.

What Counts as an Estate in Australia?

An estate is the pool of assets and liabilities that can be dealt with under a will (or intestacy rules if there is no valid will). In practice, some valuable items pass outside the estate, which is why people are often surprised by the outcome. Before looking at rules, it helps to separate “estate assets” and “non-estate assets”.

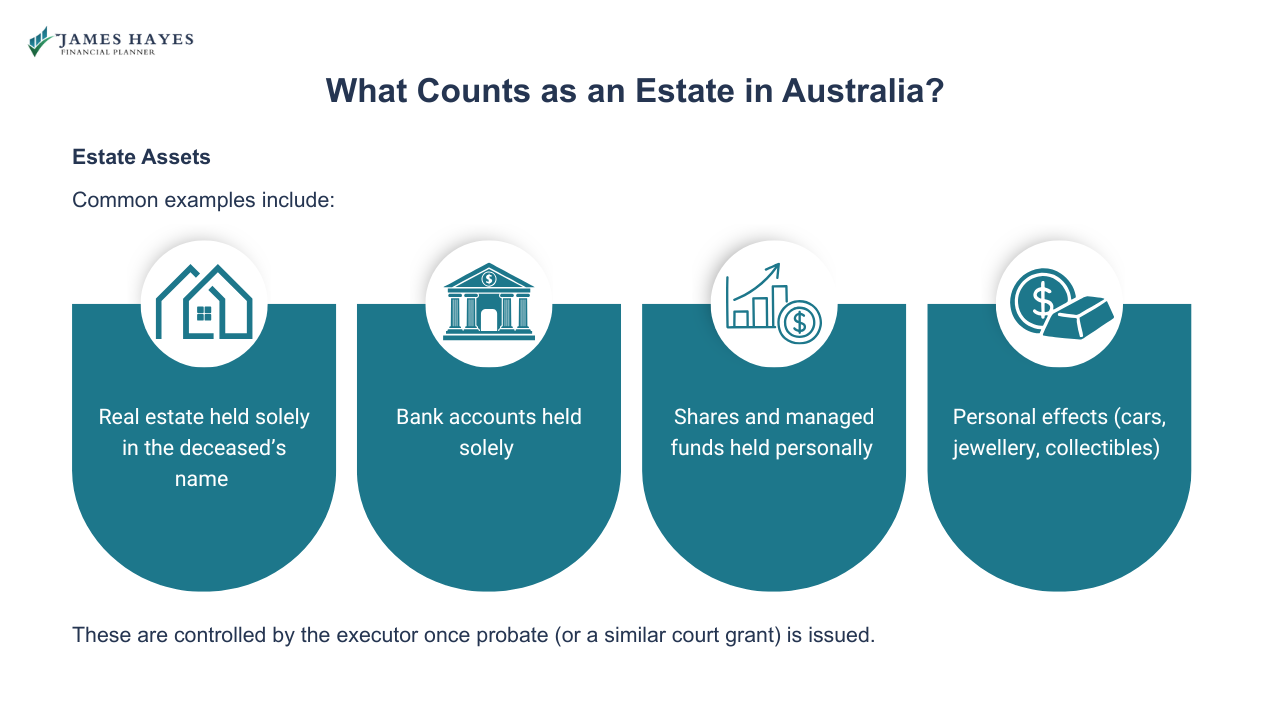

Estate Assets

Common examples include:

Real estate held solely in the deceased’s name

Bank accounts held solely

Shares and managed funds held personally

Personal effects (cars, jewellery, collectibles)

These are controlled by the executor once probate (or a similar court grant) is issued.

Non-Estate Assets

Non-estate transfers include:

Superannuation death benefits (paid under fund rules and trustee decision-making, and guided by a valid nomination)

Jointly held property as joint tenants (passes to the surviving joint tenant by survivorship, rather than under the will)

Assets in a trust or company (controlled by trustee/director succession and governing documents, not the will)

This is a planning pressure point for Sydney households where super and property make up a large share of net worth.

How Does Inheritance Work in Australia?

Inheritance administration is state and territory based. In NSW, it is governed by the Succession Act 2006.

If There Is a Valid Will

A valid will sets out who receives estate assets and appoints an executor. In NSW, the executor applies to the Supreme Court for a grant of probate, which is the court’s confirmation that the will can be acted on.

