The Financial Planning Process Step by Step

Summary

Financial planning with James follows a clear path: triage call, discovery meeting, written proposal, Statement of Advice, implementation, then reviews. You receive documents in writing, fees in dollars, and a service calendar. Meetings can be online or in-office with identical standards. The plan updates as life events and priorities change.

Free eBook: Financial Adviser Meeting Preparation Checklist (Instant Download)

〰️

Free eBook: Financial Adviser Meeting Preparation Checklist (Instant Download) 〰️

Table of Contents

Introduction

Financial planning should feel structured, calm, and clear. Below is the exact process James follows with households across the Sutherland Shire and Sydney CBD. It explains what happens, who does what, and when you can expect each deliverable. If you prefer video calls, the same documents and standards apply.

This is how James Hayes works with you, step by step.

1) 15-minute Triage Call

This short call confirms your goals at a high level, whether James can help, and what to prepare. If there’s a fit, you’ll receive a checklist and a booking link for the longer session. Typical upfront fees when you proceed are quoted in dollars and confirmed in writing.

See Online Financial Planning Services in Australia for how the triage call slots into online or in-office workflows.

2) Discovery and Whiteboard Session

In this meeting, you’ll map what matters most to you, the moving parts, and the order of operations. Many pre-retirees choose a longer in-room session; time-poor professionals often prefer Zoom with screen-shares. Either way, the obligations, documents, and audit trail are identical.

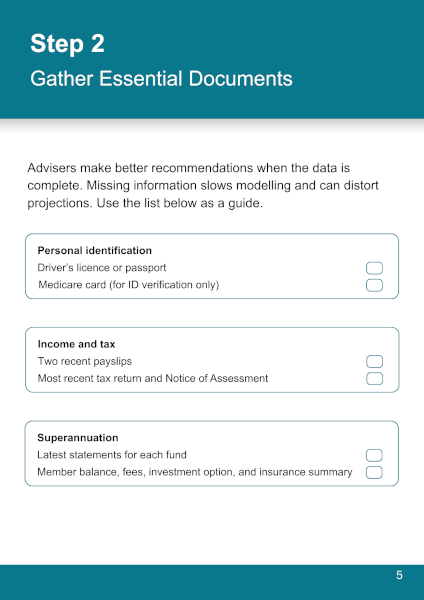

Before you arrive, gather recent super and investment statements, loan summaries, insurance schedules, two payslips, your last tax return, and estate documents. A short paragraph describing priorities speeds up the work.

3) Written Proposal

After discovery, you’ll receive a concise proposal that sets the scope, inclusions, and a timetable for the Statement of Advice (SoA). Fees are based on complexity and are shown in dollars, not percentages. You can accept, refine, or pause.

For context on fee models and questions to ask, read What Does Financial Advice Cost in NSW?

4) Fact-find and Document Collection

Once you accept the proposal, James completes a structured fact-find. Secure portals and e-signing are used where possible. You can ask for a written summary of custody, execution steps, and turnaround times for your records. If you prefer paper, the office can accommodate that.

Here’s a quick view of common items you’ll provide:

Loan summaries and offset details

Current insurance policies and medical disclosures

Two recent payslips and the last tax return

Estate documents and beneficiary nominations

Once uploaded, you’ll receive acknowledgement and any follow-up requests so nothing stalls.

5) Strategy Design and Modelling

James designs strategies that connect super, investments, insurance, and cashflow. Modelling shows ranges, trade-offs and the order of steps. For pre-retirees, this often includes contribution settings, risk calibration, projected income, and sequencing of withdrawals. Written projections support confident decisions on dates and spending.

If the work is limited to a single decision (for example, contributions or a portfolio update), you may receive limited-scope advice instead of a full plan.

Free eBook Financial Adviser Meeting Preparation Checklist (Instant Download)

〰️

Free eBook Financial Adviser Meeting Preparation Checklist (Instant Download) 〰️

6) Statement of Advice

You’ll receive an SoA that explains the strategy, risks, costs and alternatives. James walks you through the document, page by page, and answers questions before anything proceeds. SoA is the regulated record of advice provided under an AFSL; it sits within the broader planning process.

See Financial Planner vs Financial Adviser for the planning vs advice distinction and how to verify an adviser.

7) Implementation

Once you approve the SoA, James coordinates forms, platform setup, and any provider changes. Online or in-office, you get the same AFSL rules, fee disclosures, and identity checks. The team documents custody, execution, and status updates so you always know what’s next.

This phase may include liaising with your accountant, mortgage broker, or solicitor to keep tax, debt, and estate settings aligned.

8) First 90 Days

Early in the engagement, James confirms accounts, contributions, rebalancing settings, and beneficiary nominations. You’ll receive a short note summarising what’s live, what’s pending, and any items waiting on third parties. Online clients get the same confirmations through the portal with timestamps.

9) Review Cadence

You choose an appropriate frequency: annual, half-yearly, or quarterly. Review packs cover performance, fees paid, changes since last meeting, and next steps. Many clients prefer a hybrid model: one in-person deep-dive with printed packs, plus shorter video triage between meetings for quick issues.

