What Is Superannuation & How Does It Work in Australia?

Summary

Superannuation is Australia’s compulsory retirement savings system. Your employer pays a minimum percentage of your wage into a fund, you can add extra contributions, that money is invested at concessional tax rates, and you withdraw it under strict rules after reaching preservation age, retirement or other legal conditions of release.

Table of Contents

- Introduction

- What Is Superannuation?

- How Super Fits into Your Retirement Picture

- How Money Goes into Your Super

- How Your Super Is Invested

- How Superannuation Is Taxed

- When You Can Access Super

- What Happens When You Retire?

- Super, Estate Planning, and Death Benefits

- A Snapshot of Self-Managed Super Funds (SMSFs)

- Other Super Particulars to Plan for Over Time

- Working with a Local Financial Planner in Sutherland Shire or Sydney CBD

- FAQs

- Superannuation & SMSFs Knowledge Bundle

Introduction

Superannuation (super) is Australia’s long-term retirement savings system. For most households in the Sutherland Shire and Sydney CBD, it sits alongside the family home as one of the largest assets they will ever own.

This guide explains how super works, the rules that apply from your 30s through to retirement, and where more detailed articles in this super and SMSF series fit in.

James Hayes provides advice on super, retirement, and SMSFs. He does not assist with Centrelink Jobseeker claims, debt consolidation schemes, or early-release arrangements designed to withdraw super before the law allows.

What Is Superannuation?

Super is a tax-advantaged trust structure designed to hold money for your retirement. Your super fund receives contributions, invests them on your behalf, deducts fees and tax, and eventually pays benefits when a legal “condition of release” is met.

Money inside the super system is generally “preserved” until at least your preservation age, which is now effectively 60 for new retirees.

At a practical level, super answers three questions:

How does money go in?

How is it invested and taxed?

How and when does it come out?

The rest of this article works through those questions in order, then points you to deeper guides in this blog series when you want more detail.

Want a simple way to bring all your super details into one place? Download the Super Fundamentals Starter Pack. It helps you list every fund, capture fees, insurance, contributions, and spot areas worth reviewing before your next meeting.