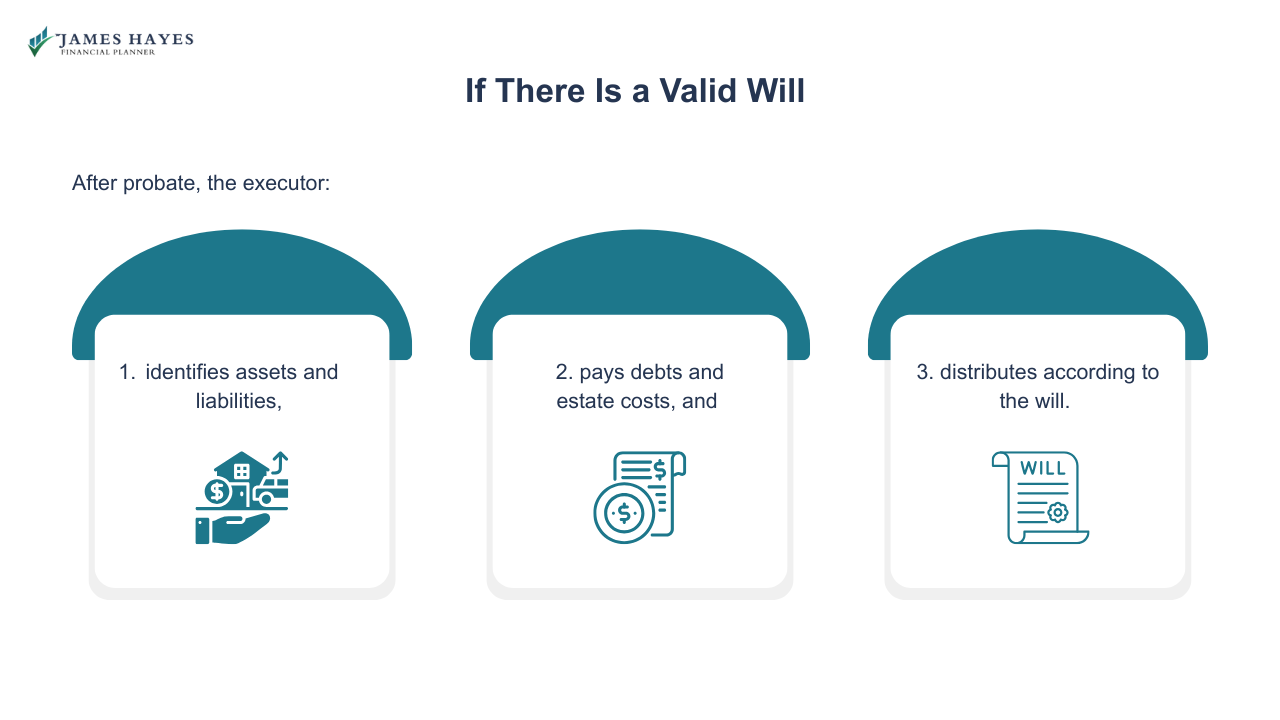

After probate, the executor:

identifies assets and liabilities,

pays debts and estate costs, and

distributes according to the will.

If There Is No Will (Intestacy)

If there is no valid will, intestacy rules dictate who receives the estate and in what order. The process still needs a court-appointed administrator (letters of administration), and distribution follows the state’s legislative scheme rather than personal preference.

For families with blended arrangements, estranged relatives, or uneven asset ownership, intestacy is a frequent cause of delay and dispute.

Estate Planning Documents and Decisions

Estate planning is not only a will. It is the match between your legal documents and how your assets are held.

Will, Executor Choices, and Testamentary Trusts

A will handles estate assets and appoints an executor. Some wills also establish testamentary trusts for beneficiary control (for example, managing distributions to minors or protecting vulnerable beneficiaries).

A family with one child under 18 and one adult child may prefer different structures for timing and control of distributions, even if the end beneficiaries are the same.

Powers of Attorney and Incapacity Planning

Most estate problems begin before death, through incapacity. State-based enduring powers of attorney and guardianship appointments can determine who can act if you lose decision-making capacity. This is separate to inheritance, but it often affects asset sales, pension commencements, and document updates late in life.

