Local Financial Services in Sutherland Shire

Summary

Sutherland Shire residents thrive with financial advice tailored to property, commuting, and retirement goals. The financial planning strategy should align your cashflow and super with suburb-level realities and evolve as your life and the financial year progress. It is practical, accessible, and built for those who value staying in the Shire.

Table of Contents

Introduction

If you live in The Shire, you already know the lifestyle is different. Beaches, river, bush, and tight-knit suburbs shape daily decisions – including money decisions. This guide explains how local financial advice maps to these suburb-specific needs and shows how a Sutherland Shire-based adviser can help you reach your goals while staying local.

Why Choose a Local Sutherland Shire Financial Adviser?

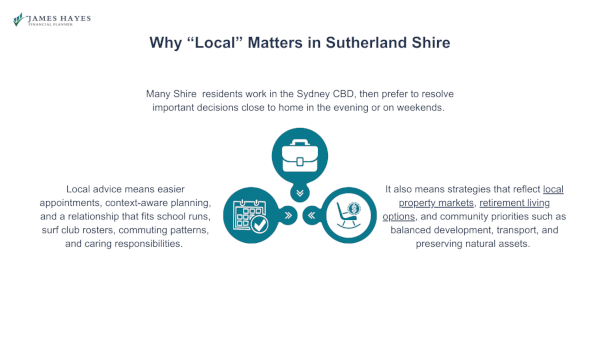

Many people in the Shire work in the Sydney CBD, then prefer to deal with important decisions closer to home in the evenings or on weekends. Working with a local adviser usually means appointments are easier to book, advice is shaped by your lifestyle, and the relationship fits around school runs, surf club rosters, commuting, and caring responsibilities.

It also means your planner is acutely aware of the local context, including Shire property prices, retirement living options, and community priorities.

Facts That Shape Money Decisions in the Shire

Sutherland Shire is around 26 km south-southwest of Sydney’s CBD, covers roughly 370 km², and includes major natural areas such as the Royal National Park, the Georges River, and the Port Hacking estuary.

The Shire’s population was about 230,000 at the 2021 Census, with a median age of 41 and incomes above the national average. Households average 2.7 people, and freestanding homes are common. Larger homes often come with bigger, less optional costs like renovations and ongoing maintenance, higher insurance needs, and, later on, bigger decisions around downsizing and what to do with property equity.

Residents also consistently rate quality of life highly. In Council’s 2024 community engagement, people ranked access to beaches, parks, and nature as top strengths, alongside a friendly community. At the same time, common concerns included traffic congestion, population growth, and the need for infrastructure to keep pace with housing.

Congestion requires you to plan for car upgrades, tolls, and high commuting costs. Similarly, regional growth forces families to weigh school and childcare proximity against transport links to keep life workable. Effective planning ensures you can afford to stay in the area long-term, rather than being forced to relocate later.

Local Economy Signals That Affect Your Plan

Council’s economic strategy is focused on building more jobs in professional, scientific and technical services, and growing health care and social assistance. It also points to the ANSTO Innovation Precinct at Lucas Heights as a long-term employment hub.

The types of jobs growing locally can influence income stability, career opportunities closer to home, and the demand profile for housing, services, and aged care over time. It helps you stress-test your financial plans against the local job market you’re relying on.

The strategy also aims to strengthen local business activity and the visitor economy in and around places like Cronulla, which can affect small business conditions and some property pockets.

What could this mean for you?

Income resilience: When a region isn’t reliant on one major industry, it can reduce the risk of household income disruption if one sector slows.

Property decisions: Employment growth around Miranda, Sutherland, and Cronulla can influence rental demand and rental returns, and also affect the timing of buying, upgrading, or selling.

Retirement planning: Access to health services and aged-care options can make it easier to plan for ageing in place (staying in your home and local area as you get older), rather than having to move unexpectedly.

How do you ground your plan in local realities?

Renovate or relocate: If you’re deciding whether to upgrade your current home or move, compare the total cost of the upgrade (including contingency, holding costs, and higher insurance) against the likely change in sale value in your area. For example, Gymea or Miranda versus bayside suburbs like Yowie Bay and Lilli Pilli.

Strata in older buildings: Factor in building-specific costs such as lift maintenance funds, concrete remediation, and rising strata insurance premiums. These can materially change the true cost of ownership.

Lifestyle priorities: If being near beaches, parks, and nature is a non-negotiable for you, build it into the numbers. It can affect what you’re willing to pay, how long you plan to stay, and whether your plan supports keeping that lifestyle without compromising on other goals like school costs, retirement savings, or cash flow.