How Super Fits into Your Retirement Picture

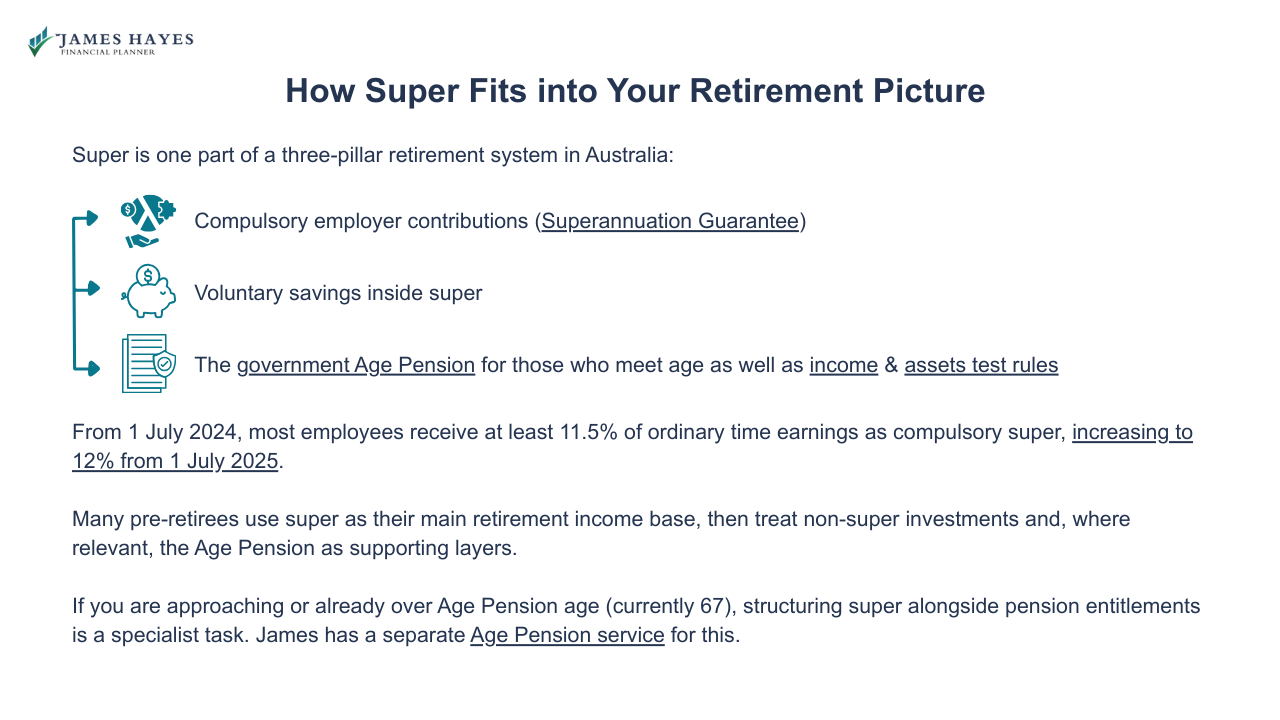

Super is one part of a three-pillar retirement system in Australia:

Compulsory employer contributions (Superannuation Guarantee)

Voluntary savings inside super

The government Age Pension for those who meet age as well as income & assets test rules

From 1 July 2024, most employees received at least 11.5% of ordinary time earnings as compulsory super, increasing to 12% from 1 July 2025.

Many pre-retirees use super as their main retirement income base, then treat non-super investments and, where relevant, the Age Pension as supporting layers.

If you are approaching or already over Age Pension age (currently 67), structuring super alongside pension entitlements is a specialist task. James has a separate Age Pension service for this.

How Money Goes into Your Super

Money reaches your super fund through several contribution types. Each has its own caps, timing rules, and tax treatment. Each has its own caps, timing rules, and tax treatment, which we cover in full in Super Contribution Rules 2025 and Tax Benefits of Super Contributions.

Employer Superannuation Guarantee (SG)