Superannuation and Estate Planning

Super is a major asset for both retirees and wealth builders, and it does not automatically follow the will. Super is governed by the Superannuation Act 1916, fund trust deeds, and trustee decisions, with nominations often being a key practical control.

Death Benefit Nominations and Reversionary Pensions

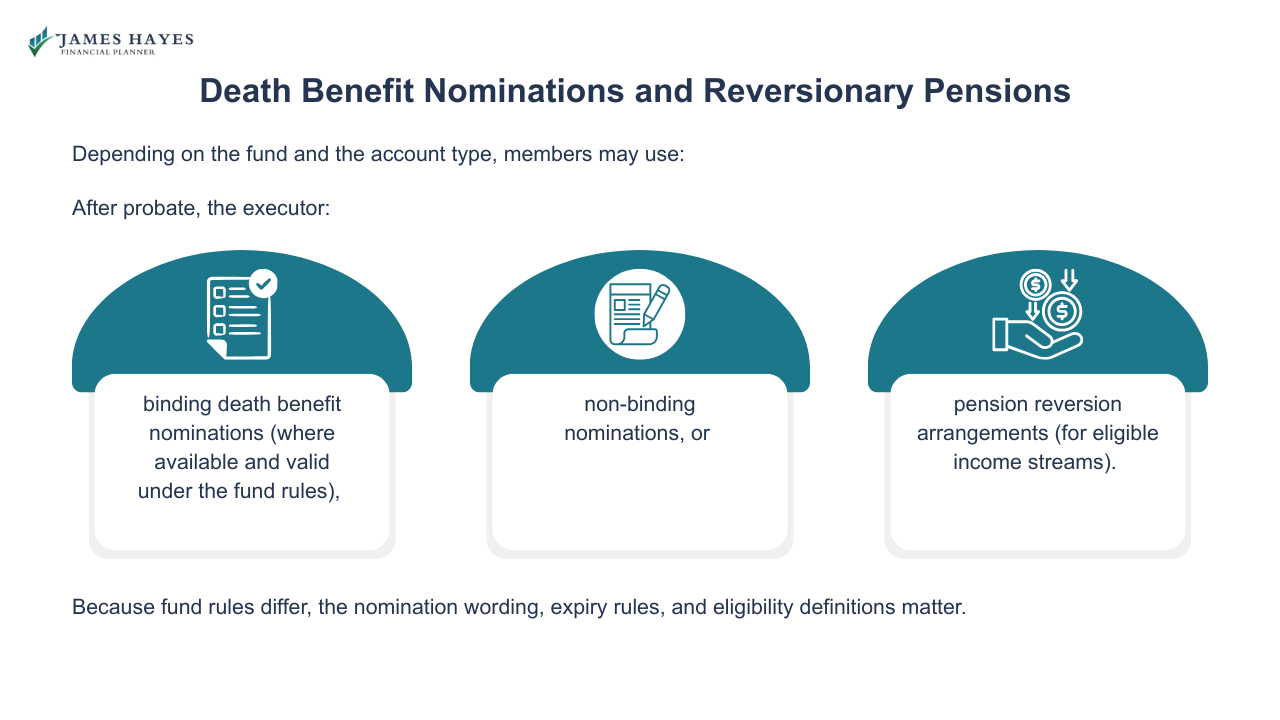

Depending on the fund and the account type, members may use:

binding death benefit nominations (where available and valid under the fund rules),

non-binding nominations, or

pension reversion arrangements (for eligible income streams).

Because fund rules differ, the nomination wording, expiry rules, and eligibility definitions matter.

Tax on Super Death Benefits

Super death benefits can be taxed differently depending on who receives them and how the benefit is paid (lump sum vs income stream). The ATO guidance sets out the framework used for taxation outcomes.

This is one of the few areas where inheritance can produce an immediate tax cost, so it often warrants specific planning alongside the will.

Free eBook: Inheritance First 30 Days Checklist + Document List

〰️

Free eBook: Inheritance First 30 Days Checklist + Document List 〰️

Tax Considerations for Beneficiaries

Australia has no inheritance or estate taxes, but tax can apply to income produced by inherited assets and to capital gains when assets are sold.

