When to Get Financial Advice in Australia: Age, Stage, Triggers

Summary

Get advice when stakes rise, rules are complex, or decisions interlock. Typical triggers include first job, property purchase, family changes, rising income, inheritance, SMSF considerations, pre‑retirement planning, and aged care choices. A short, targeted engagement can solve one decision, while a full plan coordinates super, investments, insurance, and cashflow.

Free eBook Financial Milestones Roadmap (Instant Download)

〰️

Free eBook Financial Milestones Roadmap (Instant Download) 〰️

Download Now

Introduction

Financial advice delivers the most value when it is engaged at decision points. These points arise with age, changing responsibilities, new capital, and rising complexity. This guide outlines the key moments to seek advice, how to prepare, and includes a fillable roadmap you can use to plan the next 12 to 36 months.

Seek advice when one or more of these conditions apply: the stakes are high, the rules are complex, your time is scarce, or multiple money decisions interlock. In practice, that looks like retirement timing, investment structure, super contributions, insurance cover, or entity choices that carry long‑term consequences.

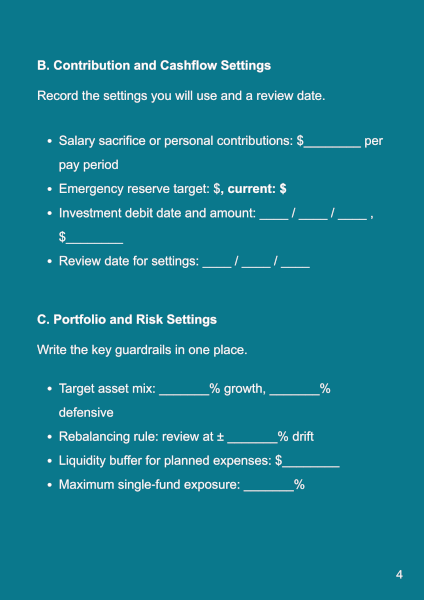

Before you read, you might want to download our fillable Financial Planning Roadmap to plot the upcoming 12 to 36 months.

Age and Stage

Life stage does not dictate wealth, yet it does shape common decisions. Use the map below to anticipate where tailored advice adds value.

Early Career (First Full‑time Role, 20s to Early 30s)

At this stage, small choices compound for decades. Advice helps set foundations that survive job changes and rising income.

Super contributions and fund selection

Cashflow system and emergency reserve

First investment account or ETF plan

Insurance needs aligned to income and dependants

HECS‑HELP strategy in the context of saving and investing

A short advice engagement can install the framework you use for the next five years.

Household Formation (Couple, Home Purchase, Children)

Responsibilities expand, and risk tolerance often shifts. Advice aligns debt, protection, and investing with real‑world cash demands.

Deposit strategy and purchase budget

Loan structure, offset use, and repayment order

Income protection, life and TPD cover sized to liabilities

Investment plan that coexists with mortgage reduction

Education saving plan with realistic targets

Expect a written plan that protects the household and keeps growth on track.

Instant & Free eBook: Financial Milestones Roadmap

〰️

Instant & Free eBook: Financial Milestones Roadmap 〰️

Peak Earning Years (Mid‑career Professionals and Business Owners)

Income rises, complexity follows. Advice coordinates tax awareness, super, portfolio design, and business cashflow.

Salary sacrifice and non‑concessional contribution strategy

Portfolio construction and automated rebalancing

Entity selection for investing or business cashflows

Insurance review as liabilities change

Liquidity planning for lumpy expenses and opportunities

Annual reviews keep the plan aligned with changing income and obligations.

Pre‑retirement (5 to 10 Years from Finishing Work)

Decisions here set retirement income for decades. Modelling clarifies contribution settings, drawdown rates, and risk.

Retirement income projections and sequencing of withdrawals

Super fund selection and contribution caps

Transition‑to‑retirement considerations, where relevant

Portfolio risk calibration for lower volatility

Tax‑aware cashflow between super and non‑super balances

Written projections support confident decisions on dates and spending.

Retirement and Later Life (Income, Health, Estate Intentions)

The priority shifts to reliability, administration, and protecting family wishes.

Account‑based pension setup and cashflow calendar

Portfolio maintenance with a focus on liquidity and fees

Insurance wind‑down or repurposing as liabilities reduce

Estate document alignment with beneficiary nominations

Planning for aged care funding structures and service choices

Advice here reduces administrative strain and household risk.

Organise upcoming financial decisions by age or life stage simply by using the Financial Milestone Roadmap. It helps you sort out what to do now, what to delay, and what needs advice.

Event‑driven Triggers

Events often carry deadlines or irreversible choices. A short, targeted engagement can prevent costly errors.

Property transaction: Buying, selling, renovating, or restructuring loans.

Liquidity event: Inheritance, business sale, equity vesting, bonuses.

Career change: New role, redundancy, self‑employment.

Family changes: Marriage, separation, children.