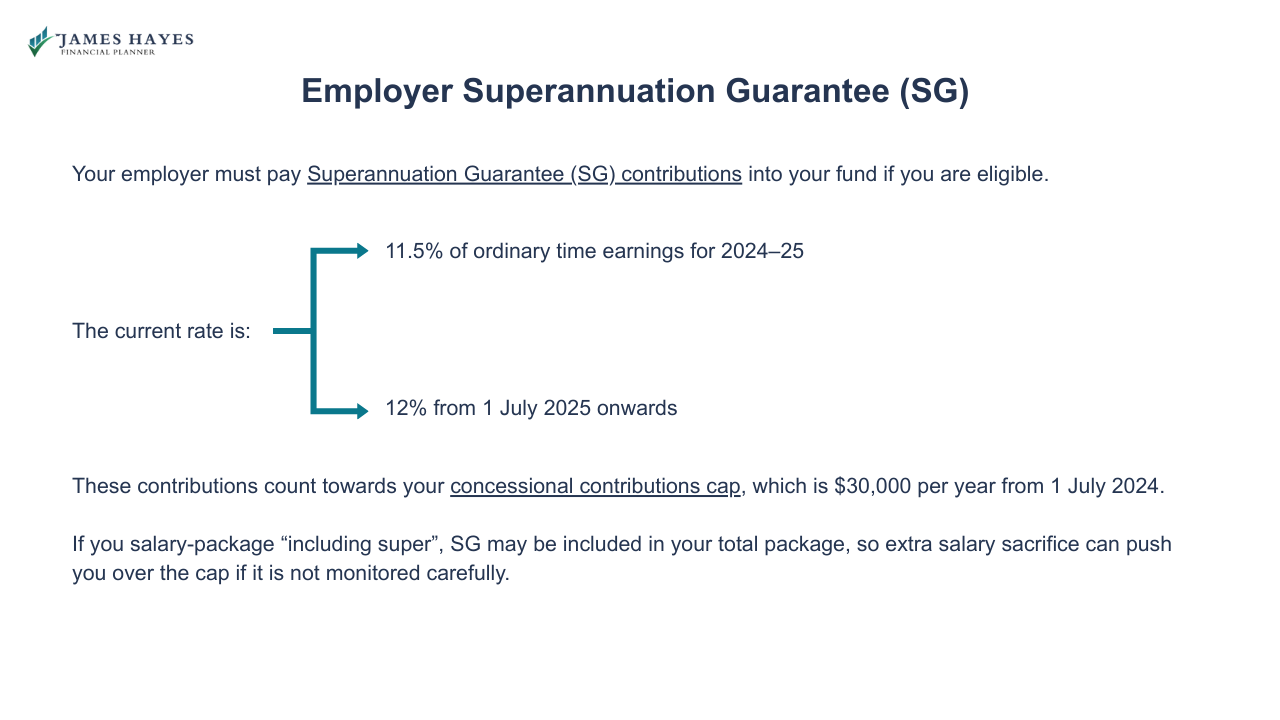

Your employer must pay Superannuation Guarantee (SG) contributions into your fund if you are eligible. The current rate is:

11.5% of ordinary time earnings for 2024–25

12% from 1 July 2025 onwards

These contributions count towards your concessional contributions cap, which is $30,000 per year from 1 July 2024.

If you salary-package “including super”, SG may be included in your total package, so extra salary sacrifice can push you over the cap if it is not monitored carefully.

Voluntary Concessional (Before-tax) Contributions

On top of SG, you can make before-tax contributions, which are usually taxed at 15% inside the fund rather than at your marginal tax rate. These include:

Salary sacrifice from your employer payroll

Personal contributions you later claim as a tax deduction

From 1 July 2024, all concessional contributions – SG, salary sacrifice and personal deductible – share a single $30,000 cap. If your income plus concessional contributions exceeds $250,000, an extra 15% contributions tax (Division 293) may apply.

If you have a total super balance under $500,000, you may be able to “catch up” unused concessional cap amounts from the previous five financial years.

The separate article Tax Benefits of Super Contributions will compare concessional contributions to investing outside super.