Capital Gains Tax on Inherited Assets

In many cases, beneficiaries effectively take over the deceased’s cost base for CGT purposes (subject to specific rules). CGT is often triggered when the beneficiary or executor disposes of the asset, not when the asset is inherited.

Main Residence Exemption and the Two-Year Rule

Consider an inherited home. Sections 118-195 of the Income Tax Assessment Act 1997 set out rules that can allow a full CGT exemption for a dwelling sold by the legal personal representative or a beneficiary in certain circumstances, including time-based conditions that are often discussed as a two-year window.

Because facts change outcomes (who lived in the home, when it was rented, timing of sale), record-keeping is central.

Probate, Estate Administration, and Timing Issues

Probate is required to deal with banks, share registries, and land titles. NSW probate is handled through the Supreme Court of NSW, and published requirements can affect timing (including notice periods and expedition criteria).

Disputes, Family Provision Claims, and Blended Families

Even with a valid will, NSW law can allow eligible persons to seek a larger share if adequate provision is not made. The Succession Act 2006 (NSW) is the key legislation for family provision and related estate concepts.

Family Provision Claims in NSW

Eligibility and outcomes depend on relationship, dependency, financial position, and estate size. A will that is legally valid is not automatically immune from a claim.

Notional Estate in NSW

NSW has the concept of “notional estate”, which can, in certain circumstances, bring some assets back into the claim pool even if they were transferred before death. This can be relevant when people try to move assets out of their name late in life.

Gifting vs Inheriting

People compare transferring wealth during life versus leaving it via a will. Whether an endowment is an inheritance or a gift depends on control, tax, and dispute risk.

Gifting During Life

Gifting can shift ownership immediately, which may trigger CGT (and, for property, stamp duty depending on the transaction and jurisdiction). It also changes asset control, which is a risk if circumstances change.

Leaving Assets Via the Estate

A will can stage transfers, set conditions, and coordinate with trustee and company succession. It also leaves a paper trail for executors and the ATO where tax records are needed.

What to Do After Receiving an Inheritance

Once you expect to receive funds or assets, the focus shifts from legal administration to cash flow, tax records, and portfolio structure.

First Steps That Protect Decision Quality

Start with the facts:

what asset(s) you are receiving,

whether it is from the estate or outside the estate (especially super),

expected timing, and

what cost base and tax records exist.

The ATO notes that while inherited cash is not taxed as an inheritance, income and CGT outcomes can follow the asset.

Turning an Inheritance into a Plan

A financial plan tests:

whether to hold or sell inherited property,

how to invest proceeds relative to your timeframe and risk tolerance, and

how this interacts with super contributions and retirement income planning.

Ethical Wills and Legacy Planning

A legacy plan can include non-financial intent like values, family decision rules, and guidance for heirs. This is often documented as a non-binding “ethical will” or letter of wishes that coexists alongside legal documents.

Used well, it clarifies why decisions were made (for example, unequal distributions due to prior gifts, or support provided during life), which can assist communication even though it is not a substitute for a properly drafted will.