CBD by Day, Shire by Night?

Many Shire residents work in the Sydney CBD. Longer weekdays and commute time can make standard office-hour appointments unrealistic.

Being able to meet your financial planner after hours or on Saturdays makes life easier because you don’t need to take time off, rush across the city, or squeeze calls into the middle of the day. A local adviser can work with your schedule, so reviews don’t fall apart when life gets busy.

When something is time-sensitive (for example, end-of-financial-year super contributions or other deadline-driven actions), a Shire-based adviser can usually coordinate documents, signatures, and follow-ups without relying on CBD meeting times or long back-and-forth scheduling.

Life Stages in The Shire

What financial service client profiles do we see in the Sutherland Shire?

Wealth Construction (30s–50s)

At this stage, many households are balancing a mortgage with family costs and long-term goals. The focus is usually on creating a plan around:

Cashflow and mortgage strategy: Setting up a budget that covers rising costs, maintains buffers, and supports steady debt reduction.

Investing alongside the mortgage: Building a diversified portfolio (often using ETFs and managed funds) without over-committing cashflow.

Super and tax planning: Making the most of super contributions and tax settings, where appropriate, as incomes grow.

For business owners, the conversation often extends to income variability, tax planning, and making sure personal wealth isn’t completely dependent on the business. James may also point clients towards local business networks or programs if they’re useful.

Pre-retirement and Retirement (55–70s and Beyond)

Here, the work shifts from building wealth to turning savings into reliable income. Common priorities include:

Income planning: How much you can spend each year, and where that income should come from (super, investments, pensions, or other assets).

Drawdown strategy: How to structure withdrawals to manage tax, reduce the risk of running out of money, and handle market ups and downs.

Home and location decisions: Whether staying put is affordable and practical long term, and if downsizing makes sense, including the costs, the trade-offs, and what it means for cash reserves.

Health services, transport, and community connections can also affect these decisions, because they influence whether someone can comfortably stay in their home and local area as they age.

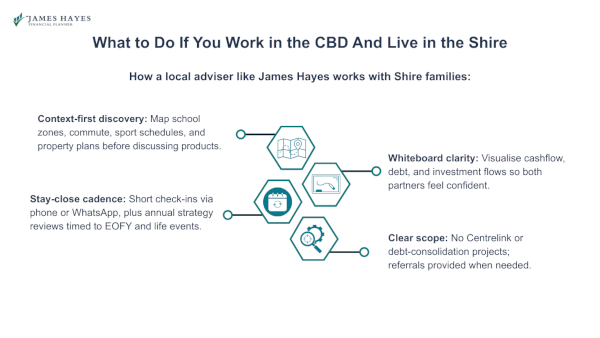

What to Do If You Work in the CBD And Live in the Shire

Follow these steps:

Book a short local call after work to triage goals and fit.

Bring numbers, including mortgage, super balances, income, insurance.

Decide your one-year wins like cash buffer, extra super, or investment automation.

Set an annual rhythm, considering periods like tax time, bonus months, and school terms.

Keep it local with documents collected, signatures signed, and progress meetings arranged close to home.

Conclusion

Better plans start with local context. In the Sutherland Shire, that means financial advice that factors in your values and the unique lifestyle of your suburb. For a strategy that supports your way of life, with the convenience of a local office, speak with James Hayes, a Shire-based adviser.

FAQs

-

No. However, most decisions happen after hours. Being local means faster meetings, stronger context on property and schools, and easier paperwork. We align cashflow to commuting costs and family logistics, then set an annual rhythm that fits your calendar, not a city office’s. Proximity saves time and stress.

-

Plenty. Bayside pockets like Gymea Bay and Yowie Bay, or beachside Cronulla, are popular for ageing in place. We check services, transport, and medical access, then design sustainable drawdowns. If downsizing, we compare nearby options first, so you keep your community ties and preferred routines intact.

-

We start with the mortgage and renovation roadmap, then build a core ETF portfolio around it. For strata units near the coast, we budget rising levies and insurance. For houses inland, we plan staged upgrades. The portfolio complements the property strategy, rather than competing with it.

-

Income depends on your tools, vehicle, and your back. We prioritise the right income protection, plan for equipment replacement, and protect cashflow during slow periods. Investing is rules-based and low maintenance, so you’re not watching markets between jobs. The plan fits seasonal rhythms and workload.

-

Maybe, but only if scale, governance, and the investment need truly justify it. We compare SMSF costs, duties, and exit options to simpler super solutions. Many high-income families get similar outcomes via contribution strategies and diversified funds, keeping weekends free from trustee paperwork.

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.