Non-concessional (After-tax) Contributions

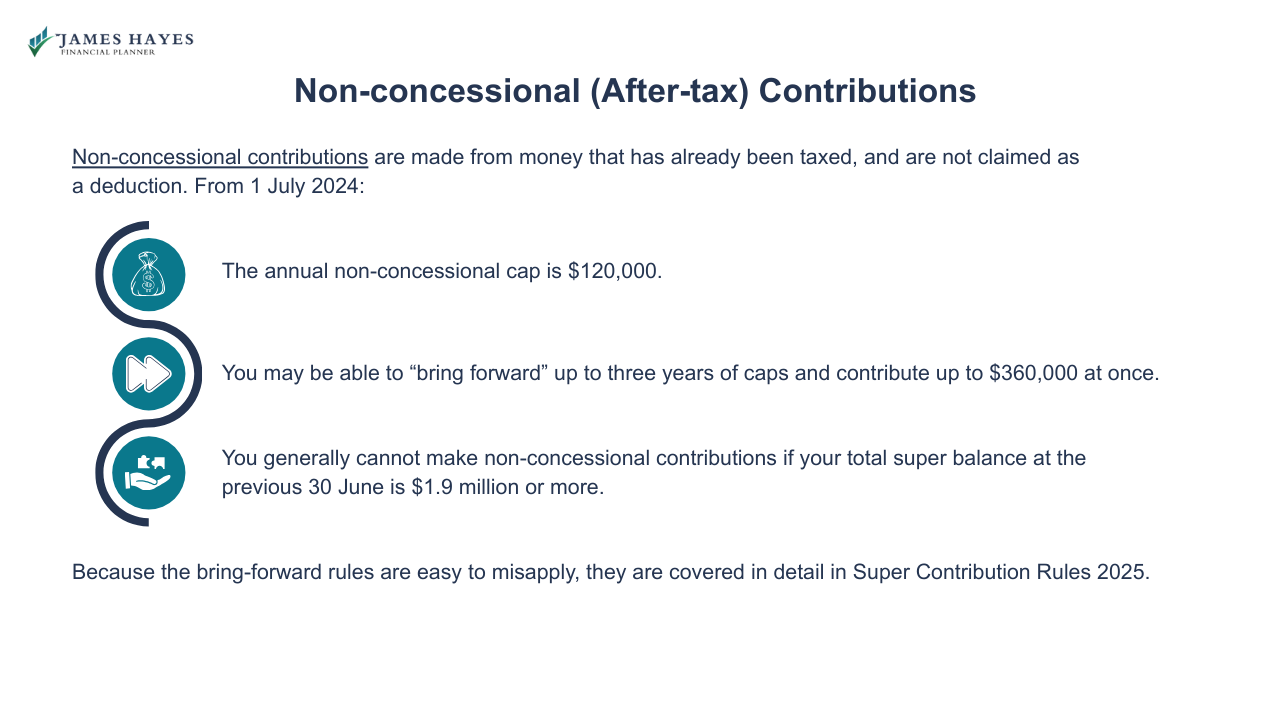

Non-concessional contributions are made from money that has already been taxed, and are not claimed as a deduction. From 1 July 2024:

The annual non-concessional cap is $120,000.

You may be able to “bring forward” up to three years of caps and contribute up to $360,000 at once.

You generally cannot make non-concessional contributions if your total super balance at the previous 30 June is $1.9 million or more.

Because the bring-forward rules are easy to misapply, they are covered in detail in Super Contribution Rules 2025.

Government and Spouse Contributions

For some households, extra contributions from the government or a spouse can help build balances more evenly.

Examples include:

Government co-contribution: Up to $500 if you make eligible personal after-tax contributions and your income is within certain thresholds.

Low-income super tax offset (LISTO): Up to $500 to refund contributions tax for low-income earners.

Spouse contributions and tax offset: A higher-earning spouse contributes to their partner’s super and may receive a tax offset.

Contribution splitting: One partner transfers part of their concessional contributions to the other’s fund, usually to balance retirement savings.

These strategies are especially relevant for couples where one partner has taken time out of the workforce or earns less, which is common in households affected by the gender super gap.

The separate guide Women & Super Gap Awareness will focus on this issue and practical repair strategies over time.

Not fully sure where all your super sits or what you’re paying for? Get James' free Super Fundamentals Starter Pack. It gives you one clean worksheet to list your funds, fees, insurance, and contributions so you’re not making decisions in the dark.

Free eBook: Understanding Superannuation and How Does It Work in Australia

〰️

Free eBook: Understanding Superannuation and How Does It Work in Australia 〰️

How Your Super Is Invested

Inside the fund, your balance is pooled with other members’ money and invested in assets such as:

Shares (Australian and international)

Property and infrastructure

Fixed interest and cash

Alternative assets

Most people are placed in a default (MySuper) investment option unless they make a choice. MySuper options are usually diversified, with a mix of growth and defensive assets, but actual risk levels vary across funds.

Your choices here affect long-term returns more than small fee or tax differences. Higher-growth options usually suit longer timeframes, while pre-retirees often prefer a more measured risk profile.

Ethical and sustainable super options sit within this same framework. They use positive and negative screens to avoid certain industries (for example, fossil fuels or controversial weapons) and tilt towards companies meeting environmental or social criteria. Because ethical filters and performance vary widely between funds, we cover this in Ethical & Sustainable Super Funds rather than in depth here.

How Superannuation Is Taxed

Super’s main attraction is its tax treatment. There are three levels:

Tax on contributions

Tax on earnings while you are still accumulating

Tax on withdrawals in retirement

Tax on Contributions

Most concessional contributions (SG, salary sacrifice, deductible personal contributions) are taxed at 15% within the fund. High-income earners may pay an extra 15% (Division 293) on some or all concessional contributions if income plus concessional contributions exceed $250,000.

Non-concessional contributions are not taxed on the way in, because the money has already been taxed, but exceeding the cap can lead to penalty tax.

Tax on Investment Earnings

During the accumulation phase, earnings inside super (interest, dividends, rent, and realised capital gains) are generally taxed at a maximum of 15%, with capital gains effectively taxed at 10% if the asset has been held for more than 12 months.