When to Revisit Your Estate Plan

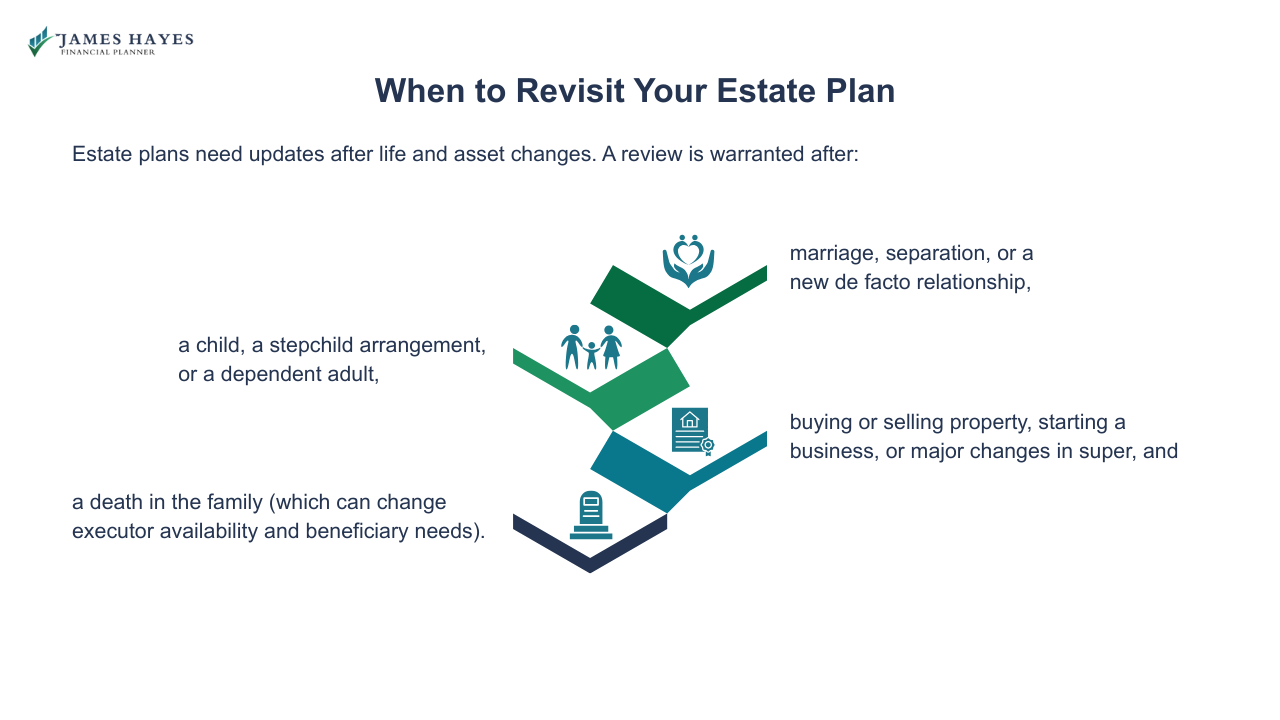

Estate plans need updates after life and asset changes. A review is warranted after:

marriage, separation, or a new de facto relationship,

a child, a stepchild arrangement, or a dependent adult,

buying or selling property, starting a business, or major changes in super, and

a death in the family (which can change executor availability and beneficiary needs).

In South Australia, significant succession law changes were enforced on 1 January 2025 under the Succession Act 2023 (SA), a reminder that rules can change by jurisdiction over time.

How James Hayes Can Help

James Hayes is an ASIC-licensed financial planner based in Caringbah, working with wealth builders and pre-retirees or retirees across the Sutherland Shire and Greater Sydney.

In an inheritance and estate planning context, a financial planner helps you:

map asset ownership and beneficiary outcomes (including super),

model tax outcomes tied to selling or retaining inherited assets, and

set an investment and retirement strategy after an inheritance is received.

If you want to pressure-test how your property, super, and investments would transfer under your current setup, book a free 15-minute call.

FAQs

-

Australia has no inheritance or estate tax. Tax can still apply after you inherit an asset, such as capital gains tax when you sell inherited property or shares, and income tax on rent, dividends, or interest earned after you take ownership. Recordkeeping is critical for later tax reporting.

-

No, superannuation death benefits are paid under super fund laws and trustee decisions, sometimes guided by a valid nomination or pension reversion. A will can be relevant if the death benefit is paid to the estate, but the will does not automatically control super.

-

Probate is a Supreme Court grant confirming the executor’s authority to administer a will. Many banks, share registries, and NSW property transfers require probate before assets can be collected or transferred. NSW probate rules also include notice and procedural requirements that can affect timing.

-

The two-year rule is a label for timing conditions that can affect the main residence CGT exemption when a dwelling is sold after death. Sections 118-195 of the Income Tax Assessment Act 1997 outline the rules, and facts drive the outcome.

-

Yes. The Succession Act 2006 (NSW) provides for family provision claims by eligible persons in certain circumstances. A legally valid will can still be altered by a court order if the court decides adequate provision was not made. Time limits and eligibility details matter.

-

Confirm what you are receiving, when you will receive it, and whether it is from the estate or outside the estate (especially super). Then gather documents for cost base and tax records. The ATO notes there is no inheritance tax, but CGT and income tax can apply later.

Inheritance & Estate Planning Knowledge Bundle

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.