Health changes: Reviewing cover and cash reserves.

Cross‑border moves: Migration or returning to Australia, residency status.

SMSF considerations: Trustee responsibilities, investment approach, audit readiness.

Major market shifts: Portfolio risk review and rebalancing discipline.

Event timing rarely matches review dates, which is why an adviser’s on‑call support is valuable.

Complexity Signals

Complexity is a signal to pause and call in help because DIY ups the risk factor. The list below captures common thresholds.

Multiple platforms or funds with overlapping fees

Blended family or multiple entities with unclear ownership

Large cash balances without an investment policy

Insurance structures that no longer match liabilities

Confusion around contribution caps or pension rules

Portfolio risk that conflicts with spending plans

Administrative strain that delays decisions

If two or more apply, schedule a discovery meeting.

Alternatively, you can use James Hayes’ Financial Roadmap to stay organised and avoid rushed decisions.

Confusion Around Financial Instruments

Confusion is a legitimate trigger. If you cannot explain a product or strategy in a few sentences, request a plain‑English brief from a licensed adviser. Expect the brief to cover purpose, benefits, costs, risks, and the alternative considered. If clarity does not follow, walk away.

Limited‑scope or Full Plan

Not every situation requires a full plan. Use this guide to size the engagement.

| Situation | Engagement style | Outputs to expect |

| One decision, low interdependence | Limited-scope session | Short Record of Advice, action list |

| Two to three linked topics | Targeted project | Statement of Advice , implementation support |

| Retirement, inheritance, or multi-entity | Full plan | Modelling, investment policy, service calendar |

If in doubt, start small, then expand once value is demonstrated.

Documents and Information to Prepare

Preparation shortens the path to useful advice. Bring current statements and a clear summary of your goals.

Super and investment statements, loan summaries, and insurance schedules

Two recent payslips and last tax return

Household budget and upcoming large expenses

Estate documents and beneficiary nominations

A one‑paragraph scope statement and questions

The first meeting should convert this material into a clear plan outline.

Conclusion

Timing matters. Engage advice when stakes, complexity, or time pressure are high. Use the roadmap to convert intentions into dates and actions. A clear plan, reviewed on a set cadence, reduces error, supports better decisions, and lowers stress throughout each stage of life.

For selection guidance, see How to Choose the Right Financial Adviser. For pricing and value scenarios, see What Does Financial Advice Cost in NSW?

FAQs

-

No. This stage sets your long‑term trajectory. We align loan structure, cashflow, super contributions, and a simple investment plan that coexists with repayments. We also right‑size insurance to liabilities and dependants. A short project is often enough, with a yearly check to keep momentum.

-

Review it now. Pay rises change capacity for salary sacrifice and non‑concessional contributions. Small setting changes compound for decades. We also revisit your emergency reserve, investment debit, and insurance cover so your plan reflects the new income level rather than last year’s numbers.

-

Park the funds in a safe place and pause. We then map near‑term cash needs, debt options such as offset, portfolio structure, and estate alignment. The goal is to avoid rushed choices, set liquidity correctly, and place the balance into a fee‑aware, risk‑appropriate structure with written rationale.

-

Park the funds in a safe place and pause. We then map near‑term cash needs, debt options such as offset, portfolio structure, and estate alignment. The goal is to avoid rushed choices, set liquidity correctly, and place the balance into a fee‑aware, risk‑appropriate structure with written rationale.

-

Sequence and sustainability. We model spending, contribution settings, portfolio risk, and a drawdown path. The plan covers the mix between super and non‑super balances, income timing, and a schedule for reviews. With numbers on paper, you can pick a date with far greater confidence.

-

Yes. Confusion is a valid trigger. In our first meeting we translate options into plain English, show costs and risks, and compare a small set that fits your goals. If there is no clear benefit to acting, the recommendation will be to do nothing and review later.

Financial Planner Knowledge Bundle

- What Exactly Does a Financial Planner Do?

- Financial Advice vs Financial Planning

- Independent vs Institution-Linked Financial Advisers

- What Does Financial Advice Cost in NSW?

- How to Choose the Right Financial Adviser in Australia

- When to Get Financial Advice in Australia

- What Areas Do Financial Planners Cover?

- Online Financial Planning Services

- Financial Planning Process Explained

- Common Mistakes When Choosing Financial Advisers

- Certified Financial Planner (AFP®/CFP®) Explained

- Financial Adviser Regulation & Licensing (ASIC/AFSL) Explained

- Local Financial Planning Services in Sutherland Shire

Disclaimer

The information in this article is provided as a general guide only. It does not constitute personal financial advice and should not be relied upon as such. Readers should seek advice from a licensed financial adviser before making any financial decisions. James Hayes and his associated entities accept no responsibility or liability for any loss, damage, or action taken in reliance on the information contained in this article. Links to third-party websites are provided for reference purposes only. We do not endorse or guarantee the accuracy of their content.