Once part of your balance moves into an account-based pension and sits within your transfer balance cap (currently $1.9 million, expected to move to $2 million from 1 July 2025), earnings on that portion are usually tax-free.

Tax on Withdrawals

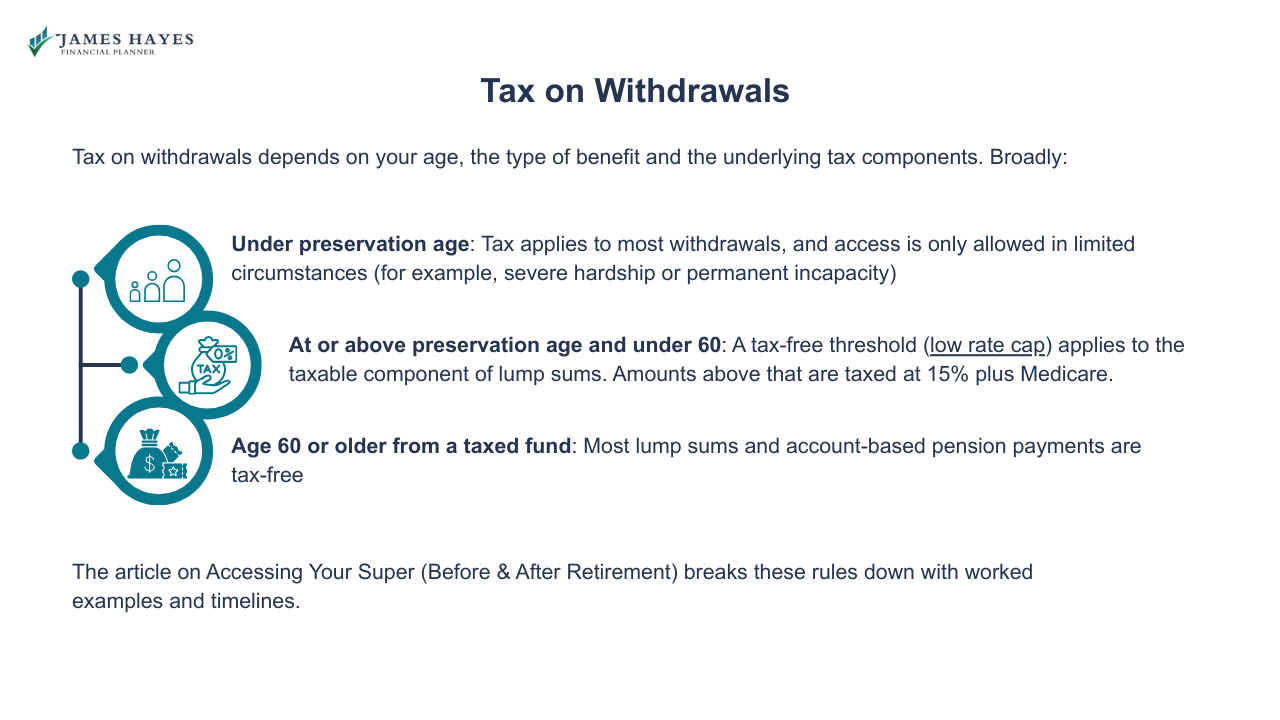

Tax on withdrawals depends on your age, the type of benefit and the underlying tax components. Broadly:

Under preservation age: Tax applies to most withdrawals, and access is only allowed in limited circumstances (for example, severe hardship or permanent incapacity).

At or above preservation age and under 60: A tax-free threshold (low rate cap) applies to the taxable component of lump sums. Amounts above that are taxed at 15% plus Medicare.

Age 60 or older from a taxed fund: Most lump sums and account-based pension payments are tax-free.

The article on Accessing Your Super (Before & After Retirement) breaks these rules down with worked examples and timelines.

When You Can Access Super

Super is deliberately difficult to access. The law limits withdrawals to specific conditions of release. The most common are:

Reaching your preservation age and retiring

Reaching preservation age and starting a transition-to-retirement (TTR) income stream

Ceasing an employment arrangement after age 60

Reaching age 65 (access allowed even if still working)

Death (benefits paid to dependants or your estate)

For 2024–25 and future years, preservation age is effectively 60 for everyone who has not already reached it, based on date of birth.