If several decisions collide at once, book the office for a longer whiteboard session; otherwise, most follow-ups shift well to video without losing quality.

10) Change Management

Events such as property moves, inheritances, career changes, or pre-retirement timing often require targeted amendments. The service model allows for short, event-driven advice where needed, or a comprehensive refresh when several topics connect. The aim is to meet deadlines and avoid irreversible errors.

Free Download Financial Adviser Meeting Preparation Checklist (Instant Download)

〰️

Free Download Financial Adviser Meeting Preparation Checklist (Instant Download) 〰️

Scope and Boundaries

James focuses on super and SMSFs, transition to retirement, retirement income, inheritance, shares and ETFs, property strategy, ethical investing, first-home advice, Age Pension strategy, aged care planning, and estate alignment with your solicitor. He is non-bank aligned and client-paid.

Some planners handle Centrelink applications or debt consolidation. James does not offer these services. If a request sits outside scope, he will say so early and suggest alternatives so your time is respected.

For an overview of the financial service menu, see: What Areas Do Financial Planners Cover?

Online vs In-office

Video meetings suit time-poor professionals, pre-retirees coordinating with adult children, and anyone outside the Shire who still wants a Sydney adviser. In-person often fits complex family decisions. The regulatory standard is identical either way, including SoAs, fee disclosure, and annual consent.

Choose the right space for your meetings after reading Online Financial Planning Services.

Quick Reference Table

The table below summarises roles and deliverables across the core stages. Use it as a checklist during the engagement.

| Stage | What You Receive | Who Does What |

| Triage | Call notes, prep checklist | You confirm goals; James confirms fit |

| Discovery | Meeting summary, document list | You upload documents; James scopes work |

| Proposal | Scope, fees in dollars, timetable | You approve or refine; James schedules SoA |

| SoA Briefing | Formal recommendations with risks and costs | James explains; you approve or pause |

| Implementation | Forms lodged, custody documented | James coordinates providers; you e-sign |

| Reviews | Pack with performance, fees, changes, actions | You choose cadence; James reports and adjusts |

The same table applies whether you meet on Zoom or in the office. The difference is convenience, not standards.

Who This Process Suits

James Hayes’ process is intended for:

CBD professionals and Sutherland Shire locals who want an adviser close to home after work

Pre-retirees five to ten years out who need retirement income modelling and contribution settings

Wealth accumulators who value a documented plan with a clear review calendar

Explore When to Get Financial Advice in Australia for age, stage and trigger maps; review What Areas Do Financial Planners Cover for service depth and check Financial Planner vs Financial Adviser to understand licensing and documents.

How to Verify and Stay Safe

Always verify the adviser on ASIC’s Financial Adviser Register, confirm AFSL and AFCA membership, and request key points in writing. Use the secure portal for uploads and e-signing, and reconfirm any bank-detail change on a live call. Keep screenshots with dates in your files.

The information in How to Choose a Financial Adviser in Australia and Common Mistakes When Choosing a Financial Adviser will be useful to you.

Conclusion

Good planning is systematic. You start with fit and scope, move through formal advice, implement with care, and keep a steady review cadence. Whether online or in-office, you should receive the same documents, controls and clarity. When the moving parts change, the plan updates and the calendar keeps you on track.

If you would like James Hayes to work out a financial plan for you, please book a complimentary 15-minute introductory call.

FAQs

-

You’ll get a short checklist and a link to book the discovery session. In that meeting, we map goals, constraints, and timelines. I then send a written proposal with fees in dollars and inclusions. If you’re happy, we proceed to an SoA and implementation.

-

No. You receive the same SoA, disclosures, and audit trail. We use a secure portal and e-signing for speed, and I document custody and execution. If a topic needs a calm room or whiteboard, we meet in the office, then switch back to video for reviews.

-

Fees reflect scope and complexity. I quote in dollars, upfront, before work begins. Typical upfront ranges are provided in writing. You’ll see what’s included, from meetings and modelling to implementation and reviews. You approve the SoA before implementation, so timing and costs remain transparent throughout.

-

I advise on strategy and timing for Age Pension settings, but I don’t lodge Centrelink forms or consolidate debts. If your request sits outside my scope, I’ll say so early and point you to suitable alternatives. That respects your time and keeps focus on the work I do best.

Financial Planner Knowledge Bundle

- What Exactly Does a Financial Planner Do?

- Financial Advice vs Financial Planning

- Independent vs Institution-Linked Financial Advisers

- What Does Financial Advice Cost in NSW?

- How to Choose the Right Financial Adviser in Australia

- When to Get Financial Advice in Australia

- What Areas Do Financial Planners Cover?

- Online Financial Planning Services

- Financial Planning Process Explained

- Common Mistakes When Choosing Financial Advisers

- Certified Financial Planner (AFP®/CFP®) Explained

- Financial Adviser Regulation & Licensing (ASIC/AFSL) Explained

- Local Financial Planning Services in Sutherland Shire

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.