There are special early-release provisions (for example, permanent incapacity or very severe financial hardship). James does not advise on schemes that try to access super outside lawful conditions, or on debt consolidation structures that risk breaching superannuation law.

The detailed article Accessing Your Super (Before & After Retirement) will map out each condition of release and how they apply to both super funds and SMSFs.

What Happens When You Retire?

When you reach preservation age and meet a condition of release (for example, fully retiring or ceasing a job after 60), you can generally move from accumulation into retirement phase.

Your main options are:

Start an account-based pension: Regular income payments, with minimum drawdown rates that increase as you age.

Take one or more lump sums: Suited to one-off needs like clearing a mortgage or funding renovations.

Use a combination: Keep some money in accumulation, some in pension, and withdraw lump sums over time.

For those still working but wanting to cut back hours, a transition-to-retirement income stream can supplement salary between preservation age and full retirement.

The article Accessing Your Super (Before & After Retirement) will cover drawdown strategies, while How to Grow Your Super Balance will look at pre-retirement contribution and investment planning.

Not sure how ready your super actually is for retirement? The Super Fundamentals Starter Pack walks you through your balances, contributions, and insurance so you can see exactly where you stand before making big decisions.

Super, Estate Planning, and Death Benefits

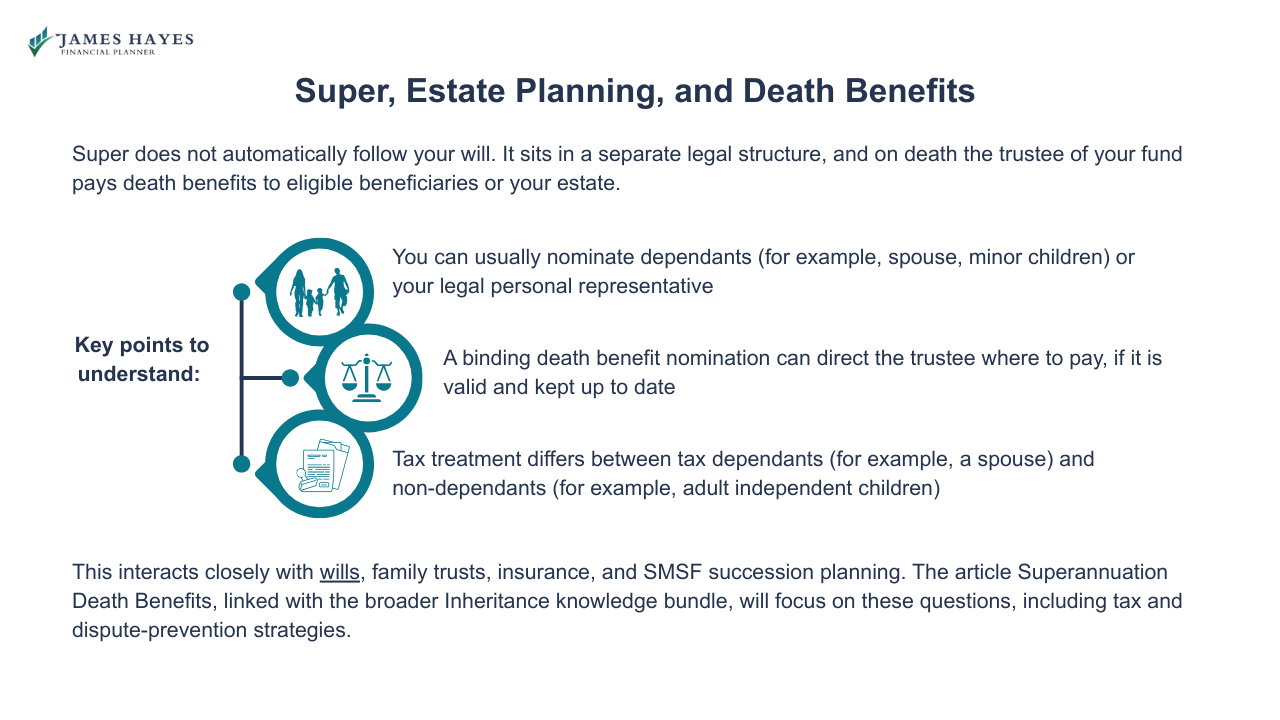

Super does not automatically follow your will. It sits in a separate legal structure, and on death the trustee of your fund pays death benefits to eligible beneficiaries or your estate.

Key points to understand:

You can usually nominate dependants (for example, spouse, minor children) or your legal personal representative

A binding death benefit nomination can direct the trustee where to pay, if it is valid and kept up to date

Tax treatment differs between tax dependants (for example, a spouse) and non-dependants (for example, adult independent children)

This interacts closely with wills, family trusts, insurance, and SMSF succession planning. The article Superannuation Death Benefits, linked with the broader Inheritance knowledge bundle, will focus on these questions, including tax and dispute-prevention strategies.

A Snapshot of Self-Managed Super Funds (SMSFs)

A self-managed super fund (SMSF) is a private super fund that you run yourself. It is a trust, set up solely to provide retirement benefits to its members and their dependants.

In an SMSF:

Members are usually individual trustees or directors of a corporate trustee.

You make the investment decisions and are responsible for compliance with super and tax law.

There can be up to six members.

ASIC has recently highlighted that a significant proportion of SMSF advice files fail the “best interests” test, and that poor SMSF structures can cause serious harm to retirement outcomes.

SMSFs can suit investors who:

Have sufficient capital (often at least several hundred thousand dollars)

Are comfortable with trustee obligations

Want specific investment features (for example, business property in super)

But they are not right for everyone. James’ SMSF advice focuses on suitability, investment strategy and ongoing compliance, rather than aggressive or early-release schemes.

Before you compare funds or change your contributions, use the Super Fundamentals Starter Pack to map your balances, fees, insurance, and nominations. It turns scattered statements into a clear snapshot you can actually work with.

Detailed SMSF topics sit in separate articles:

Self-Managed Super Funds (SMSFs) Explained (structure, pros & cons)

Setting Up an SMSF (step-by-step setup process)

SMSF Investment Rules 2025 (what you can and cannot invest in)

SMSF Compliance & Administration (audits, reporting, and trustee duties)

Other Super Particulars to Plan for Over Time

Super interacts with many real-world situations. This section helps you see how the pieces fit together.

Growing Your Super Balance

For wealth builders in their 30s, 40s, and early 50s, the priority is getting enough into super early enough for compounding to work. Strategies include salary sacrifice, personal deductible contributions, non-concessional contributions, and contribution splitting within couples.

The article How to Grow Your Super Balance will focus on contribution and investment tactics by decade, including trade-offs with paying down home loans and investing outside super.

Rolling Over Super Funds

Many people have multiple funds from changing employers. Consolidating into one well-chosen fund can simplify fees and investment decisions. Before rolling over, you need to review insurance, investment options, and any exit fees or tax implications.

The guide Rolling Over Super Funds will cover practical steps, including how to compare super funds and when it can make sense to keep certain legacy benefits.

Ethical & Sustainable Super

If you want your retirement savings to align with environmental or social values, you can usually choose an ethical option within an existing fund or switch to a specialist ethical fund. Approaches vary, from simple exclusions (for example, tobacco) to impact-focused strategies.

The article Ethical & Sustainable Super Funds will explain screening methods, greenwashing risks, and performance considerations in more depth.

Super for the Self-employed

If you are self-employed, no employer is required to pay SG for you. You decide whether to contribute and how much. Missed contributions during busy years can create a gap that is hard to close later.

The dedicated article Super for the Self-Employed will outline contribution options, tax deductions, and cashflow planning for business owners and contractors.

Super and Divorce / Relationship Splits

Under Australian family law, super is treated as property. On separation, couples can value their super interests and split them through agreement or court order. The split stays within the super system – it usually cannot be taken as cash.

The article Super and Divorce / Relationship Splits will cover how valuations, splitting orders, and timing work, and how to protect retirement outcomes during property settlements.

Women and the Super Gap

On average, Australian women retire with substantially less super than men, often 20–30% lower balances in the years just before retirement. Career breaks, part-time work, and pay gaps are key drivers.

The article Women & Super Gap Awareness will focus on practical steps – including contributions, spouse strategies, and super splitting – to help close that gap over time.

Before working through these next steps, take a moment to go through the Super Fundamentals Starter Pack. It’s an easy, step-by-step guide to organise your super and spot the areas that deserve a closer look.

Working with a Local Financial Planner in Sutherland Shire or Sydney CBD

Super is a national system, but personal decisions are local. For households in the Sutherland Shire and Sydney CBD, the right strategy depends on:

Your age, income, and business or employment structure

Existing super balances and investment mix

Home ownership and debt position

Relationship status and estate planning priorities

James Hayes is an ASIC-licensed financial planner based in Caringbah who works with wealth builders, pre-retirees, and retirees across the Shire and Sydney CBD on super, SMSFs, investments, and estate planning.

A typical super engagement may cover:

Mapping how much you need in retirement and what your super can realistically support

Structuring contributions within current caps and tax rules

Selecting or reviewing funds and investment options (including SMSFs where appropriate)

Planning the transition from work income to super income

Coordinating super with wills, death benefit nominations and, where relevant, Age Pension advice

If you would like advice tailored to your situation rather than general rules, you can book a free 15-minute call.

FAQs

-

Superannuation is a retirement savings system where your employer and, optionally, you contribute into a fund that invests on your behalf. Contributions and earnings receive concessional tax treatment, and the balance is generally preserved until you reach your preservation age, retire, turn 65 or meet another condition of release.

-

There is no universal “right” balance. A common rule of thumb is aiming for super that can provide your desired annual income, indexed, for a retirement that may last 25–30 years or more. James models this using your actual spending, assets, Age Pension prospects, and investment assumptions rather than generic targets.

-

Compulsory employer contributions of 11.5%, rising to 12%, provide a base but often fall short of funding a comfortable retirement, especially for higher-income households or those with career breaks. Voluntary contributions, investment choices, and retirement age matter. A planner can quantify any shortfall and design a structured contribution plan.

-

If you die with super remaining, the fund pays a death benefit to eligible dependants (for example, a spouse or minor children) or to your estate. Tax treatment depends on the recipient and underlying components. Keeping death benefit nominations and your estate plan aligned is essential to avoid disputes or unintended outcomes.

-

In a standard fund, a professional trustee runs the fund, chooses investment menus, and handles compliance. In an SMSF, the members act as trustees, control investments, and carry legal responsibility for meeting super and tax law requirements. SMSFs offer control and flexibility but demand time, capital and governance discipline.

-

You cannot simply withdraw super while working to reduce your mortgage unless you meet a legal condition of release. Some retirees use tax-free lump sums after preservation age or 60 to clear remaining debt. Any decision to trade super for lower home debt needs modelling and independent financial advice.

-

No. James does not assist with early-release schemes designed to access super outside standard conditions of release, or with debt consolidation structures that rely on questionable withdrawals. His advice focuses on lawful contribution, investment, and retirement income strategies that keep your super working inside the rules over the long term.

-

Online calculators and fund tools provide useful starting points but cannot fully account for your tax position, business structures, estate planning, or relationship dynamics. A local planner can review your full balance sheet, model trade-offs, explain legislation in plain language, and coordinate super with investments, property, and pension strategies.

Superannuation & SMSFs Knowledge Bundle

- How to Grow Your Super Balance

- Super Contribution Rules 2025

- Tax Benefits of Super Contributions

- Accessing Your Super (Before & After Retirement)

- Superannuation Death Benefits

- Self-Managed Super Funds (SMSFs) Explained

- Setting Up an SMSF

- SMSF Investment Rules 2025

- SMSF Compliance & Administration

- Rolling Over Super Funds

- Ethical & Sustainable Super Funds

- Super for the Self-Employed

- Super and Divorce / Relationship Splits

- Women & Super Gap Awareness

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.